With tuition fees averaging between C$20,000 and C$30,000 per year, Canada offers a more cost-effective study abroad option for students, compared to the USA, UK, and Australia.

But even with those lower costs, studying abroad can be expensive. You’ll need money for rent, food, textbooks, and everyday living expenses.

And if there is no other means, education loans can help you cover these costs.

This blog is your one-stop guide to education loans for studying in Canada. We’ll explore interest rates, courses, requirements, banks, and other benefits of education loans.

About studying in Canada

Canada boasts a quality education. One proof is the higher-than-average graduation rate, which is 79%, compared to the average of the Organization for Economic Cooperation and Development (OECD), which is 76%. This graduation rate reflects the country’s commitment to providing accessible, high-quality education to its students and many international students as well.

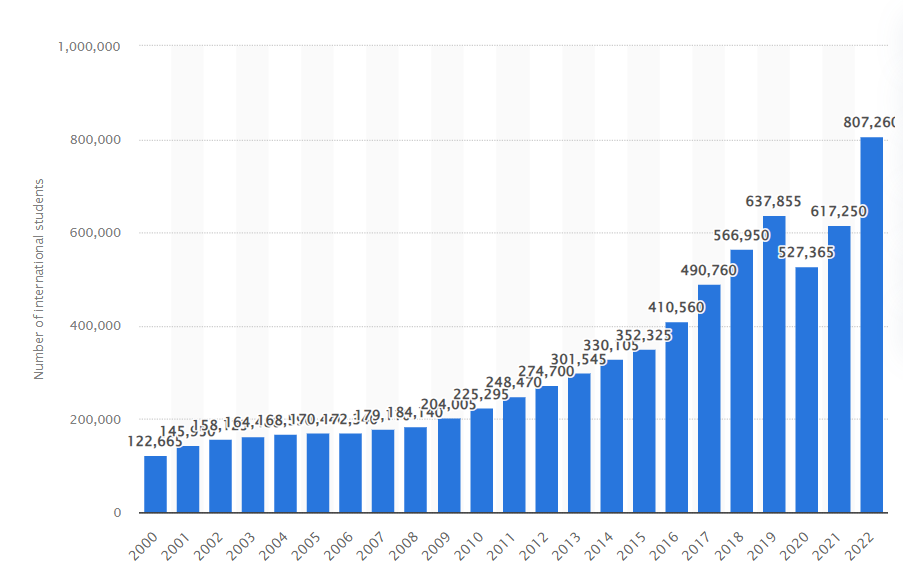

By 2022, there were 807,260 international students in Canada–a number that showcases the country’s appeal as a global education hub for pursuing higher education.

Many other factors contribute to the appeal of studying in Canada, including the ease of obtaining a Permanent Residency (PR), the availability of post-graduation work visas, numerous scholarships, and more.

And here’s a bonus: Canada has a large international community, which makes it easier for students from all over the world to settle in and study in Canada.

Also Read: A guide to IELTS score for Canada

Education loan for studying in Canada

Studying in Canada means you’ll need to pay for the tuition fee and the living costs for the duration of your stay, all of which add up into significant amounts, particularly for Indian students.

Nevertheless, the high quality of education, strong industry connections, and practical skills acquired during studies help graduates from Canadian universities find jobs more easily.

This means the money you put into your studies in Canada pays off in the long run.

If you’re worried about the cost, don’t forget that an education loan for studying in Canada could help you manage those expenses.

Various banks and financial institutions offer education loans for Canada. These also include special loans for different programs, such as education loans for MBA in Canada or education loans for MS in Canada.

Also Read: Compare Education Loan Interest Rates of Top Banks in India 2025

Application process for education loan in Canada for Indian students

Once you get the admit card from your university (or you can start even if you have your GRE, IELTS, or similar test scores), you can begin the application process for getting an education loan for Canada.

Step 1: Figure out the type of loan you want

There are two types of loans for international students: a secured loan (collateral loan) and a non-collateral education loan for Canada.

You can easily compare both types of loan options from 15+ top lenders (Indian as well as international) on FundRight. We explain how it works in more detail later in this guide.

Step 2: Research banks

If you are Indian and considering an education loan for Canada in India, list different banks based on competitive interest rates, loan processing time, processing fees, and lower repayment terms and duration.

