About 2 to 2.5 million students apply for loans annually to fund their higher education. Over 90% of these education loans are used for studies abroad. However, the traditional process of acquiring loans from banks or NBFCs works against the student’s interests – it is slow, rigid, opaque, and leaves students with the first available offer rather than the best available offer.

GradRight’s FundRight platform is one of India’s first loan-bidding online interfaces, which simplifies the process of securing education loans. Since launch, GradRight has processed approximately Rs 16,300 crore in loan requests for more than 200,000 students. This article explores how the traditional loan process compares with GradRight’s reverse-bidding model – and why the difference matters for your finances.

GradRight vs Traditional Loans – Quick Reference

| Feature | Traditional Process | GradRight FundRight |

| Number of lenders compared | 2-3 (most students visit nearby banks only) | 18+ simultaneously |

| Time to get offers | 2-4 weeks per bank | 48 hours |

| Applications required | Separate form for each lender | Single application |

| Documents uploaded | Separately to each bank | Once, shared securely with shortlisted lenders |

| Interest rate | Fixed rate from bank – little negotiation room | 9.25% – 13.50% p.a. – lenders compete, rates go down |

| Transparency | Each bank’s offer seen in isolation | All offers side-by-side on one dashboard |

| Potential savings | None – accept or reject fixed offer | Up to Rs 23 lakh over loan tenure |

| Collateral and co-signer flexibility | Rigid – SBI requires co-borrower + collateral above Rs 7.5L | More varied – market-driven model offers more options |

| Process location | Branch visits required for most banks | 100% online – zero bank visits needed |

| Expert guidance | Bank’s own officer (conflict of interest) | Unbiased FundRight expert advisors |

The Traditional Education Loan Process – What It Actually Looks Like

Before getting into GradRight’s approach, it is worth being honest about what the traditional way looks like. Traditionally, if students needed education loans, they would turn to public and private banks or NBFCs. The process involves many time-consuming steps:

- Research and select a lender – spending days visiting branches, calling bank helplines, asking seniors

- Fill out separate applications for each lender – each bank has its own form, its own document checklist

- Provide extensive documentation – admission letter, academic records, collateral documents, co-signer details – again, separately to each lender

- Undergo interviews and credit checks – often requiring in-person visits

- Wait for approval – which can take from several days to several weeks

The selection process itself requires significant time and effort to compare loan terms like interest rates, co-applicant requirements, and collateral (property, fixed deposit, etc.) requirements. Most students end up applying to just 2-3 banks because going further is too exhausting – and they accept whichever offer arrives first, not the best available offer.

For students in non-metro cities, this process is even harder due to fewer bank branches and slower communication. The conventional lending process is outdated and tedious – yet thousands of students still navigate it every intake cycle.

Also Read: Education Loan Providers in India – Top Banks, NBFCs, International Lenders

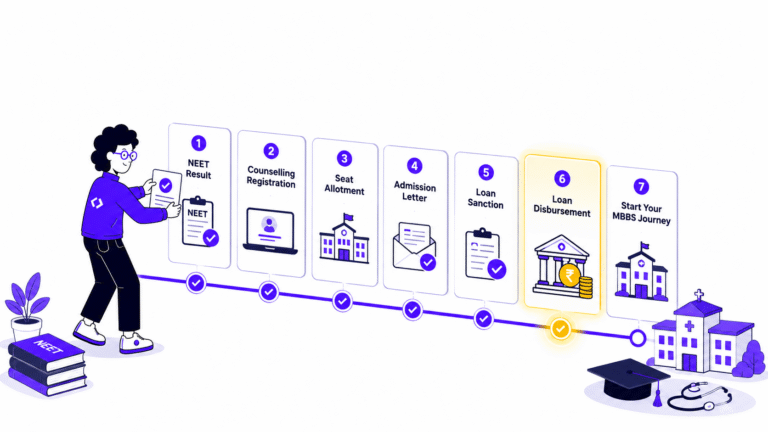

How GradRight FundRight Works – The Reverse Bidding Model

GradRight’s loan search platform is one of India’s first loan-bidding online interfaces. Instead of students chasing banks for loans, GradRight flips the model: lenders compete for your profile.

