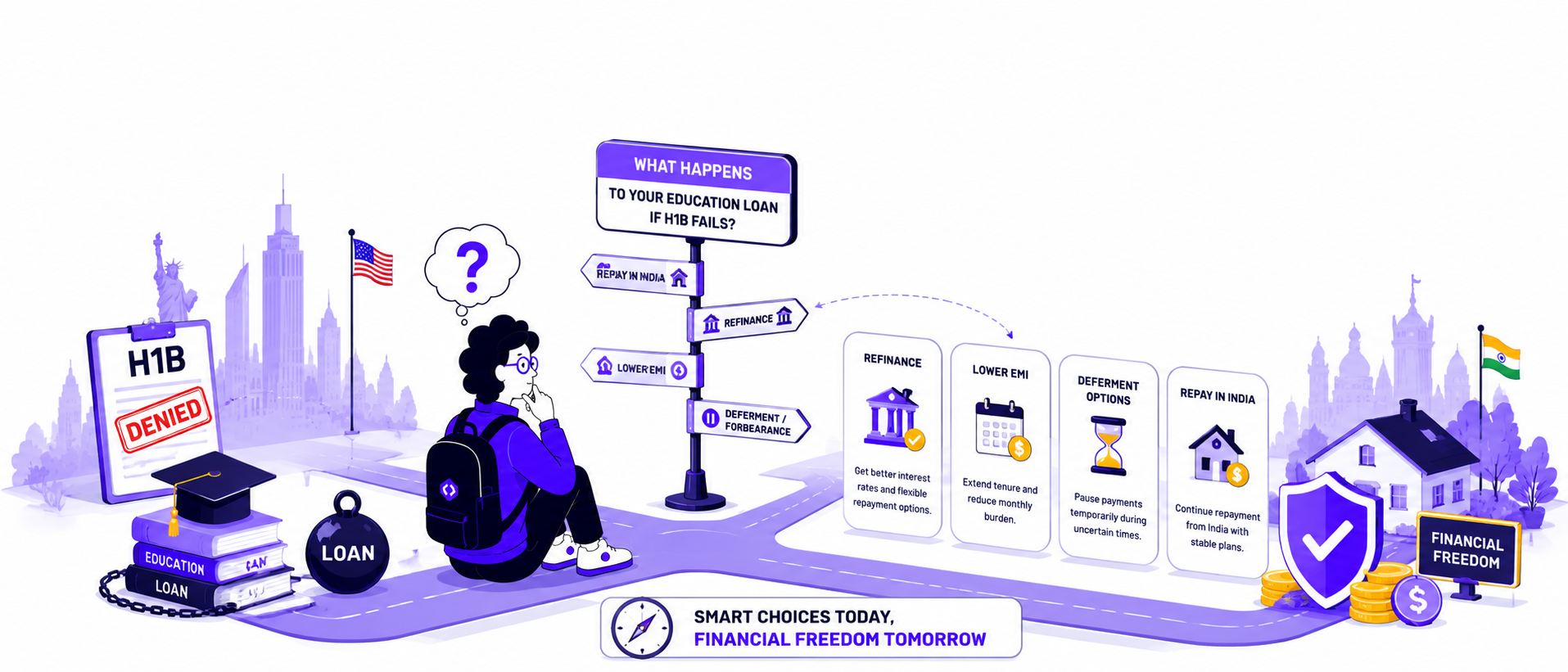

What happens to an education loan if H1B fails is simple at the contract level: nothing changes automatically. Your Indian education loan does not pause, reduce, or get cancelled because your H1B or OPT did not come through. The loan is governed by your agreement and Indian banking rules, not your US visa status. Refinancing is the most effective way to bring your EMI back in line with your actual income, in USD or INR.

In this guide, you’ll learn:

- What happens to education loan if H1B fails, stage by stage

- Why refinancing should be your first move, not your last resort

- How much refinancing can save you

- When to refinance to qualify for the best rate

- What to do if you’ve already missed payments

- How to protect your CIBIL score and your family’s collateral

What happens to an education loan if H1B fails?

