Pursuing higher education dreams often comes with a significant financial burden. However, the Indian government recognizes the importance of education and offers valuable tax benefits to ease this burden.

This article explains the Section 80E education loan deduction available to students pursuing higher education abroad or in India. The most significant advantage of Section 80E is that there is no limit on the deduction you can claim for the interest paid on your education loan. Every rupee of interest you pay on your education loan during the financial year is eligible for deduction from your taxable income.

Section 80E Education Loan Tax Benefits 2026 – Quick Reference

| Feature | Section 80E Detail |

| What is deductible? | Only the interest component of your education loan EMI. Principal repayment is NOT deductible. |

| Upper limit on deduction? | None. Full annual interest amount can be claimed – no cap unlike 80C. |

| Duration | Maximum 8 assessment years from the year repayment begins. Or until interest is fully repaid – whichever is earlier. |

| Tax regime | Old (regular) tax regime ONLY. NOT available under new simplified tax regime. |

| Who can claim? | Individual taxpayers only. HUFs and companies are NOT eligible. |

| Whose education? | Self, spouse, children, or a student for whom you are the legal guardian. |

| India or abroad? | Both domestic and international higher education qualify. |

| Approved lender required? | Yes. Must be from a bank/financial institution under the Banking Regulation Act or an approved charitable organization under Section 80G. |

| Friends/relatives loans qualify? | No. Informal loans do not qualify regardless of educational purpose. |

| Eligible courses | Engineering, medicine, management (UG). Applied sciences, pure sciences, mathematics, statistics (PG). Also vocational courses. |

What Is the Section 80E Education Loan Deduction?

The 80E education loan deduction is a tax benefit that allows you to reduce your taxable income by the amount of interest you paid on an education loan during the financial year.

Section 80E is a valuable tax exemption designed to encourage individuals to invest in their own or their dependents’ higher education. The key principle: there is no limit on the deduction you can claim. Unlike Section 80C (capped at Rs 1.5 lakh) or Section 80D (medical insurance cap), Section 80E has no ceiling – you claim the full interest paid.

Eligibility for Section 80E Deductions

Eligible Individuals and Ineligible Entities

Individuals who have taken an education loan for their own higher education, or for the higher education of their spouse, children, or legal wards are eligible for the education loan exemption. Companies and Hindu Undivided Families (HUFs) are NOT eligible to claim this education loan deduction.

Purpose of the Loan

The education loan tax deduction is only applicable if the loan is taken to pursue higher education after passing the Senior Secondary Examination or its equivalent from any school, board, or university recognized by the Central or State Government.

The tax benefit applies whether the higher education is pursued in India or abroad. This education loan income tax benefit is applicable for full-time courses for:

- Undergraduate programs in: Engineering, Medicine, Management

- Postgraduate programs in: Applied sciences, Pure sciences, Mathematics, Statistics

- Vocational courses recognized by the relevant authority

Note: There is no restriction on whether the institution is public or private, or whether the study is in India or abroad. The loan must be for higher education post-10+2.

Approved Lenders Only

The education loan subsidy is only applicable if the loan is obtained from a financial institution to which the Banking Regulation Act applies, or an approved charitable organization established under Section 80G of the Income Tax Act. If the loan is obtained from friends or relatives, it will not qualify for the Section 80E tax benefit – even if the purpose is purely educational.

Only the Interest Component Is Deductible

The principal amount of the loan is not eligible for deduction under Section 80E. Only the interest component of the education loan can be claimed as a deduction. When your bank provides your annual repayment certificate, it will show the principal and interest components separately – only the interest figure goes into your Section 80E claim.

Old Tax Regime Only

The Union Budget 2023 made the new simplified tax regime the default choice for all citizens. The education loan exemption can only be claimed by individuals who have opted for the regular (old) tax regime. To opt for the old regime, you must file Form 10-IEA before filing your income tax return. You cannot avail of the Section 80E exemption under the new simplified tax regime.

Also Read: Education Loan Tax Benefits – All About Section 80E (GradRight)

Documentation to Claim Section 80E Deductions

To claim the tax deduction, you must obtain a loan sanction letter and certificate from an approved lender, clearly stating the principal and interest amounts paid on the education loan during the financial year.

The financial institution from which you took the loan will provide a certificate each year stating the specific amounts paid towards interest on the education loan. Although these documents are necessary, there is no need for immediate submission with your ITR. You must, however, maintain these documents for scrutiny if the Income Tax Department requires them.

