Studying in the US is a dream many Indian students share. But let’s face it, the costs are enough to make your head spin. We’re talking tuition fees that could swallow all of your savings.

However, the aspiration to study in US and make it big in life always drives you to overcome these hurdles.

That’s why many Indian students take an education loan for USA. If you plan to apply for an education loan to fund your studies in the USA, this guide will help.

Studying in the USA

Studying in the USA opens a world of endless opportunities.

It is home to prestigious universities, such as the Massachusetts Institute of Technology (MIT), Stanford University, and Harvard University. As the biggest economy of the world, it’s a land that offers ample opportunities to students. The USA is also home to the world’s leading companies in all industries.

No wonder America’s valuable and quality education is a magnet for students globally.

Also Read: How Can Indian Student Get A U.S. Education Loan?

The cost of education

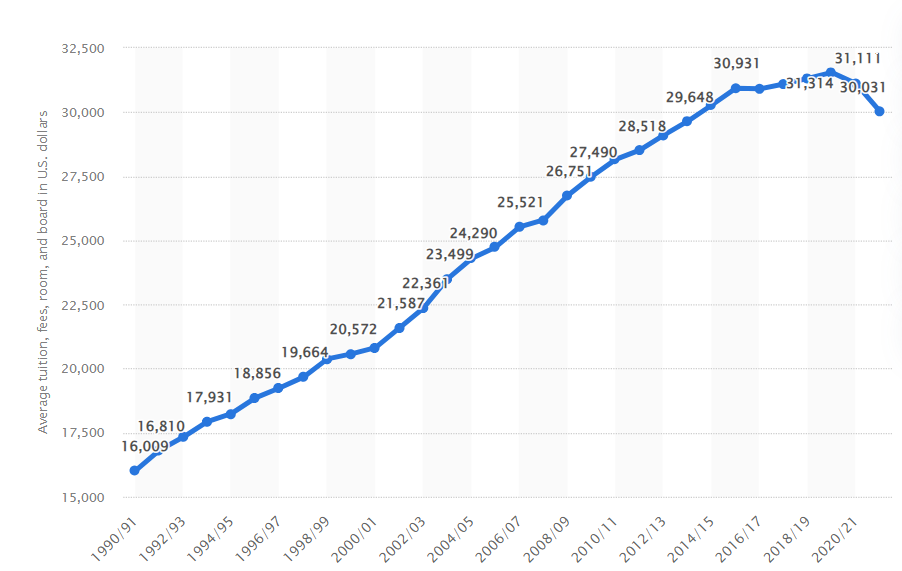

Here’s the catch – getting that top-notch education doesn’t come cheap. The tuition fee is the biggest part of the expense. Apart from tuition fees, you must consider accommodation (on/off campus), and transportation costs.

On average, students have to spend approximately $30,031 for tuition, fees, room, and board, per year (for undergrad courses), as per data available for 2022. In INR, this amount (for four years of education) crosses ₹1 crore.

The graph below shows the trajectory of these costs over the past thirty years. Chances are you’d have to spend even more in 2024 and the years beyond.

However, students need to put the expenses in perspective by also checking the ROI on the education.

The role of education loans

Enter education loans for studying abroad. They make a foreign education viable for anyone with the aspiration, and give students the chance to pay back the loan from their future income.

These loans have become a lifeline for many, covering everything from tuition fees to living expenses. However, it’s not all smooth sailing.

Taking on debt without a proper plan to repay can land you in a tough spot. The student debt in the USA is an often talked about problem, globally. A shaky job market can aggravate the anxieties of students.

It’s natural for students to wonder whether an education loan for studying abroad in the USA is a meaningful investment.

Also Read: Compare Education Loan Interest Rates of Top Banks in India

Is an education loan for studying abroad worth it?

In 2022, over 465,000 Indian students went to the US for higher studies, a 35% increase from the previous year.

Despite rising costs, many Indian students still choose the USA for their education. Why? The allure lies in its top-tier universities and exciting career opportunities.

Even without substantial financial means, Indian students can pursue their dreams. Education loans provide access to the USA’s adaptable education system, diverse culture, globally recognized degrees, innovative coursework, and excellent job and internship prospects.

So, an education loan for studying in a reputed university in the USA is definitely worth it.

Ready to take the next step? Let’s understand the application process for getting an education loan.

Also Read: Education Loan in India: Interest Rates, Process, Best Banks & More

Application process for getting an education loan for studying in the USA

Securing an education loan for an MBA in the USA or any other course requires careful planning and research.

Follow these steps in the process to make an informed decision.

Step 1: Understand your eligibility

Before you begin the application process, you must meet the eligibility criteria of securing an education loan in the USA for Indian students.