Also, check all the expenses covered by an education loan for studying in Canada.

Step 3: Fill out the loan application form

Next, download the application form on the bank’s website and fill in all the necessary details in the application form. This includes the cost of studying in Canada, estimated tuition fees, and other relevant information.

Step 4: Submit required documents

Once you’ve filled in all the details, submit the required documents to secure your education loan for studying in Canada. This includes providing the admission letter from your Canadian university, along with any other documents requested by your chosen lender.

Step 5: Complete the KYC process

Follow the instructions provided by your lender to complete your registration and the Know Your Customer (KYC) process, typically using your Aadhar number.

Step 6: Loan application acknowledgment

After submitting your application, the bank usually takes 1 to 2 days to acknowledge your application.

Step 7: Loan disbursement

The bank will disburse one semester or year’s tuition fee directly to your Canadian university upon approval. Note that if you’re getting your loan from an NBFC, they will disburse the loan amount into an Indian loan bank account instead of directly disbursing it to the university.

Step 8: GIC requirement

At the same time, you’ll need to release approximately CAD 20,635 (around ₹12,17,619) towards the Guaranteed Investment Certificate (GIC) and retrieve the GIC Certificate.

Eligibility for education loan for studying in Canada

Some of the eligibility factors that banks consider are:

- You must be an Indian citizen.

- You must be above 18 years of age.

- If you are a minor, you’ll need a guardian to sponsor your education and stay in Canada.

- You should have a seat or proof of admission to a foreign university.

- You should be enrolled in a professional course.

How to choose a bank for a study loan in Canada?

When looking for an education loan for studying in Canada, picking the right bank is key.

Interest rate

The interest rate is a critical factor. A small difference can lead to significant savings. Therefore, compare the offerings from various banks. For instance, look into the HDFC Credila education loan for Canada and the SBI education loan for Canada, both of which provide competitive interest rates, and go for the deal that’s light on your pocket.

Tax benefits

Did you know that loans from Indian banks can help you save on taxes? Loans from scheduled Indian banks are eligible for tax deductions under Section 80E of the Income Tax Act 1961.

Under Section 80E of the Income Tax Act, you can get deductions on the interest you pay. You can avail of tax deductions for up to 8 consecutive years, starting from the year you take the loan.

Eligibility and documents

Banks assess your academic background, creditworthiness, co-applicant details, and family income to know if you’re a good match for a loan.

They also check out the course and college you’re considering, whether it’s an education loan for MBA in Canada, for an MS in Canada, or for a PG diploma in Canada.

And yes, paperwork is a big deal here. So ensure you have all your documents, such as mark sheets, proof of income, and a confirmed admission letter.

Costs covered

Ask your lender about the coverage of costs in education loans for studying in Canada, including tuition fees, lab charges, personal expenses, and travel fares.

This is particularly important for education loans for diploma courses in Canada, as these programs are shorter and often require significant upfront payments.

Prepayment terms

If you can pay back your loan sooner, that is, 6 months after your course is completed, you’ll save on interest. But some banks might charge you for this. Hence, check with your bank if there are any penalties for early repayment.

Loan processing time

Processing time can affect your admission and visa application process. Check if your bank offers faster processing times, which can ease your visa application.

Factors to consider when applying for your education loan

Before applying for an education loan for studying in Canada, you should have a clear roadmap to how much you need and can pay from your end for your education in Canada.

Here are a few important factors to keep in mind before applying for an education loan for Canada:

- First of all, finalize the graduate course you’d like to study because it affects the loan amounts that can vary depending on the course and institution. For example, an education loan for MS in Canada might have different terms compared to an education loan for a PG diploma in Canada.

- You must take an English proficiency test beforehand and score above 6.5 to qualify for better loan amounts to study in Canada.

- Identify and keep a financial co-applicant if you are applying for a non-collateral education loan for Canada.

- Understand if your loan requires collateral and what types are accepted.

- Apply for the loan three months before the visa interview date and estimate the time of disbursement.

- Check if your loan provider covers all the other expenses, such as health insurance, examination fees, books and equipment costs, and travel expenses.

