Too many loan options, too much confusion. Choosing the best education loan in India requires understanding interest rates, how they impact your repayment plans, and what each lender’s unique advantages and limitations actually mean for your specific situation. This is not a generic list – it is a practical guide to the best education loans available in India in 2026, including the details that brochures leave out.

Students using GradRight get up to 40% better loan rates by accessing competing offers from 18+ lenders. If you are studying for a field that leads to a very high-paying job – engineering, medicine, data science, programming – you may want to opt for a shorter tenure and higher EMI. The best education loan in India is the one that best matches your career trajectory, not just the one with the lowest headline rate.

Best Education Loans in India 2026 – Quick Reference

Loan Need | Best Lender | Why |

Lowest interest rate overall | SBI (8.40%) or PNB (8.35% premium) | Public bank rates are lowest; nil processing fee at SBI |

Highest collateral-free from a bank | ICICI Bank (Rs 1 crore, premier) | Highest no-collateral limit from any Indian bank |

Best no-collateral option among private banks | IDFC First Bank (Rs 50 lakh) | Original article specific recommendation for this category |

Fastest processing | Tata Capital (72 hrs) or Auxilo (3-5 days) | NBFCs beat banks significantly on speed |

Best for working professionals abroad | BOB International EDP (Rs 80 lakh) | Specifically for employed professionals studying abroad |

No co-signer, no collateral | Prodigy Finance (USD 220K) | International lender, top global programs only |

Best for government subsidy (CSIS/PM-Vidyalaxmi) | Any public bank (SBI, Union Bank, BOI) | Subsidies only available through public banks |

Widest course coverage (NBFC) | Avanse (50+ countries, 27,000 courses) | Broader than HDFC Credila or Tata Capital |

Competitive bidding for best rate | GradRight FundRight (18+ lenders) | Lenders compete; up to 40% better rates |

