A student still studying abroad who not only lowered his existing loan rate but unlocked additional funding to finish his degree – all in one deal.

Case Study Overview

Most refinance stories begin after graduation. Akshat’s began while he was still studying.

With his master’s program at Monash University due to conclude in June 2026, Akshat had ₹40 lakhs outstanding with the original lender at 11.75%. He also had a problem: he needed ₹20 lakhs more to see out his degree. Taking a fresh loan at current rates while carrying an existing one was going to be expensive and administratively messy.

GradRight identified a cleaner path: a combined refinance and top-up through a leading bank. The result – a lower rate, ₹20 lakhs in additional funding, zero processing fees, and a simple interest repayment structure during the study period.

Student Financial Profile

| University | Monash University |

| Program Status | Currently studying (graduating June 2026) |

| Outstanding Loan Amount | ₹40 Lakhs |

| Original Interest Rate | 11.75% |

| Co-applicant Profile | Both parents – government employees |

| Combined Co-applicant Income | ₹2 Lakhs+ per month |

| Co-applicant Existing Liabilities | Zero |

READ MORE: Student Loan Refinancing Explained: Is It Worth It?

Problem Statement

A Funding Gap at the Finish Line With his master’s program due to conclude in June 2026, Akshat needed ₹20 lakhs more to complete his degree. The straightforward option – a fresh loan on top of the existing one – would mean managing two separate loans at different rates, with additional processing costs and administrative complexity.

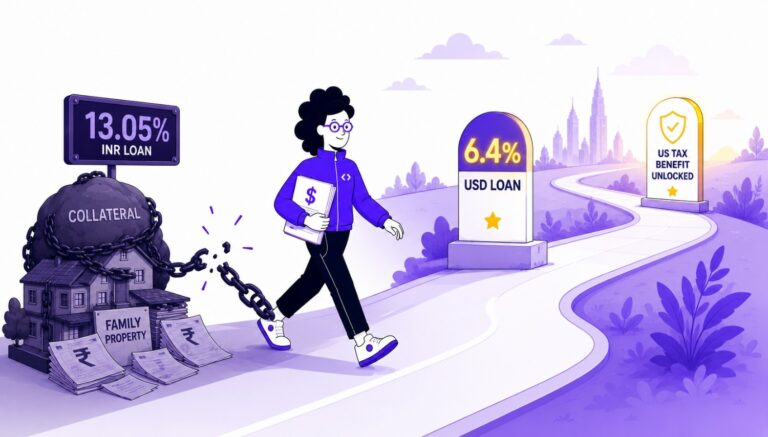

An Existing Rate That Could Be Better The outstanding loan of ₹40 lakhs at 11.75% with the original lender was serviceable – but not optimal. A lower rate was available, and a refinance made sense on its own terms. The opportunity was to solve both problems in a single transaction.

Mid-Program Refinancing – Not as Unusual as It Sounds Most borrowers assume refinancing is only possible after graduation. Akshat’s case demonstrates otherwise. With the right co-applicant profile and the right lender, a mid-program refinance and top-up is entirely achievable.

Solution

GradRight identified the right lender for a combined refinance and top-up – a single transaction that would transfer the existing loan, reduce the rate, and disburse the additional ₹20 lakhs Akshat needed, all at once.

The case was built around the co-applicant profile: both parents are government employees with a combined monthly income of over ₹2 lakhs and zero existing liabilities – a strong, low-risk financial base that gave the new lender the confidence to approve a total sanction of ₹60 lakhs.

Combined Refinance and Top-Up – Original Lender to New Lender ₹40 lakhs transferred from the original lender. ₹20 lakhs disbursed as a top-up. Total sanction: ₹60 lakhs. Rate: 9.88%. Processing fee: zero. Repayment structure: simple interest during the study period, switching to full EMI after graduation.

Old Loan → New Loan

Old Loan

| Interest Rate | 11.75% |

| Outstanding Loan Amount | ₹40 Lakhs |

New Loan

| Lender | New Lender |

| Interest Rate | 9.88% |

| Loan Transfer Amount | ₹40 Lakhs |

| Top-Up Amount | ₹20 Lakhs |

| Total Sanction | ₹60 Lakhs |

| Processing Fee | ₹0 |

| Repayment During Study | Simple Interest only |

READ MORE: Top 7 Myths About Refinancing Education Loans You Shouldn’t Believe

How Did GradRight Help?

Identifying the Combined Solution Rather than treating the rate reduction and the funding gap as two separate problems, GradRight identified a single transaction that solved both – a combined refinance and top-up through the new lender.

Building the Case Around the Co-applicant Profile GradRight structured the application around the strength of the co-applicant profile – both parents as government employees with strong, stable income and zero existing liabilities – giving the new lender the confidence to approve a ₹60 lakh total sanction.

Securing a Student-Friendly Repayment Structure GradRight ensured the new loan included a simple interest repayment structure during Akshat’s remaining study period – keeping cash flow manageable while he focused on completing his degree.

Results

- Rate: 11.75% (Original Lender) → 9.88% (New Lender)

- Loan Transfer: ₹40 Lakhs

- Top-Up Approved: ₹20 Lakhs

- Total Sanction: ₹60 Lakhs

- Processing Fee: ₹0

- Repayment Structure: Simple Interest during study period

In a single transaction, Akshat lowered his rate, freed himself from the original lender’s terms, and secured the funding he needed to complete his degree – without disrupting his academic focus or his family’s finances.

The simple interest repayment structure during the study period means the principal isn’t compounding aggressively while he’s still in class. When Akshat graduates and starts earning, he’ll step into repayment at a rate that reflects his family’s creditworthiness – not the rushed terms of his original loan.

Refinancing isn’t just a post-graduation move. If your profile supports it, you can restructure and fund – at the same time.