A UK-based professional who refinanced from a high-rate NBFC to a leading bank and immediately lowered both his EMI and long-term interest burden.

Case Study Overview

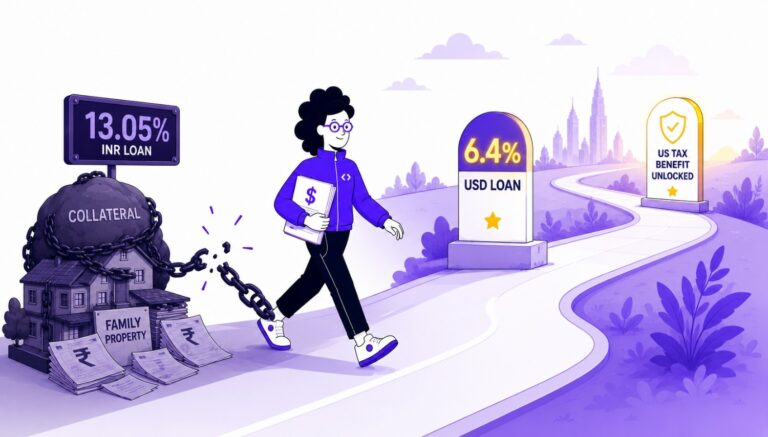

Rohan had built a solid career after graduating from Queen Mary University of London. Working in the UK- a good job, a stable life. But one thing was quietly draining his finances every month: an education loan of ₹47 lakhs at 14.1%.

For a professional earning in GBP, servicing an INR loan at that rate meant paying a premium that didn’t reflect his current financial strength. Every EMI- approximately ₹81,900 per month – carried more interest than it needed to.

GradRight assessed his profile and facilitated a refinance from the original lender to a leading Indian bank, bringing the rate down to 10.4%. Monthly EMI dropped to ₹72,300- a saving of ₹9,600 per month, and ₹9.2 lakhs in total interest savings over the tenure.

Student Financial Profile

| University | Queen Mary University of London |

| Location | United Kingdom |

| Employment Status | Full-time |

| Outstanding Loan Amount | ₹47 Lakhs |

| Original Interest Rate | 14.1% |

| Original Monthly EMI | ₹81,900 |

READ MORE: Student Loan Refinancing Explained: Is It Worth It?

Problem Statement

A Rate Built for a Different Borrower 14.1% was a rate assigned when Rohan was a student with no income and an unproven profile. Working full-time in the UK, earning in GBP, with a consistent repayment track – that borrower no longer existed. The rate should have changed. It hadn’t.

The Currency Friction of an INR Loan Rohan earned in GBP and serviced a loan in INR. Every EMI involved a currency conversion – adding friction, exchange rate exposure, and unnecessary complexity to a monthly obligation that could have been simpler.

A Monthly Cost That Added Up At ₹81,900 per month, the EMI was substantial. Over the remaining tenure, the total interest burden at 14.1% represented a significant and avoidable excess – money that could have been redirected into savings or investments.

Solution

GradRight assessed Rohan’s profile and identified the right refinancing lender – one offering a meaningfully lower rate for a borrower with his employment profile and repayment history.

Single Move – Original Lender to New Lender Rohan’s loan of ₹47 lakhs was refinanced to a leading Indian bank at 10.4%. A clean, single-step transfer that immediately restructured the monthly cost and the total interest burden over the remaining tenure.

Old Loan → New Loan

Old Loan

| Interest Rate | 14.1% |

| Outstanding Loan Amount | ₹47 Lakhs |

| Monthly EMI | ₹81,900 |

New Loan

| Lender | Leading Indian Bank |

| Interest Rate | 10.4% |

| Monthly EMI | ₹72,300 |

| Monthly Saving | ₹9,600 |

READ MORE: Top 7 Myths About Refinancing Education Loans You Shouldn’t Believe

How Did GradRight Help?

Profile Assessment GradRight evaluated Rohan’s employment status, income, repayment history, and outstanding balance to confirm eligibility and identify the right lender.

Lender Match GradRight identified the right lender for Rohan’s profile and secured the refinance at 10.4% – a 3.7 percentage point reduction from his original rate.

End-to-End Execution GradRight managed the full process from application to disbursement, ensuring a clean transition with no complexity for Rohan to navigate from the UK.

Results

- Rate: 14.1% (Original Lender) → 10.4% (New Lender)

- Monthly EMI: ₹81,900 → ₹72,300 (saving ₹9,600 per month)

- Total Interest Savings: ~₹9.2 Lakhs over 8-year tenure

- Improved cash flow for UK-based career building

A monthly saving of ₹9,600 – roughly £900 at current rates – adds up to over ₹9.2 lakhs over the tenure. That’s money Rohan can redirect into savings, investments, or simply the quality of life he’s worked hard to build abroad.

For every Indian professional working abroad and still carrying a high-interest NBFC loan, Rohan’s story is a clear signal: your financial profile has changed since you took that loan. Your interest rate should too.