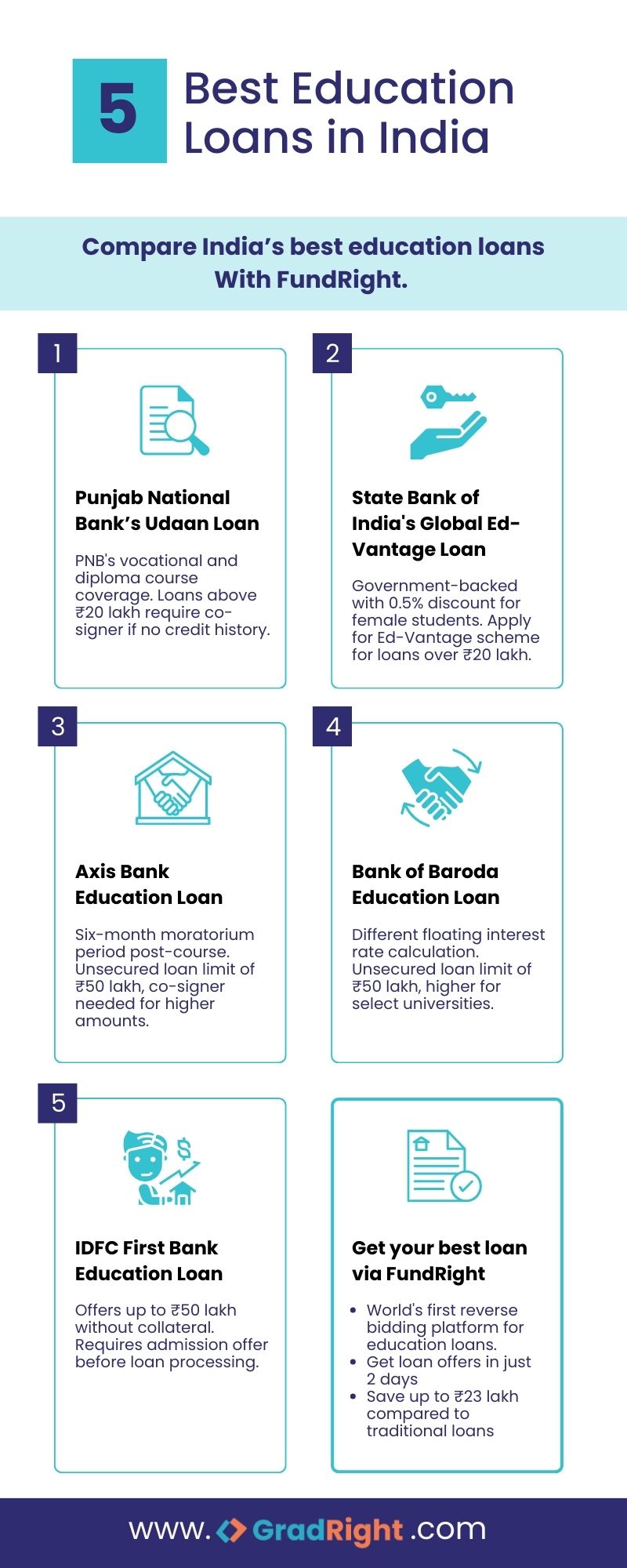

1. State Bank of India (SBI) – Best for Lowest Rate and Highest Amount

SBI is the most recognized name in education loans, and for good reason. It covers education in India and abroad at the most competitive rates among Indian banks.

Feature | SBI Global Ed-Vantage (Abroad) |

Interest rate | 8.40% – 10% p.a. (floating, RLLR-linked) |

Maximum loan | Up to Rs 1.5 crore (up to Rs 3 crore with additional collateral) |

Collateral-free limit | Rs 50 lakh for premier institutions |

Processing fee | Nil |

Girl student concession | 0.50% |

Moratorium | Course duration + 1 year (or 6 months post-job) |

Prepayment penalty | Zero |

Government subsidy eligible | Yes – CSIS, PM-Vidyalaxmi |

Service Area Approach rule | Does NOT apply to SBI (per RBI guidelines) – you can apply to any SBI branch |

2. Bank of Baroda – Best for USA and UK Abroad Studies

Bank of Baroda often crops up as an answer to ‘which bank is best for education loans?’ – particularly for study in the USA and UK. Note that Bank of Baroda uses BRLLR (Baroda Repo Linked Lending Rate) as its floating rate calculation – this is different from SBI’s approach, so compare carefully if you are evaluating both.

Feature | Baroda Scholar (Abroad) |

Interest rate (premier institutions) | ~9.5% p.a. |

Interest rate (non-premier) | ~11% p.a. |

Maximum loan | Rs 1.5 crore (premier, secured) |

Margin requirement | 10% (vs SBI 15%) – requires less personal funds |

Processing fee | 1%, max Rs 10,000 (refundable for premier institutions) |

Floating rate formula | BRLLR (Baroda Repo Linked Lending Rate) + spread – different from SBI RLLR |

GIC/Blocked Account covered | Yes – for Canada and Germany specifically |

Life insurance | Included in loan amount, deducted at first disbursement |

International EDP | Rs 80 lakh for employed professionals abroad |

3. Axis Bank – Flexible but Note the Shorter Moratorium

Axis Bank offers one of the best education loans for students in India. However, there is a critical detail that borrowers must note: the Axis Bank moratorium period is only 6 months post-course completion, NOT 1 year like most public banks. The moratorium period is the amount of time you have after graduating before you need to begin paying your EMIs.

This shorter moratorium matters in practice. Most public bank loans give you course duration + 12 months to find a job before EMI starts. Axis Bank gives you course duration + 6 months. If you are in a field where job placement takes time, this compressed window may be a genuine constraint.

Feature | Axis Bank Education Loan (Abroad) |

Interest rate | 10% – 12.5% p.a. (profile dependent) |

Maximum unsecured | Up to Rs 75 lakh |

Product categories | Prime A, B, D, and E – loan amount, rate, and flexibility vary by category |

Moratorium period | Course duration + 6 months (NOT 1 year – key difference from public banks) |

Processing time | 7-15 working days (faster than public banks) |

Government subsidy eligible | No |

4. IDFC First Bank – Best Education Loan Without Collateral Among Private Banks

IDFC First Bank has one of the best education loan interest rates in the country. However, that is not why it is on this list. IDFC First Bank offers the best education loan in India without collateral, providing up to Rs 50 lakh without any asset pledge for students at domestic Indian universities. This is useful for students who do not have assets that can cover the cost of their loan.

