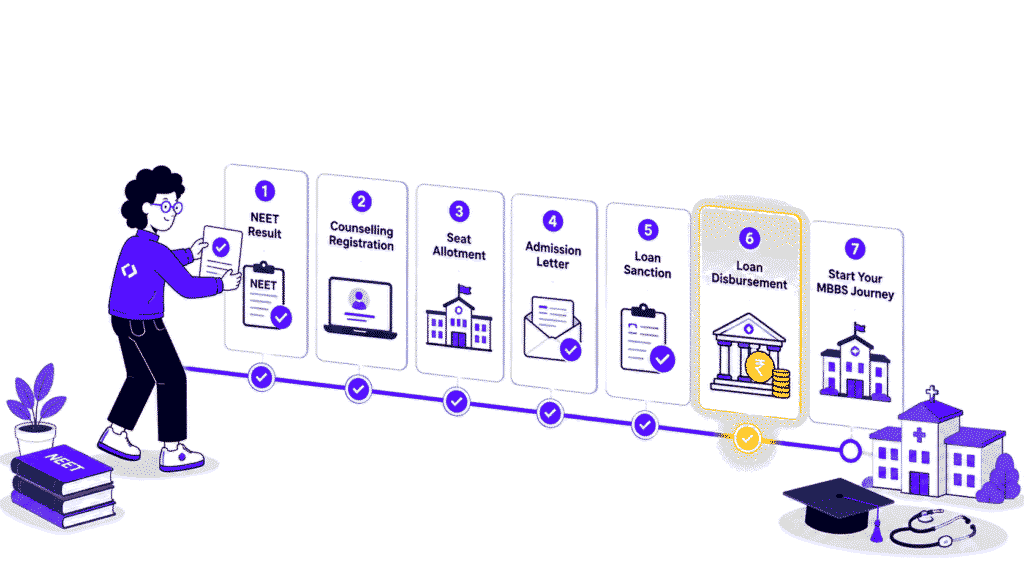

The GMAT results are out. With a score of 310+, you are sure that at least five of the top 20 US universities would accept your application.

The other big question surfaces: How do you fund the program?

You’ll need $40,000 for a two-year study-abroad program. That translates to a whopping ₹30 lakhs.

The cost of education is not your problem. After all, a degree from a well-known university abroad improves your employability by many folds. It could even be the ticket to settling down abroad with a permanent visa.

The problem is this. Education loans for studies abroad are tough to crack, particularly using traditional search tactics (ask a senior, ask a consultant, visit the neighborhood bank).

The loans market is disorganized, correct information is inaccessible, and sellers (lenders) enjoy inordinate leverage over buyers (students).

We developed this guide to answer these questions:

- What’s the standard funding strategy for most students?

- What are the loopholes and knots in the traditional loan-search process?

- How does FundRight categorically eliminate all these problems?

- How can you keep stress-gremlins at bay, as you search for your best international education loan?

- How, and where to find a scholarship or grant suitable for you?

Let’s begin.

How to secure sufficient funds for study abroad?

Most students rely on a hybrid strategy—fund a part of the education by scholarships or grants, and the remaining by an education loan.

Scholarships and Grants

This is so obvious, that we don’t even mind repeating it.

A scholarship is a financial aid granted to a student. It is based on merit. A grant is however need-based and might not be reserved only for the brightest students.

Large scholarships are, however, elusive. Stiff competition, lower probabilities. Any scholarship that pays for the entire cost has thousands of applicants from around the world.

Many scholarships are targeted (e.g. scholarships for Commonwealth students, scholarships for women, scholarships for students of color, scholarships for LGBTQ+ students). Such a targeted scholarship could ease your scholarship-search burden.

Who sponsors these scholarships?

Government

The first is government scholarships.

The most suitable example is the Fulbright Student Scholarship, a highly prestigious award. It is funded by the United States Cultural Exchange Programs. Of the 8,000 Fulbright Scholarships awarded every year, 4,000 are for international students.

Another example is the GREAT Scholarship offered by British Council that offers £10,000 to a student pursuing study in 41 impaneled UK universities.

Institution

An example:

- 1 in 5 students at Harvard pays nothing.

- 55% receive some amount of financial relief.

- In the 2020-21 academic year, 47% of students at Oxford received full or partial funding.

