Your new life in Dallas pays in dollars. Yet, every month you still wire INR 45,000+ to an Indian bank that charges 10%-13% floating interest and keeps your parents’ flat as collateral.

Refinancing that loan to a US-based lender is the obvious smart choice. But the real question is: which lender will actually touch an India-serviced loan and on what terms?

- Eligibility hoops: Will a lender accept your H-1B or STEM-OPT status and a loan originally booked in rupees?

- Direct payoff: Can they wire funds to SBI or Avanse and trigger a clean NOC so your collateral is released?

- Rate reality: Will the promised fixed APR really beat your current floating rate once fees and forex are done?

Finding the best lenders for refinancing student loans based in India isn’t quite as straightforward as we would like it to be. Thankfully, with the right guidance, the road can get much easier.

How Student Loan Refinancing Works in the US: The Market Reality

On the surface, refinancing feels like a simple trade. A new lender pays off your old education loan, and you start making one consolidated monthly payment in dollars.

- Payoff and replacement: Once you sign the final disclosure papers, the refinance lender must wait three business days before wiring funds (the required ‘right-to-cancel’ period).

- New repayment schedule: The moment the payoff posts, your old loan closes and a new amortization clock starts.

- Rate tweaks: Most lenders shave 0.25 percentage points off the rate when you enroll in AutoPay.

Two Tracks for Indian Borrowers

| Track | Your Loan | Lenders Available | Obstacles |

| Cross-border refi | Indian bank/NBFC (SBI, Avanse, Credila) | MPOWER Financing (active). Prodigy Finance (check availability). | Visa and employment checks. Fixed APR starts ~9.99%. Payoff letter plus SWIFT details required. |

| US-serviced refi | Loan already reported to US credit bureaus | Citizens, SoFi, Laurel Road, Earnest, ELFI | Most require US citizen/PR or cosigner. Loans in India don’t qualify. |

Pre-filter before you apply: Check visa/residency policy, whether the lender pays off India-serviced loans, and use soft-pull pre-qualification tools first.

Compare refinance offers from 18+ lenders – one profile, multiple competing bids, free. Explore on GradRight

India to US Refinancing: What Options Are Available in 2026?

As of June 2026, the cross-border refinance pool remains small but workable.

MPOWER Financing – The Single Fully-Active Cross-Border Refi Program

What they do: Pay your Indian lender directly via SWIFT. Maximum amount: $100,000; no prepayment penalty.

Who qualifies: US residents holding valid F-1 (OPT/STEM-OPT) or H-1B status, in full-time employment for at least 3 months, with citizenship from one of MPOWER’s 150+ supported countries. No cosigner, no collateral required.

Current pricing: Fixed APR ~9.99% with 0.25 pt AutoPay discount; terms 7 or 10 years. Verify current rate at mpowerfinancing.com before applying.

Paperwork: Payoff letter dated within 15 business days, degree and employment proof, government ID, Indian bank’s SWIFT/IFSC details.

Prodigy Finance – Check Availability Before You Bank on It

Prodigy briefly piloted a refi product. As of mid-2025, their public site focuses on new study loans. Treat Prodigy as a ‘maybe’ for 2026 – pre-qualify first and move on if the option isn’t live.

Bottom line: If your education loan still sits with SBI, Avanse, HDFC Credila, or any other Indian lender, MPOWER is the only fully operational cross-border refinance path right now.

Refinancing a Loan That’s Already US-Serviced

Many Indian students have debt already in dollars – either from a US in-study loan with a cosigner, or after a previous cross-border refi. If you’re in either camp, you can shop the broader US market for lower rates, cosigner release, or term adjustment.

Three filters to apply:

- Residency rules: Most brands want a US citizen or PR as primary borrower. SoFi is an exception – check their live eligibility page for current visa-holder policy.

- Credit and income thresholds: Expect hard minimums around $35,000 salary and a mid-600s credit score.

- Cosigner release language: If you needed a cosigner during school, confirm the new lender offers a clear path to release them later.

Top US Refinance Lenders 2026

Rate disclaimer: All rates below are lowest advertised fixed APRs as of June 2026. With the Fed funds rate at 4.25-4.50% (held since December 2024), floor rates are higher than the 2021-22 lows. Your actual rate depends on credit, income, and term. Always verify on each lender’s website on the day you pre-qualify.

| Lender | Visa / Residency | Cosigner | Fixed APR (June 2026) | AutoPay Discount | Stand-out Feature |

| SoFi | Select visa types – verify during pre-qualification | Optional if income/credit qualify | 0.25 pt | Career coaching; unemployment protection | |

| Citizens Bank | Non-citizen OK with US citizen/PR cosigner; loan must be US-serviced | Required for non-citizens | 0.25 pt | Cosigner release after 36 on-time payments | |

| Earnest | US citizen/PR only | Not offered | 0.25 pt | Custom term length to exact month | |

| Laurel Road | US citizen/PR only | Optional | 0.25 pt + 0.25 pt with linked checking | Extra discounts for healthcare grads | |

| ELFI | US citizen/PR only | Optional | 0.25 pt | Dedicated refi advisers |

Second refinance timing: A second refinance usually makes sense 12-24 months after your first one – enough time to build credit, establish stable US income, and watch the rate market.