For STEM fields – especially in engineering, data science, and STEM – IDFC First often has better rates than the competition among private banks. Their digital platform is user-friendly and processing is relatively fast.

Feature | IDFC First Bank Education Loan |

Interest rate | From ~10.5% p.a. |

Maximum loan (abroad) | Up to Rs 1 crore (with strong profile) |

Collateral-free limit (domestic) | Up to Rs 50 lakh – best for domestic education without collateral |

STEM advantage | Better rates for engineering, data science, STEM fields vs general courses |

Processing time | Faster than public banks |

Moratorium period | Course + 12 months (standard – unlike Axis Bank) |

Also Read: Education Loan Without Collateral for Study Abroad

Top NBFCs for Education Loans in India 2026

NBFC | Starting Rate | Max Unsecured | Key Differentiator |

10.5% | Rs 1 crore+ | Oldest dedicated education lender (2006). Internationally recognized. Universities trust Credila sanction letters. | |

10.5% | Rs 75 lakh (Rs 1.2Cr strong profiles) | 50+ countries, 27,000 courses. Step-up EMI. Bridge loan (pre-admission sanction). | |

10.5% | Rs 85 lakh (USA) | 100% financing without confirmed admission. Partial moratorium EMI Rs 5,000/month for Masters. | |

11% | Rs 1.5 crore (per website) | Higher stated unsecured limit. Profile-based tiering. | |

11% | Rs 85 lakh | Platinum/Gold tier by GRE/GMAT. 72 working hours processing. STEM + Management only. | |

~12.15% APR (USD) | USD 220,000 | No collateral, no Indian co-signer. For top global programs only. |

Compare all lenders – public banks, private banks, NBFCs, and international lenders – on GradRight FundRight. 18+ competing offers, 48 hours, free. Compare Education Loans on GradRight

Best Education Loans in India 2026 – Full Comparison

Lender | Rate (Study Abroad) | Max Loan | Collateral-Free Limit | Processing Fee | Processing Time |

SBI (Global Ed-Vantage) | 8.40-10% | Rs 1.5 Cr | Rs 50L (premier) | Nil | 15-25 days |

PNB (Udaan) | 8.35-9.60% | Rs 2 Cr | Rs 7.5L standard | 1% max Rs 10K refundable | 15-25 days |

Bank of Baroda (Scholar) | 9.5-11% | Rs 1.5 Cr | Rs 40L (premier) | 1% max Rs 10K refundable | 15-20 days |

Union Bank of India | 9-10.3% | Rs 1.5 Cr | Rs 40L (premier) | Nil | 15-25 days |

ICICI Bank | 10.25-13% | Rs 3 Cr secured | Rs 1 Cr (premier) | 0.5-1% + GST | 7-15 days |

IDFC First Bank | 10.5%+ | Rs 1 Cr | Rs 50L domestic | 0.5-1% | 7-15 days |

Axis Bank | 10-12.5% | Rs 2 Cr | Rs 75L (abroad) | 0.5-1% | 7-15 days |

HDFC Credila | 10.5-13% | Rs 1 Cr+ | Rs 1 Cr+ | 0.5-1% | 5-10 days |

Avanse | 10.5-13% | Rs 1.2 Cr | Rs 75L-1.2Cr | 1-2% | 5-7 days |

Auxilo | 10.5-13% | Rs 1 Cr (USA) | Rs 85L (USA) | 1% + GST | 3-5 days |

Tata Capital | 11-13.5% | Rs 2 Cr | Rs 75-85L | 1-2% + taxes | 72 hrs processing |

Prodigy Finance | ~12.15% APR (USD) | USD 220,000 | No collateral, no co-signer | 4.2% admin | 7-14 days online |

Note: all rates are indicative and floating. They change with RBI repo rate revisions. Get personalized quotes via GradRight for your actual rate.