What happens to an education loan if H1B fails comes down to one fact: the lender is never informed of your visa outcome, so the loan continues exactly as agreed. There is no built-in clause that pauses or adjusts EMIs because a lottery result didn’t go your way.

This is increasingly common. For the FY2027 H1B cycle, USCIS introduced wage-weighted selection, and early estimates put odds for Level I registrations (most entry-level roles) as low as 12 to 18%, against 55 to 65% for Level IV. The FY2027 cap lottery prioritized Level 4 registrations first, then Level 3, Level 2, and Level 1, meaning seniority and pay now matter more than chance ever did. Most recent graduates apply at Level I.

If you’re on standard OPT (12 months), you typically get one lottery attempt before your work authorization runs out. STEM OPT extends this to 36 months and multiple attempts, which helps but does not guarantee a result.

The Moratorium Still Ends on Schedule

Most education loans carry a moratorium equal to course duration plus six to twelve months. Principal isn’t due during this period, but interest typically continues to accrue and compound daily unless you’re covered under the government’s CSIS subsidy scheme.

If you’re wondering what happens to education loans if H1B fails while you’re still inside the moratorium, this is your best window to act. Refinancing here, before any EMI is due and before any payment history exists on the loan, gives you access to the strongest possible terms.

EMIs Start Whether You’re Employed or Not

Many lenders have no formal visa-failure clause. The EMI date doesn’t move because your visa outcome didn’t go as planned.

What Happens If You Miss EMIs?

| Timeline | Consequence |

| First missed EMI | Reported to CIBIL within 30 days; score drops 30–50 points |

| 90+ days non-payment | Loan classified as Non-Performing Asset (NPA) |

| NPA classification | 100–150 point CIBIL score drop; recovery process begins |

| NPA on record | Stays on credit report for 7 years from first missed payment |

| Secured loan above Rs 7.5 lakh | Lender can invoke SARFAESI Act and seize collateral without a court order |

| Unsecured loan below Rs 7.5 lakh | Recovery through civil courts or Debt Recovery Tribunal |

A parent co-applicant’s CIBIL score is hit equally hard. If property was pledged, it can be seized and auctioned once the loan turns NPA. This is the harshest version of what happens to education loans if H1B fails, and exactly the outcome refinancing, done early, is meant to prevent.

Why refinancing should be your first move

Refinancing replaces your existing education loan with a new one priced against your actual current income, not the income your lender assumed when you first borrowed. It changes the terms rather than waiting out the consequences.

What Refinancing Changes

Lower Interest Rate

If you originally borrowed at 11–13%, steady income in India can qualify you for a lower-rate product. Moving from 12% to 9% on a Rs 50 lakh loan over 10 years saves approximately Rs 9–11 lakh in total interest.

Restructured Tenure

A longer tenure lowers your monthly EMI immediately, useful if you’re earning in INR rather than USD. A shorter tenure clears the loan faster if income allows. You choose the direction.

Loan Consolidation

Secured and unsecured loans can sometimes be combined into one agreement with better blended terms.

Earlier Collateral Release

Refinancing into a smaller or unsecured product can free up pledged property sooner than your original term would have.

When to Refinance

Refinancing eligibility depends on demonstrated income and a clean repayment record. Refinance during the moratorium or in the first few EMIs, before anything has gone wrong, and you negotiate from strength. Wait until after missed payments, and approval gets harder, with worse terms if it’s offered at all.

What happens to an education loan if H1B fails while you’re still in the US?

If your H1B attempt didn’t land but you’re still on STEM OPT, you have time before refinancing in India becomes relevant, and what happens to an education loan if H1B fails looks different for you than for someone whose OPT has already run out.

You can register again in the next lottery cycle or pursue a cap-exempt employer, such as a university, non-profit research organization, or government research institution, which can file H1B petitions year-round outside the lottery. A change of status to O-1 or L-1 is also worth exploring.