Step 2: Choose the right bank

All major Indian banks offer student loans for international studies, with amounts up to ₹2 Cr. The loan amount highly depends on your chosen university and the respective course. Compare factors like interest rates and loan terms to find the best education loan for studying in the USA for Indian students.

Some of the well-regarded options are from lenders like HDFC Credila, Prodigy Finance, State Bank of India, and more.

Step 3: Gather the necessary documents

Prepare and gather all the necessary documents for your loan application. Here’s a representative list. Note that the complete documents list depends on the bank you’re applying to for the loan.

Documentation Required to Apply for a Loan

For the Student:

- Completed application form

- Photo ID proof

- Proof of residence

- Passport-sized photograph

- Proof of admission or entrance exam scores (e.g., GRE, IELTS, GMAT)

- Fee structure document

- Salary slips (for experienced candidates)

- Visa copy for overseas education (or pre-visa documents if visa not yet received)

- Academic documents

- Income proof, if applicable

For the Co-applicant:

- Completed application form

- Last 6 months’ bank statements, if required

- Photo ID proof

- Proof of residence

- Passport-sized photograph

- Relationship proof

- Balance fund proof

- Residence ownership proof

- Collateral documents, if applicable

Step 4: Apply for the loan

Once you have all your documents in order, you can apply for the loan. This is what the application process is like for most education loans.

- Make sure you have all the necessary documents ready.

- Decide whether you want to apply for the loan online or by visiting the bank in person. Both methods are usually available.

- Complete the loan application form carefully. Double-check for accuracy to avoid any delays in processing.

- Along with the application form, submit all the required documents. This can usually be done online or in person, depending on your preference.

- Once you submit the application, the bank will provide you with an application number. This number will be your reference throughout the loan process.

- Use the application number to track the status of your loan application. This will help you stay informed about any updates or requests for additional information.

Step 5: Wait for the decision of the application made

This could be an approval or a rejection. Rejection of a loan application may be due to reasons around university ranking, poor academics, low cosigner income, low credit scores, or invalid collateral etc

Step 6: Understand the loan sanction terms

Once the loan is approved, understand the sanction terms. Loan sanction terms would include all the terms and conditions briefly about the loan. This could include loan amount approved, margin money, processing fee charges, all additional charges, repayment tenure, moratorium period, post approval conditions etc.

Step 7: Finalize the loan

The loan approval may be from just one bank or you may have your loan approved from multiple banks. After comparing all the approved loan options, the best one is to be finalized. This finalization is confirmed on payment of processing fee charges. Once you pay the processing fee, the bank offers the loan sanction letter which is a critical document used for either securing your i20 or for visa later.

Step 8 : Wait for loan disbursement

The loan amount is disbursed closer to your fee payment deadline or when you leave the country. This step would involve signing a bunch of loan documents & the loan agreement. Disbursement is usually done semester-wise or as the college seeks.

Eligibility for education loan for USA

Before applying for an education loan for studying in the USA, it is important to be eligible on the following criteria:

- To apply for a loan to an Indian bank or NBFC, you must have a co-applicant. You and your co-applicant must be Indian citizens. When you apply for a loan with an international lender, you can also get a loan without a cosigner.

- You must seek admission to technical or professional study programs that are job-oriented in nature.

- You must secure an admission at a university in the USA or you must have some entrance test scores (GRE/GMAT/IELTS/TOEFL) valid for US

- You should be above 18 years of age.

- If you’re under 18, your parents must apply for the loan on your behalf.

How to choose a bank for an education loan for studying in the USA?

When it comes to education loans for courses like an MS in the USA for Indian students, selecting the right bank is crucial.

Here’s what you need to consider for securing an education loan for studying in the USA:

Interest rate

The interest rate is a crucial factor as it determines the total cost of your loan. Check whether the banks are offering fixed or variable interest rates as it directly impacts your repayments over time. For instance, State Bank of India (SBI) offers student loans with a fixed interest rate of 11.15%(secured loans), while HDFC Credila’s rate is variable and starts from 11% for unsecured education loans.

Coverage

Check what the loan covers. Does it include tuition fees, living expenses, travel costs, and other expenses like books and equipment? Many banks’ education loans cover tuition fees, exam or lab expenses, travel, safety deposits, and miscellaneous expenses. Public sector banks usually have 10-15% of margin involved which you may have to furnish from your own savings, while private banks/non banks can cover 100% of the cost of education.

When you apply for a loan, check what expenses it covers. Ideally, you’d want your education loan to cover not only the tuition fees, but also living expenses, travel costs, books, and equipment.