The All Souls Hugh Springer Graduate Scholarship, Clarendon Fund, Oxford-Reuben Scholarship, and at least a dozen more scholarships are applied-to automatically when you apply to this august institution.

Others

Besides governments and institutions, private individuals and companies also offer scholarships. Some examples:

- The Tata Scholarship offers funds to Indian students who have been accepted for undergraduate studies at Cornell University.

- The C. Mahindra Scholarships pay ₹ 4-8 lakhs to deserving students who have secured admissions abroad.

- The Narotam Sekhsaria Scholarships provide up to ₹ 20 lakhs to scholars studying at 55 universities.

Student Loans

Education loans for studies abroad are a popular retail banking product in India.

Public sector banks, e.g. State bank of India, Punjab National Bank, Bank of Baroda, and Canara Bank, offer loans for 6.9% to 9.95%.

ICICI Bank offers loans of ₹ 1 crore and HDFC Bank offers ₹ 45 lakhs.

Availability isn’t the problem. Still, you can’t expect to saunter into a bank branch, declare your funding requirement, and enjoy small talk with the manager while a staffer readies your dossier. In reality, you’ll probably spend weeks in the loan-search process. You’ll:

- Visit multiple bank branches

- Flitting across bank branches

- Talk to half a dozen loan agents every other day

- Lose your sanity blocking unsolicited callers

- Get used to ceaseless waiting without updates from bank staff

- Eventually, be disappointed by an arbitrary application rejection

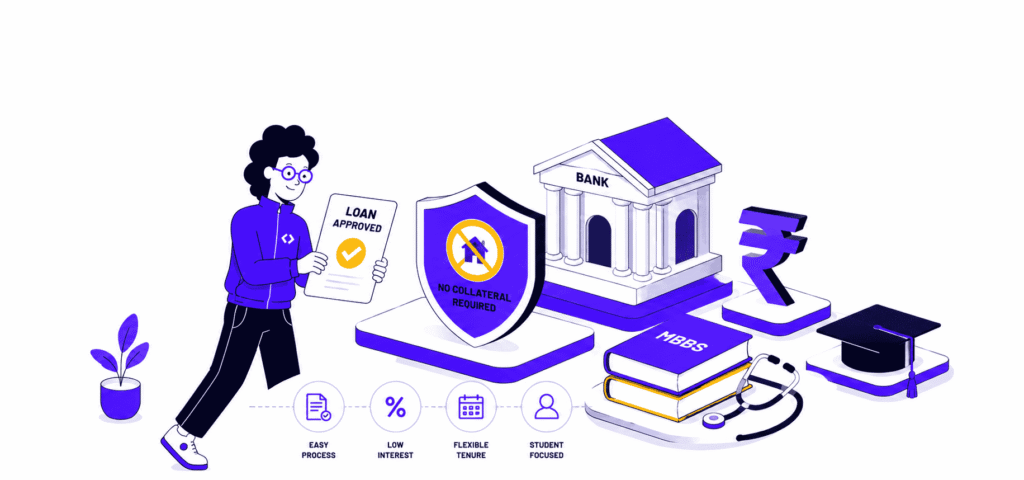

Financing brings down the curtains on this obscene tragedy.

Think of FundRight as your ticket to your best student loan for study abroad. An affordable, favorable, quick, zero-hassle, and transparent education loan, from the most reputed lenders, domestic and international.

Is FundRight different from what you’d do usually–apply for an education loan at multiple banks? Yes, and here’s how:

- On FundRight, you don’t chase banks; lenders bid for your loan.

- One profile connects you to 14 lenders (we add more every month)

- Your sensitive information remains inaccessible to lenders until you show interest in their offers; bye-bye spammers

- FundRight is free. No sneaky charges, no misinformation, no secrets. 100% free.

- Not only do you get the choicest offers, but also a team of experts who help you select the one that is best for you.

There’s more.

Study loans for abroad—stuff you ought to know

Moratorium

Usually, when you take a loan to buy a car or house, the repayment starts immediately.

That is a problem for students. They have to complete their education and only then can begin to repay the loan from their salary.

Hence, there is a gap between receipt of the education loan for abroad and the date repayment is going to commence. This is known as the moratorium period.