- Loan sanction letter from the financial institution

- Annual interest certificate showing principal and interest amounts separately

- Keep records for up to 6 years post-filing in case of ITR scrutiny

- No separate schedule is required – declare the interest amount in the deductions section of your ITR under Chapter VI-A

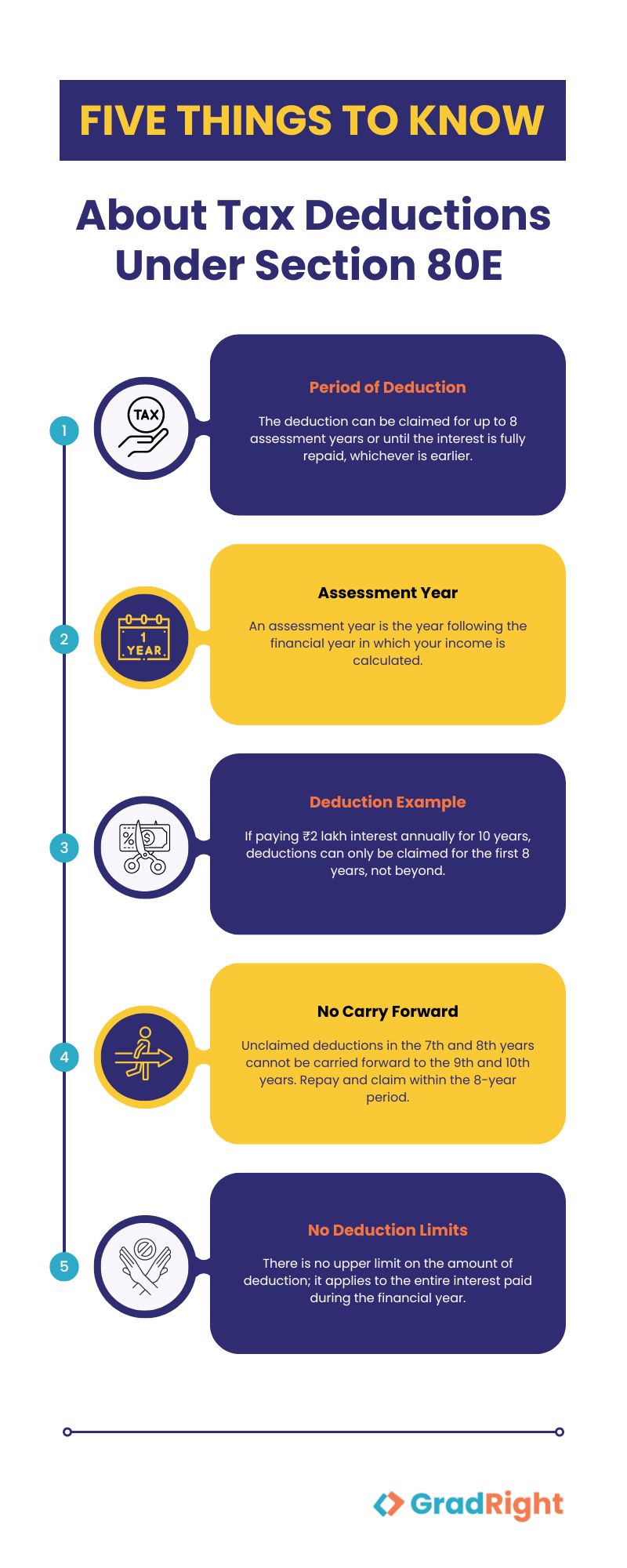

Period of Deduction Under Section 80E

The deduction can only be claimed for a maximum of 8 assessment years or until the interest is fully repaid, whichever is earlier. The assessment year is the year succeeding the financial year in which your income is calculated.

For instance, if you obtain an education loan for a four-year course, your repayments will typically begin 6-12 months after the completion of your course, depending on your employment status. You can only enjoy the tax benefit for the first 8 years, or until the interest is fully repaid – whichever is earlier.

Important: if you claim the deduction for the first 6 years and do not make any loan repayments for the 7th and 8th year, you cannot carry forward the deduction to the 9th and 10th year. Once the 8-year window closes, no deductions are applicable – the interest payable after the 8-year window cannot be reduced from your taxable income. Ensure you make loan repayments and claim the deduction within the eligible period.

Section 80E Tax Exemption Limits and How It Works

There is no limit on the deduction amount you can claim. Unlike Section 80C and Section 80D, Section 80E does not impose any cap. You can save the entire interest amount paid during the financial year as a deduction, regardless of the actual sum.

How the calculation works:

- First, calculate your gross taxable income after claiming other eligible deductions, if any.