Note that some banks require you to contribute a certain amount towards your education expenses, known as the loan margin. Public sector banks usually require you to cover 10-15% of the expenses from your own savings. This margin might need to be paid upfront (to the educational institute), or some banks may allow it to be spread out over the loan disbursement period.

In contrast, private banks and non-banking financial companies (NBFCs) often cover 100% of the cost of education. Clarify these details with your bank.

Processing fee

Processing fees can be a fixed amount or a percentage of the loan amount. Clarify this aspect for each lender’s loan offer, and look for lenders with low processing fees.

Income tax exemptions

Some banks offer tax benefits under Section 80E of the Income Tax Act, which can help reduce your or your parents’ taxable income. Check with the bank if such exemptions are available.

Repayment terms

Consider the repayment terms and check which bank offers a generous repayment period. Typically, repayment tenures can range from 5 to 15 years. Public sector banks often offer flexible repayment terms, sometimes extending up to 15 years. Most banks also include a moratorium period in your repayment terms, which is a grace period after you end your studies, during which you don’t have to make any payments. Note that the interest keeps on accruing for this period.

Collateral

Some banks may require collateral for loans above a certain amount. Public sector banks like SBI require collateral over and above ₹7.5 lakhs, whereas HDFC Credila gives out both collareal and non collateral loans. Lenders may accept collaterals in the form of houses, flats, FDs, and other assets or properties

Factors to know before applying for an education loan for studying in the USA

Before applying for a student loan, one should always have a clear idea about the money involved and other factors like:

- Finalize the course you want to pursue and the university you want to study in

- Estimate the amount you need to finance the education

- Make a list of documents required

- Decide on a cosigner for the loan

- Make sure to apply for the loan at least three months before the visa interview date

- Some banks may offer loan approval based on your GRE or GMAT scores. High scores in these exams can increase your chances of securing a loan with better terms.

- Estimate the time of disbursement

Also Read: Why Study in USA in 2025

To ensure you’re a good investment, lenders will assess your academic potential and ability to repay your loan. Be prepared to provide the following:

Documents required for securing a student loan to study in the USA

- US University Offer Letter: Your proof of admission is essential.

- Estimated Cost of Study (I-20): Banks need to see the financial breakdown.

- Loan Application Form: The starting point of the process.

- Education Certificates/Mark Sheets: Showcase your academic achievements.

- Exam Scorecards (IELTS, TOEFL, GMAT, etc.): Prove your language and test-taking skills.

- Residential Proof (Student and Cosigner): Establishes your residency.

- Cosigner’s IT Return: Demonstrates their financial stability.

- Cosigner’s Identification and PAN Card: Verifies their identity.

- Cosigner’s Proof of Income: Ensures their ability to support the loan.

- Student’s Passport Copy: A must-have for international travel.

- Asset/Liability Details (Parents/Cosigner): Gives a complete financial picture.

- Important Note: Requirements can differ for MBA programs. Always confirm the exact list with your chosen lender.

Also Read: Study Abroad Loan Documents | Documents for Education Loan

3 things to remember when applying for US education loans

Moratorium period

The moratorium period is basically a break from having to pay back your loan. During this period the borrower does not need to make any repayment to the bank. It usually varies from bank to bank and could last until after course completion.

Loan margin

Margin money is the percentage of money the lender decides the borrower must pay from their pocket to the total loan amount. Public sector banks usually have 10-15% of margin involved which you may have to furnish from your own savings. Private banks/non-banks can cover 100% of the cost of education.

Effect of exchange rate

Always calculate the amount you will receive at the time of disbursement, as any change in the exchange rate can affect this amount.

Collateral rules for US education loans

Collateral is a valuable asset that you promise to give to the bank in case you can’t pay back your loan. Indian lenders may ask for collateral to reduce the risk of losing money.

Types of collateral accepted

Banks accept house property, commercial property, land, bonds, NSCs (national savings certificates), fixed deposits as collateral. The collateral value for a fully secured loan needs to be at least equivalent or more than the loan amount requested.

Non-collateral education loan for USA

Many banks and NBFCs offer non-collateral education loans for studying in the USA. This means you don’t need to provide any property or assets as security for the loan.

The amount offered without collateral typically ranges from ₹40 lakh to ₹60 lakh. These loans cover tuition fees, living expenses, travel costs, and other related expenses. They are a good option for students who do not have valuable assets to pledge.

Role of a cosigner in US education loan

When securing an education loan for Indian students in the USA, having a cosigner can play a crucial role. But what exactly does a cosigner do?

A cosigner is crucial in approving an education loan for Indian students in the USA.

They provide a moral obligation, making the student and their parents more committed to repaying the loan since it involves the financial reputation of someone else.