GradRight’s Two Calculators for Education Loan Planning

At GradRight, we offer two calculators to help you plan your education loan:

- Loan Eligibility Calculator: Enter your family income, co-applicant profile, and program details to see the maximum loan amount you are likely to qualify for across different lenders.

- EMI Calculator: Enter your loan amount, interest rate, and tenure to calculate your monthly repayment (EMI). Useful for comparing the true monthly burden of different loan offers before committing.

These calculators simplify finding the best bank for education loans and managing your finances effectively. Choosing the best bank for an education loan or the best education loan in India requires understanding interest rates and how they impact your repayment plans. Always research to ensure you select the best education loan for your specific situation – particularly if you are in a field that lands a very high-paying job (engineering, medicine, programming). In those cases, you may want to opt for a shorter tenure and higher EMI to save on total interest.

Try GradRight’s EMI calculator and compare education loan offers simultaneously. Use GradRight’s EMI Calculator

Education Loan Eligibility Criteria in India

Criterion | Requirement |

Citizenship | Indian resident (Indian citizen). Some NRI products available at select banks. |

Age | Generally 16-35 years (varies by lender; most loans require 18+) |

Academic qualification | Minimum 60% marks in qualifying examination. Admission to recognized institution required. |

Admission | Confirmed offer letter from a recognized institution in India or abroad. |

Co-applicant | Parent/guardian/spouse with stable income. Mandatory for most lenders. |

Co-applicant CIBIL | 685-700+ preferred. 750+ can reduce rate. |

Collateral | Required above Rs 7.5 lakh for public banks (standard). Optional for strong profiles at NBFCs and ICICI. |

Documents Required for the Best Education Loans in India

- Proof of admission to a college or university – offer/acceptance letter

- Identity proof: Aadhaar card, PAN card, Passport (mandatory for abroad)

- Address proof

- Academic transcripts: Class 10, 12, graduation mark sheets (all semesters)

- Entrance exam scores: GRE, GMAT, TOEFL, IELTS as applicable

- Co-applicant income proof: salary slips (3 months) + Form 16 (salaried) or ITR (self-employed)

- Bank statements: last 6 months (co-applicant)

- Collateral documents (for secured loans): property title documents, valuation certificate, FD certificates

- Fee structure and cost of attendance from the university

Advantages of Taking an Education Loan in India

Securing the best education loan in India comes with many benefits, especially for students aiming to study overseas:

Advantage | Details |

Access to premium education | Enables access to top global universities and programs that would otherwise be financially out of reach. |

Moratorium period | No EMI payments during the course + grace period. Focus on studies without financial pressure. |

Section 80E tax deduction | Full interest paid annually is deductible from taxable income (old tax regime). No upper limit. Up to 8 years. |

Credit history building | Timely repayment builds an excellent credit profile, improving home loan and car loan eligibility. |

Government subsidies | CSIS (0% moratorium interest below Rs 4.5L income) and PM-Vidyalaxmi (3% subvention below Rs 8L income) exclusively through public banks. |

Nil prepayment penalty (SBI, ICICI) | If income grows faster, pay off early without penalty – saving lakhs in interest. |

100% financing options | Select NBFCs (Auxilo, HDFC Credila) offer 100% financing without margin requirement for strong profiles. |

Competing offers via GradRight | FundRight delivers competing loan offers from 18+ lenders within two days – you get the best available rate, not just the first available rate. |

Also Read: Education Loan Tax Benefits – Section 80E Complete Guide

Too many loan options, too much confusion. Compare the best education loans in India and avoid costly mistakes on GradRight. Start on GradRight FundRight

Related Education Loan Guides

Compare Education Loan Interest Rates – All Lenders 2026

Education Loan Providers in India – Banks, NBFCs, International

Education Loan Without Collateral for Study Abroad

Education Loan EMI Calculator

GradRight vs Traditional Education Loan Process

Section 80E Education Loan Tax Benefits

Step-by-Step Education Loan Guide for Study Abroad