A deeply personal refinance story- against real odds- that ended with the lowest rate in this entire collection.

Case Study Overview

Rajeev’s situation was unlike any standard refinance case. Both his parents had passed away. His brother- listed as co-applicant on his loan at 13.5%- was struggling to get new loans for himself because of this shared liability. Rajeev wanted to free his brother. That was the goal.

But the path to that goal was blocked at every turn. A US credit score of 670- below most lenders’ thresholds. A Delinquent Payment Days (DPD) entry from a personal loan in 2021. Multiple rejections from lenders who cited the absence of a house in India. On paper, the file looked risky.

GradRight didn’t walk away. The team studied both his Indian and US credit profiles in detail, identified specific fixable issues, and drew up a credit repair plan. Rajeev followed through. A few months later, his score had climbed from 670 to 710- and a US bank approved the refinance at 4.9% fixed.

Student Financial Profile

| Visa Status | H1B |

| Annual Income | $120,000 |

| Original Interest Rate | 13.5% |

| Original Loan Currency | INR |

| Co-applicant | Brother |

| US Credit Score (Before) | 670 |

| US Credit Score (After) | 710 |

| Prior Rejections | 3 (multiple lenders who declined) |

READ MORE: Student Loan Refinancing Explained: Is It Worth It?

Problem Statement

A Brother Caught in a Shared Liability Rajeev’s brother was listed as co-applicant on the loan. Because of that shared liability, he was unable to secure new loans for himself- his creditworthiness was effectively held hostage by a loan that wasn’t his. Freeing his brother was the primary goal, before any conversation about rates.

A Credit Profile With Fixable Problems A US credit score of 670 and a DPD entry from 2021 made Rajeev’s file look risky at first glance. Combined with the absence of property in India- a requirement several lenders had- this had already produced three rejections. But GradRight identified that the issues weren’t structural. They were fixable.

Rejected Three Times- But Not Done Three lenders had all declined. Three rejections for a borrower with an H1B visa and a $120,000 salary pointed to a presentation and credit problem, not an eligibility problem. The right path was repair, not retreat.

Solution

GradRight studied Rajeev’s complete credit picture- both Indian and US profiles- and identified the specific items dragging his score down: small outstanding credit card dues and a minor loan that were creating unnecessary negative signals.

Credit Repair First GradRight advised Rajeev to close the outstanding credit card dues and the minor loan. Rajeev followed through precisely. Within a few months, his US credit score moved from 670 to 710- crossing the threshold that made him eligible for US bank refinancing.

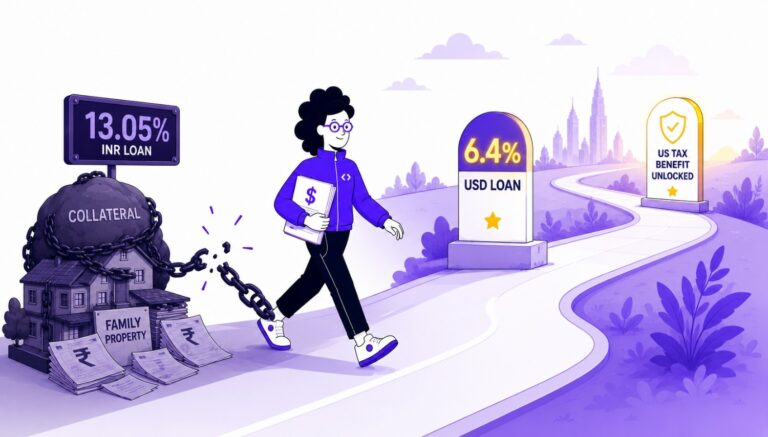

Then, the Refinance With an improved score and a well-prepared application file, GradRight took Rajeev’s case to a US bank. This time, it was approved. The loan was fully refinanced at 4.9% fixed-converting from INR to USD and aligning with his US income. His brother was removed as co-applicant entirely.

Old Loan → New Loan

Old Loan

| Interest Rate | 13.5% |

| Loan Currency | INR |

| Co-applicant | Brother |

| US Credit Score at Time | 670 |

New Loan

| Lender | US Bank |

| Interest Rate | 4.9% Fixed |

| Loan Currency | USD |

| Co-applicant | None |

READ MORE: Top 7 Myths About Refinancing Education Loans You Shouldn’t Believe

How Did GradRight Help?

Diagnosing the Real Problem Three rejections suggested a fixable problem, not a fundamental ineligibility. GradRight studied both credit profiles in detail and identified precisely what was dragging the score down.

Building a Credit Repair Plan GradRight drew up a targeted credit repair plan- specific actions, not vague advice. Close these dues. Clear this loan. Rajeev followed through, and the score moved.

Preparing a Strong Application File With the improved score, GradRight prepared a well-structured application and took the case to a US bank- presenting a complete, compelling picture of a borrower who had addressed his credit issues and had the income to support the loan comfortably.

Freeing the Brother The co-applicant removal was central to the entire exercise. GradRight ensured it was built into the refinance structure from the start- not an afterthought.

Results

- Rate: 13.5% (Original Lender) → 4.9% Fixed (US Bank)

- Brother fully removed as co-applicant

- Full loan converted to USD – aligned with US income

- Credit Score improved: 670 → 710 with targeted credit repair

- Lowest rate in this collection – despite initial rejections from 3 lenders

From 13.5% to 4.9%. An extraordinary outcome for a case that three lenders had already closed the door on. Rajeev’s brother was freed. The loan was restructured. And for someone who had already carried so much loss, this was a moment of genuine relief.

Rajeev’s story is for every borrower who has been told their profile is too complicated. It sometimes is. But complicated doesn’t mean impossible – it means you need better guidance.