- Second, determine the interest component paid on your education loan during the financial year.

- Third, deduct this interest amount from your gross taxable income. The remaining amount will be your taxable income for the year.

Example: if your gross taxable income after other deductions is Rs 10 lakh, and you paid Rs 1 lakh as interest on your education loan in that financial year, your total income for tax calculation purposes would be reduced to Rs 9 lakh (Rs 10 lakh minus Rs 1 lakh).

Section 80E Deduction – Year-by-Year Example

The following table (from the original article) illustrates how Section 80E savings work as your income grows over time:

| Financial Year | Total Taxable Income (no other deductions) | Applicable Tax Rate | Interest Paid on Education Loan | Taxable Income After 80E | Amount Saved via 80E |

| 2021-22 | Rs 6 lakh | 10% | Rs 1,80,000 | Rs 4,20,000 | Rs 18,000 |

| 2022-23 | Rs 10 lakh | 15% | Rs 1,50,000 | Rs 8,50,000 | Rs 22,500 |

| 2023-24 | Rs 12 lakh | 15% | Rs 1,20,000 | Rs 11,80,000 | Rs 18,000 |

This unlimited deduction potential under Section 80E can result in substantial tax savings, making it easier for you to manage the financial burden of pursuing higher education. The savings compound over time as your income (and therefore your tax bracket) grows.

Get an education loan from a lender that qualifies for Section 80E deduction. Compare 18+ lenders on GradRight. Compare Education Loans on GradRight

Should You Repay Your Education Loan Early?

Once you complete your degree and begin repaying your loan, you might have significant disposable income. You may have to consider whether to repay your education loan early or to invest your money. The answer depends on your financial goals, investment strategy, tax bracket, and expected returns.

Here are the guidelines from the original article:

- If you are in a higher tax bracket, consider extending the loan repayment period to the full 8 years. This strategy allows you to claim tax deductions for a longer time, which could reduce your taxable income each year.

- If the returns on your investments are likely to be lower than the loan interest rate, or if you prefer a more secure financial situation, repay your loan early.

- Compare the interest rate on your loan with the returns from investments. If your investments are expected to yield higher returns (post-tax) than the interest rate on your loan (accounting for the tax savings under Section 80E), invest your surplus income rather than prepaying.

- Repaying your loan early or on time can improve your credit score – advantageous if you plan to apply for other loans like a home loan in the future.

| Your Situation | Recommended Strategy |

| High tax bracket (30%), loan rate 10%, strong equity returns expected | Extend repayment to 8 years. Maximize 80E deduction. Invest surplus in equity for higher post-tax returns. |

| Lower tax bracket (5-10%), modest income | Repay early. The 80E benefit is small. Eliminate debt to reduce financial stress. |

| Loan rate above 12%, market returns uncertain | Prepay. Guaranteed 12%+ return on debt repayment often beats uncertain market returns. |

| Home loan planned in next 3 years | Repay on time (not early) to build credit track record. A good repayment history on a large education loan significantly improves home loan eligibility. |

Section 129 – New Income Tax Act 2025

Note: The Indian government introduced the new Income Tax Act 2025. Under this act, Section 80E (old act) has been renumbered as Section 129. The provision remains functionally the same: deduction for interest paid on education loans, up to 8 years, no upper limit, available for self/spouse/children/legal ward, from approved financial institutions only. When consulting a tax advisor or reading updated tax literature, you may see references to ‘Section 129’ – this is the same benefit.

FundRight – Find Your Best Education Loan

Here is something that could save you lakhs on the interest expense of your education loan – and ensure your loan qualifies for Section 80E. FundRight is a one-stop platform that simplifies the entire education loan process:

- Sign up on FundRight at gradright.com

- Create your student profile (15 minutes)

- Compare education loan offers from 15+ top Indian and international lenders – all from RBI-recognized institutions that qualify for Section 80E

- Upload your documents once

- Get help from a financial expert to negotiate the most suitable terms

- Get your loan approved in as few as 10 days

Also Read: Compare Education Loan Interest Rates – All Lenders 2026

Compare 18+ lenders on GradRight. All Indian lenders qualify for Section 80E. Best rates, free, 48 hours. Find Best Education Loan on GradRight

Related Education Loan Guides

Education Loan Tax Benefits – Section 80E (Detailed)

Compare Education Loan Interest Rates – All Lenders 2026

Education Loan EMI Calculator

Education Loan Repayment Tips That Actually Work

Education Loan Moratorium Period Guide

Lowest Education Loan Interest Rate for Study Abroad

GradRight vs Traditional Education Loan Process