Rupee vs Dollar: What 2026 Interest-Rate Numbers Really Show

India’s Floating Rate Reality

SBI education loans start around 10% for a standard master’s borrower. Private NBFCs run even richer spreads – Avanse pegs its base rate at 14.55%+ (final price is base + spread), resetting every time the RBI moves.

Because the rate floats, every repo-rate change pushes your EMI up or down – and the rupee’s long-term slide against the dollar amplifies the hit.

US Refinance Benchmarks

With the Fed funds rate at 4.25-4.50% (held since December 2024 after three cuts in 2024), private refinance fixed APRs for strong profiles range from approximately 5.24% to 9.99%. Variable offers start lower but carry SOFR-linked risk. AutoPay discounts of 0.25 pt are standard; Laurel Road adds an extra 0.25 pt with a linked checking account.

| Loan Location | Typical 2026 Rate | Rate Type | Currency Risk |

| India-serviced (SBI, Avanse, etc.) | ~9%-15% | Floating (linked to RBI moves) | Rupee depreciation widens true cost in USD |

| US refinance (private lenders) | ~5.24%-9.99% | Mostly fixed (variable optional) | None – borrower earns and repays in dollars |

Take an INR 30-lakh loan at 11% floating. Rolling that into a 7-year US refi at 7.5% fixed cuts about ₹6,000 (≈US $70) off each monthly payment and removes the collateral from your parents’ property file.

Also Read: How International Students Can Refinance Education Loan in the US

Also Read: Student Loan Refinance Rates 2026: What You Need to Know

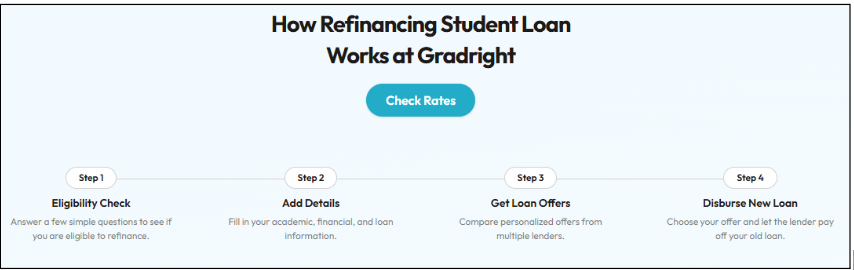

How GradRight Can Help You Refinance Your Student Loan in the US

GradRight flips the search upside-down by letting lenders bid for your profile instead of the other way around.

You’ve seen the gap between rupee-floating and dollar-fixed rates. Now comes the hard part: finding the best lenders for refinancing student loans in the US.

GradRight flips that search upside-down by letting lenders bid for your profile instead of the other way round.

GradRight is partnered with more than 15 domestic and international lenders. The list includes Indian banks (SBI, ICICI), NBFCs (HDFC Credila, Avanse), and global players that refinance in US dollars.

Once you submit a single profile, its matching engine screens your visa status, credit, income, and existing loan data, then surfaces only the lenders that can legally and competitively pay off your current loan.

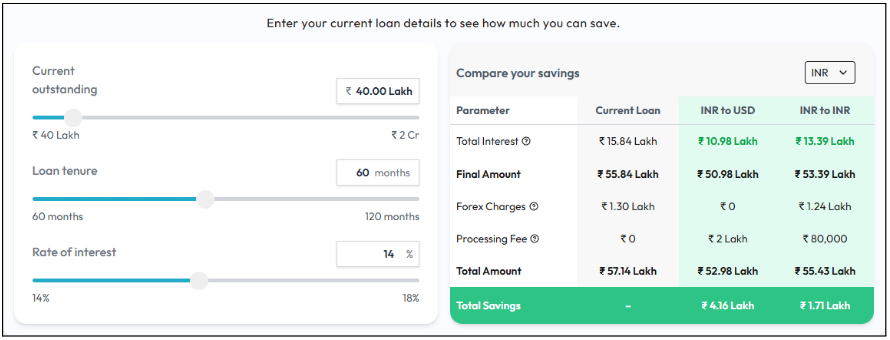

GradRight’s built-in calculator shows the rupee-to-dollar math before you commit. Converting a ₹25-lakh, 10-year loan from 11% INR to 6% USD, for example, cuts roughly ₹4.1 lakh in total interest.

Because the platform is free to students (lenders pay a success fee), there’s little downside to running your numbers.

More importantly, it prevents the common misstep of applying to ten lenders only to learn—after hard credit pulls—that nine of them don’t refinance India-serviced loans.

Refinance your education loan – one profile, 18+ competing offers, free. Start on GradRight