The process is algorithm-driven and focuses on student merit and future potential. Here is how it works:

| Step | What Happens |

| 1. Submit one profile | Create your profile on GradRight with ~20-30 data points: admission details, academic history, co-applicant information, loan amount needed |

| 2. Profile goes to 18+ lenders | All partner lenders receive your profile simultaneously. Your sensitive information remains inaccessible to lenders until you show interest in their offers – no spam. |

| 3. Lenders bid for your business | Lenders see your profile and respond with their best offer. Because they can see competing bids, they are incentivized to offer better terms. |

| 4. Compare all offers in one place | All offers appear side-by-side on your dashboard: interest rates, EMI, processing fees, collateral requirements, repayment terms. Full transparency. |

| 5. Talk to an unbiased expert | GradRight advisors help you understand complex terms, compare true total costs (not just headline rate), and negotiate better deals. |

| 6. Choose and complete online | Select your preferred offer, upload documents once, and complete the entire process digitally – zero bank visits required. |

Submit your profile once. Get 18+ competing offers in 48 hours. Free, online, expert-guided. Start on GradRight FundRight

Interest Rates: GradRight vs Traditional Process

The traditional loan process involves fixed-rate slabs with little room to negotiate. When you approach an individual bank, you receive the rate their policy assigns to your profile – there is no competitive pressure to offer you a better deal.

On GradRight, multiple lenders compete for your business. This competitive environment keeps interest rates down. Most loan offers for studying abroad through GradRight fall between 9.25% and 13.50% per annum. On GradRight, you can compare rates and terms side-by-side with full transparency.

| Scenario | Rate You Pay | Why |

| Traditional: First bank that approves you | Whatever their fixed rate slab says – no leverage | No competition, no transparency |

| Traditional: After visiting 3 banks | Slightly better – you have some comparison data but limited leverage | Minimal competition, high effort |

| GradRight: 18+ lenders competing simultaneously | Lowest available rate for your profile – lenders see each other bidding | Maximum competition, full transparency |

| GradRight typical rate range | 9.25% – 13.50% p.a. | Competitive market rate vs fixed bank slabs |

The numbers matter: students who choose the lowest available rate through GradRight versus accepting the first available traditional offer can save up to Rs 23 lakh over the loan tenure. On a Rs 40 lakh loan, even a 1.5% rate difference over 10 years amounts to approximately Rs 8-9 lakh in additional interest.

Also Read: Compare Education Loan Interest Rates – All Lenders 2026

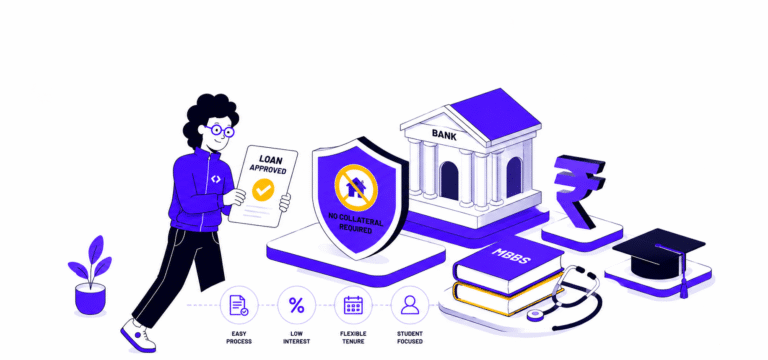

Collateral and Co-signer Rules: GradRight vs Traditional

Banks like SBI demand a parent or guardian co-borrower on every education loan, and also require tangible collateral for loan amounts above Rs 7.5 lakh. This rigid requirement excludes many deserving students who do not have property or high-net-worth co-applicants.