Tenures

You could choose to repay the student loan for study abroad in six years. Again, you could, but might not be able to, unless you net a substantial starting salary. That is why banks offer tenure of 15 years in most cases.

This tenure includes the moratorium period.

Co-signer

Banks hate defaults.

That is why they insist on co-signers for education loans for studies abroad. A co-signatory guarantees the repayment of the loan in case you default.

Usually, a family member is the co-signatory.

The co-signer needs to have a steady source of income and have solid roots in society.

Collateral

Education loan for studies abroad without collateral is possible but unlikely.

If the co-signatory has a high net worth, large income (as shown by ITR for the past few years), and owns immovable property, the bank might not ask for collateral.

Otherwise, they might require a sum to be held in a fixed deposit at the branch or demand a property deed as collateral.

Do bank loans have any drawbacks?

Any kind of loan carries an interest component on repayment. Over years, that might accumulate and become too large to repay. A loan of ₹40 lakhs is substantial, and it is not ideal to begin life with such a burden.

However, for further education, it is necessary and an acceptable liability.

The biggest problem with banks is that they are unwilling to finance education that they deem is unprofitable.

While a student of Comp Sci might easily get a foreign education loan if they were to study at the University of Southern California, someone wanting to do an MBA in Finance from Durham University will be refused.

The rationale? There are too many MBAs fighting over jobs and Durham University lacks name recognition.

While that holds water from the lender’s point of view, it is a sure-fire dampener for the student.

FundRight – How to find your best education loan for study abroad?

The Gordian Knot.

Ancient Greek lore has it that Phrygians wanted a king. Anyone wanting to be the anointed one would have to untie an inextricable knot.

Many failed. Alexander arrived and cut through it with his sword.

FundRight is our attempt to do what Alexander did, to the education finance industry.

From seller-advantage to buyer-advantage

FundRight lets banks bid to provide you with a loan.

If you were running after a lender for a loan, you lose momentum. Let them come to you and put their money where their mouth is.

When you choose FundRight for your international-education loan, you give yourself the best opportunity. Because when banks compete for your loan:

- they release their best offer, which could mean a cheaper loan, abd

- they don’t rely on myopic opinions of your academic and career prospects, which means a higher approval percentage.

14 lenders, one loan application

As a student, you have to create a profile, and then FundRight does all the heavy lifting.

The toughest part of getting an education loan is cooling your heels in grubby banks lobbies waiting to meet the manager.

Even when it happens, he has a surly expression and wants to be thanked. You did the hard work and burned the midnight oil! Your father is the guarantor who would pay back every penny if needed. Why does the manager need to be thanked?

None of that with FundRight.

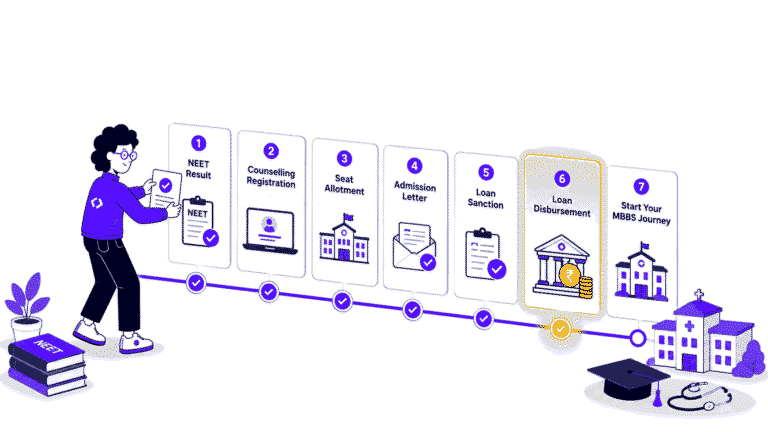

From profile to loan, in 2 days

The process is so easy, you could wiz through it half-asleep.

- Register on FundRight

- Complete your profile

- Receive bids for your loan

- Compare and select

- Upload your documents

All done; now watch as the lender does the rest until the money is disbursed.

All done, within 2 days!

All done, without trudging miles from bank to bank in a searing Indian summer.

Summary: How to eliminate stress from your education loan search?

Do these 3 things.

- Begin early.

- Don’t chase banks, let banks bid for your loan.

- Know your scholarships and grants options.

This, and some patience, will sail you safely across the choppy waters of the international education loan search.