Documents required for securing a student loan in Canada

Here’s a list of the documents needed to secure a student loan, which banks usually require to process an education loan.

- An offer letter is given by the university (proof of admission)

- Loan application form (filled)

- Passport size photographs

- Statements of borrowers’ bank accounts (last six months)

- Original education certificates/mark sheets

- Income proof of the financial co-applicant

- Documents of qualifying exams (GMAT, TOEFL)

- Residential Proof of student and co-borrower

- IT returns of co-borrower

- PAN card and other identity proofs of student and co-borrower

- Passport copy

- Details of assets and liabilities of parents/co-applicants

Things to remember when applying for Canada education loans

Here, we delve into three important elements affecting how you plan and manage your finances before and after your studies.

Moratorium Period

This is a grace period during which you don’t need to make any repayments. The length of this period varies by lender and often continues for a while after you finish your course.

Loan Margin

Banks usually do not fund the full cost of education. For example, many public sector banks cover up to 90% of total expenses, meaning you’ll need to provide the remaining 10%.

Impact of Exchange Rate

Education loans for studying abroad are typically disbursed in the currency of the study destination if you borrow from an international lender like Prodigy Finance. Therefore, changes in the exchange rate could impact the final amount you receive. In case you’re borrowing from an Indian bank, the amount is disbursed in INR.

Collateral rules for Canada education loans

The requirements for a collateral and non-collateral education loan in Canada can vary depending on the lender and the loan amount.

For loans that exceed ₹7.5 lakhs, lenders usually require tangible assets as collateral security. This could include property, fixed deposits, or other valuable assets that can secure the loan amount.

However, there are options for students who may not have collateral to offer. Certain lenders offer education loans without collateral for Canada.

For education loans in Canada for international students, having a co-signer or co-borrower, typically a parent or guardian, is a common requirement. The co-borrower is responsible for repaying the loan if the student cannot.

Also Read: Collateral Vs Non-Collateral Education Loans For Abroad Studies

Role of a co-applicant in Canada education loan

A co-applicant plays a crucial role in securing an education loan for study in Canada. A co-applicant is an individual who agrees to repay the loan if the borrower is unable to do so.

Typically, this is a parent or guardian, but it can also be a relative who meets the lender’s eligibility criteria. The co-applicant provides additional security for the loan.

Their creditworthiness and financial stability are key factors that lenders consider when assessing the loan application.

Indian Banks and NBFCs offering loans to study in Canada

Securing a loan can be challenging with endless waiting hours, unlimited paperwork, and the uncertainty of loan approval. It’s enough to make anybody lose their sanity.

That’s where FundRight steps in.

FundRight, a specialized platform that helps and guides students to take their first-ever education loan without any hassle or confusion.

Here’s how FundRight helps:

- Wide Network: The platform connects you with various lenders from India and abroad.

- Competitive Offers: Lenders on FundRight bid to provide you with loan offers.

- Quick Results: With FundRight, you can receive loan offers in just two days.

- Cost Savings: FundRight can help you save up to ₹23 lakhs compared to traditional loan options.

Join the 60,000 students who found their best loan with FundRight. Check your offers.

FAQs

1. Can students from India get a loan to study in Canada?

Yes, students from India can get loans to study in Canada.

2. How to get an education loan for studying in Canada?

Firstly, research and compare various financial institutions, their interest rates, terms of study loans, eligibility requirements, repayment options, etc. Then, check eligibility and submit all the necessary documents. Once you submit your application, the banks will review it and provide you with a final decision within 10-14 working days.

3. Do you need a good credit score to get a loan for studying in Canada?

Yes, you need a good credit score, but some loan providers might look at your future job prospects instead of your credit score.

4. Do I need someone to sign the loan with me?

Yes, for Canada, you need someone to co-sign the loan if you’re borrowing from an international lender like Prodigy Finance. But if you have someone with good credit to sign with you, you might get a better interest rate on your loan.

5. Can I get a loan for studying in Canada without offering something as security?

Yes, there are loans available that don’t require you to offer something as security, especially if you have good grades or good job prospects.

6. Can I apply for a loan to do an MS in Canada while I’m still in India?

Yes, if you’re in India, you can apply for a loan to do an MS in Canada until your visa interview date.