While conventional loan terms are stricter and hard to negotiate, GradRight’s market-driven model gives access to multiple lenders with varied requirements. Therefore, collateral and co-signer rules are more flexible. Students can access:

- Unsecured loans without pledging any collateral (up to Rs 75 lakh-1.5 crore depending on profile)

- Loans without Indian co-signers through international lenders like Prodigy Finance

- Flexible eligibility based on university ranking and future earning potential, not just current family wealth

| Feature | Traditional Bank (e.g. SBI) | GradRight (across 18+ lenders) |

| Co-borrower | Mandatory – parent/guardian | Varies – some lenders more flexible |

| Collateral (above Rs 7.5L) | Required – property/FD | Unsecured options available up to Rs 1.5Cr+ |

| Collateral-free limit | Rs 7.5L (standard IBA) to Rs 50L (premier insts) | Up to Rs 1.5Cr on platform for strong profiles |

| No Indian co-signer | Not possible | Possible via Prodigy Finance, MPower for eligible programs |

Documentation and Process: One Upload vs Repeated Paperwork

Unlike traditional bank loans, GradRight makes the whole process paperless. Upload your documents once and share them securely with your shortlisted lenders. Everything happens online.

| Process Step | Traditional Route | GradRight Route |

| Research lenders | Days visiting branches, calling helplines | Done for you – 18+ lenders pre-integrated |

| Application forms | Separate form per bank | Single profile – 15-20 minutes |

| Document submission | Separate upload/submission per bank | Upload once, shared securely with chosen lenders |

| Comparison | Manual – note-taking across bank counters | Side-by-side on one dashboard – full details |

| Expert guidance | Bank officer (represents the bank, not you) | Unbiased GradRight advisor (represents your interest) |

| Branch visits | Required for most public banks | Zero bank visits – fully digital |

| Timeline to sanction | 15-25 days (public banks), 7-15 days (private) | As fast as 10 days for NBFCs via GradRight |

200,000+ students have already used GradRight to fund their study abroad. Join them – free. Start on GradRight FundRight

Real Student Examples: What GradRight Looks Like in Practice

Collateral-heavy bank rules shut Rohit out five times. He moved his file to GradRight and received a competing offer within two days on a dollar-denominated loan that matched his budget. Rohit accepted, cleared the sanction in a week, and is now at Ohio State.

Vamsi’s middle-income background meant zero assets to pledge. FundRight surfaced an unsecured offer at a rate lower than most secured quotes elsewhere. He sealed the deal, booked his flight to Arizona, and joined the long list of students for whom ‘no collateral’ no longer meant ‘no chance.’

Harsha was overwhelmed by the education loan process. With the GradRight platform, she found clarity she could not get from visiting individual banks. With unbiased expert advice and multiple competing offers, she made a confident, informed decision.

When the Traditional Route Still Makes Sense

GradRight wins on speed, convenience, and competitive rates in most cases. But there are situations where going directly to a public bank still makes sense:

| Situation | Why Direct Bank Application May Be Better |

| Government subsidy eligibility (CSIS/PM-Vidyalaxmi) | These subsidies require you to apply through public banks. GradRight helps you identify eligible lenders, but the subsidy application happens at the bank directly. |

| Very small loan (below Rs 7.5 lakh) | For small unsecured loans under the standard IBA scheme, the public bank rate advantage (8.33-10%) vs NBFC rates (10-14%) may outweigh the convenience benefit. |

| Existing banking relationship with specific bank | If you have a strong existing relationship with a bank, they may offer better terms than the platform average for your specific case. |

| Specific lender required by scholarship program | Some scholarships specify approved loan partners. Check before assuming a comparison platform approach is better. |

In all other cases – which covers the vast majority of study abroad loan situations – the GradRight model delivers better rates, more options, less paperwork, and faster approval.

Also Read: Step-by-Step Guide to Securing an Education Loan for Studying Abroad

Related Education Loan Guides

Education Loan Providers in India – Top Banks, NBFCs, International Lenders

Compare Education Loan Interest Rates – All Lenders 2026

Step-by-Step Education Loan Guide for Study Abroad

Education Loan Processing Time in India

Education Loan Without Collateral

India Loan Bidding Platform – World First

GradRight vs LeapScholar: Compare Education Loan Assistance