Banks may require a third-party cosigner as additional security for loans above ₹4 lakh and ₹7.5 lakh, which increases the chances of loan approval.

In terms of responsibilities, the cosigner is legally obligated to repay the loan in case of default.

A cosigner’s credit score can be affected if the loan is not repaid on time, and their financial history and stability are closely examined during the loan application process.

Indian banks and NBFCs offering loans to study in the USA

Are you aware of the leading education loan providers in India for overseas studies?

Both government and private sector banks, along with some Non-Banking Financial Companies (NBFCs), offer education loans in India.

Eligible students can apply for a study loan with the necessary documents to fund their higher education abroad.

| Bank/NBFC | Maximum Loan Amount | Interest Rate | Repayment Tenure | Collateral Security |

| HDFC Credila | No upper limit | 10.5% to 14% | Up to 12 years | Various types accepted |

| State Bank of India | Up to 1.50 crore | 10.15% to 11.75% | Up to 15 years | Required for loans above 7.5 lakhs |

| Axis Bank | Up to 1.5 crore | 16.5% to 17.5% | Up to 15 years | Required for loans above 4 lakhs |

| Punjab National Bank | Up to 1.5 Crore | 10.00%–10.75% | Up to 15 years | Required for loans above 7.5 lakhs |

| Bank of Baroda | 80 lakhs for specified institutes,60 lakhs for non-specified institutes | 10.40% -10.75% | Up to 15 years | Required for loans above 7.5 lakhs |

| Canara Bank | Upto 20 lakhs | Collateral Security 100% and above – 9.4%, Collateral Security 75% to 100% – 9.65%, Collateral Security less than 75% – 9.9% | Up to 15 years | Required for loans above 4 lakhs |

| IDBI Bank | Up to 30 lakhs | Upto 7.5 lakhs – 9%, Above 7.5 lakhs – 9.5%, 0.5% concession for female student | Up to 15 years after moratorium | Required for loans above 7.5 lakhs |

| Avanse Financial Services (NFBC) | Up to 80 lakhs | Starting from 9.5% | Up to 15 years | It may or may not require collateral |

| Incred (NFBC) | Up to 60 Lakhs | 11.85% – 13.25% | Up to 15 years | Not required for loans up to 4 lakhs |

But what if there was a platform that could simplify your search and help you find the best loan for your needs? Meet FundRight.

FundRight is the world’s first loan bidding platform designed specifically for students seeking education loans to study abroad. Here’s how FundRight can help you secure the perfect loan for your American dream:

- More Options: FundRight is a self-service portal that connects you with a wide range of lenders in India and abroad.

- Competitive Offers: Lenders bid to get your loan, ensuring you get the most favorable terms possible.

- Unbeatable Speed: You could receive loan offers in as little as two days.

- Massive Savings: FundRight empowers you to potentially save up to 23 lakhs throughout your loan.

- Expert Guidance: FundRight’s team of advisors can answer your questions and guide you through the process, ensuring you choose the most suitable loan option.

Ready to simplify your education loan search?

Head over to FundRight to get started, and find the best education loan for the USA.

Also Read: Accommodation In USA For Indian Students

FAQs for Education Loan for USA

1. What does employment verification imply in an education loan?

An employment verification generally refers to the verification done to authenticate the employment details of the loan co-signer. A co-signer of the loan is usually the student’s parent/guardian or spouse. Banks hold the responsibility of verifying the employment information provided which you will provide.

2. Do banks offer education loans without interest?

No, an interest rate will be levied by banks on education loans.

3. Does the Indian government help in waiving off your loan?

Yes, the Indian government helps waive off your loan under the Central sector subsidy scheme. Your interest amount will be paid by the government during your moratorium period. But it has one condition, that is, your family has an income of less than 4.5 lakhs per year.

4. Will I get the same amount of money on my education loan for the same level course in India and abroad?

No, usually, education loans for courses in India do not offer the same amount as for comparable-level courses abroad. Education loans offer higher amounts for courses abroad, as fees and other expenses may be higher there than for courses in India (which also depends on the educational institution).

5. What types of education loans are available for studying in the USA?

There are many types of loans available by financial institutions like SBI Education Loan, Bank of Baroda, ICICI Education Loan, Axis Education Loan, HDFC Bank’s Foreign Education, Saraswat Bank, and Avanse Education Loan.

6. What are the key features of SBI Global ED-VANTAGE – Education Loan for the USA?

With SBI Global ED-VANTAGE, you can get loans between ₹20 lakhs and ₹1.5 crore, with a repayment period of up to 15 years. It requires collateral, and repayment begins six months after the course completion.