Continuing to earn in the US keeps your loan current and builds the income history that strengthens a future refinance application, regardless of which currency that income is in.

What happens to an education loan if H1B fails and you return to India?

India’s job market for US-educated professionals in tech, finance, consulting, and data roles has improved.

For most students researching what happens to education loans if H1B fails and weighing a return home, the real question is whether income in India can realistically support the EMI.

Entry salaries in Tier 1 cities for returning graduates with US experience often range from Rs 12–20 lakh annually. An EMI of Rs 40,000–60,000 a month, common for a Rs 40–50 lakh loan, takes up a significant share of that salary at the original loan terms.

This is where refinancing earns its place. Lowering the rate by two to three percentage points and adjusting tenure to match an INR salary can bring that EMI down to a manageable level.

Secure employment first, then refinance once you have two to three months of salary slips to show a lender.

Talk to your existing lender before missing payments

Before shopping a refinance elsewhere, call your current lender.

Banks and NBFCs have discretionary options for genuine hardship, including:

- Extended tenure

- Temporary EMI holiday

- Interest-only repayment periods

None of this is automatic. Ask before you miss a payment, since lenders have far less flexibility once you’re already behind.

Sometimes your existing lender will match what an external refinance offers without the paperwork of switching.

What happens if your education loan has already become problematic?

If missed payments have already happened and a strong refinance is no longer realistic, a One-Time Settlement (OTS) is the next option for resolving an education loan if H1B fails after the situation has already escalated.

The lender agrees to close the account for a lump sum below the outstanding balance. Your credit report will show “settled” rather than “closed,” which affects future borrowing, but it can be the most pragmatic exit from a genuinely difficult position.

Impact on co-applicants and guarantors

Loans above Rs 4 lakh typically require a co-applicant, usually a parent. Loans above Rs 7.5 lakh require a guarantor or collateral.

Both student and co-applicant carry legal liability.

If the loan defaults:

- The co-applicant’s CIBIL score takes the same hit

- Recovery agents can contact them directly

- Pledged property can be seized under SARFAESI after proper notice

Refinancing early is one of the strongest ways to protect a co-applicant from this outcome.

How to protect yourself financially if H1B fails

Financially prepared students typically:

- Pay interest during the moratorium, even though it isn’t mandatory

- Compare refinancing lenders and NBFCs during the second year of study

- Maintain an emergency fund covering three to six months of EMI

- Create a backup plan before lottery results arrive

- Keep co-applicant parents informed about visa risk and refinancing plans

On a Rs 50 lakh loan at 11%, untouched compounding over two and a half years adds up significantly. Early planning can prevent future repayment stress.

Education loan options after H1B failure by situation

| Situation | Best Approach | Key Risk |

| Still on STEM OPT, not selected | Reapply next cycle; explore cap-exempt employers | OPT/EAD expiry |

| OPT expired, no H1B | Secure employment in India, then refinance | Lower INR salary vs. original EMI |

| Moratorium still active | Start comparing refinancing options now | Compounding inflates principal |

| Employed in India, clean record | Refinance into lower-rate, restructured product | Eligibility and terms vary by lender |

| Moratorium ended, missed EMIs | Contact lender for restructuring before refinancing elsewhere | NPA classification; CIBIL damage |

| NPA classified, secured loan | Explore OTS or structured repayment | SARFAESI; collateral at risk |

Turn uncertainty into a clear education loan repayment plan

An H1B rejection doesn’t change your education loan obligations, but it does change the financial decisions you need to make next. The earlier you act, whether that’s exploring refinancing, restructuring your loan, or planning your return to India, the more options you’ll have and the better your outcome is likely to be.

At GradRight, we help students navigate these decisions with confidence. We compare refinancing opportunities across multiple lenders, identify options suited to returning professionals, and help you understand how different interest rates and repayment terms can impact your monthly EMI and total loan cost.

If you’re still in your moratorium period or have recently returned to India, now is the best time to evaluate your options and build a repayment plan that matches your reality, not the assumptions made when you first borrowed.