A smart reverse-refinance: moving from a USD loan back to an INR loan after returning home – and saving thousands on forex charges.

Case Study Overview

Not every refinance is about chasing the lowest interest rate. Sometimes, it’s about eliminating a cost that shouldn’t exist at all.

Abhijit had done everything a finance-savvy student would do. He took an education loan with repayments in USD at 7.49% – a smart choice at the time, given plans for a career abroad. But life had other plans. After completing his master’s, Abhijit returned to India and took up a full-time role earning ₹45 LPA. A strong salary – but now, every month, he was converting INR to USD just to service his loan. The forex charges weren’t catastrophic individually, but they added up over time into a silent, steady drain.

He came to GradRight not in crisis, but with a question: does it make financial sense to move to an Indian lender, even if the interest rate is slightly higher? GradRight ran the actual numbers – and the answer was clear.

Student Financial Profile

| Original Loan Currency | USD |

| Original Interest Rate | 7.49% |

| Employment Status | Full-time |

| Annual Income | ₹45 LPA |

| Location | India (returned after master’s) |

READ MORE: I Have EMI Bounces on My Indian Loan. Can I Still Refinance From the US?

Problem Statement

A USD Loan in an INR Life

Abhijit’s loan was structured for a borrower planning to earn in dollars. When life took a different direction and he returned to India, that structure became a liability. Every month, INR had to be converted to USD just to make a repayment – a process that carried forex charges, exchange rate risk, and unnecessary friction.

The Hidden Cost of Currency Mismatch

The forex charges on each monthly repayment weren’t dramatic in isolation. But compounded over a remaining loan tenure, they added up to a meaningful and entirely avoidable cost – one that had nothing to do with the loan’s interest rate.

The Right Question at the Right Time

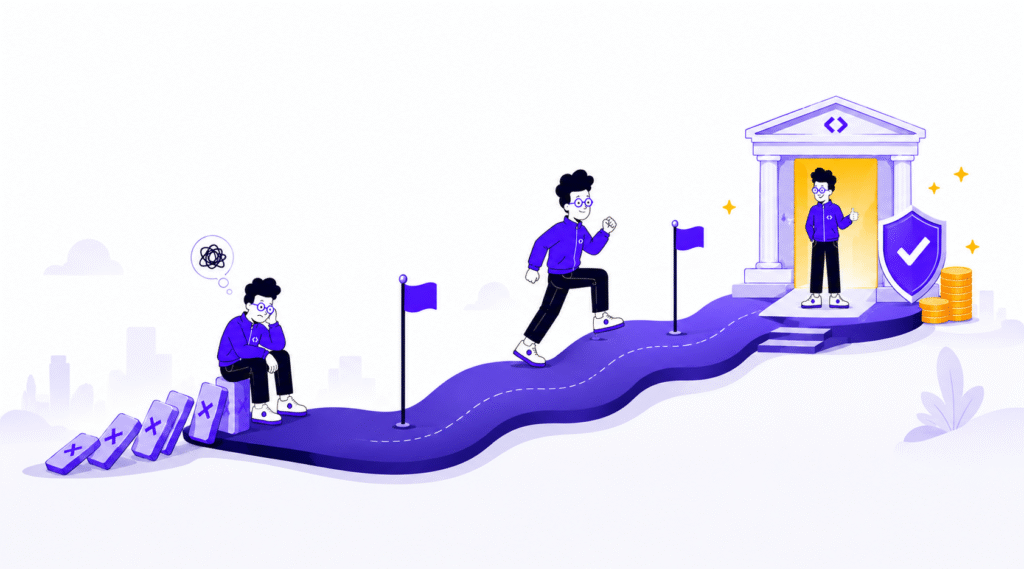

Abhijit didn’t come to GradRight in distress. He came with a sharp financial question: would moving to an INR loan – even at a higher rate – actually cost less in total? It was the right question. And it needed a proper answer backed by actual numbers, not assumptions.

Solution

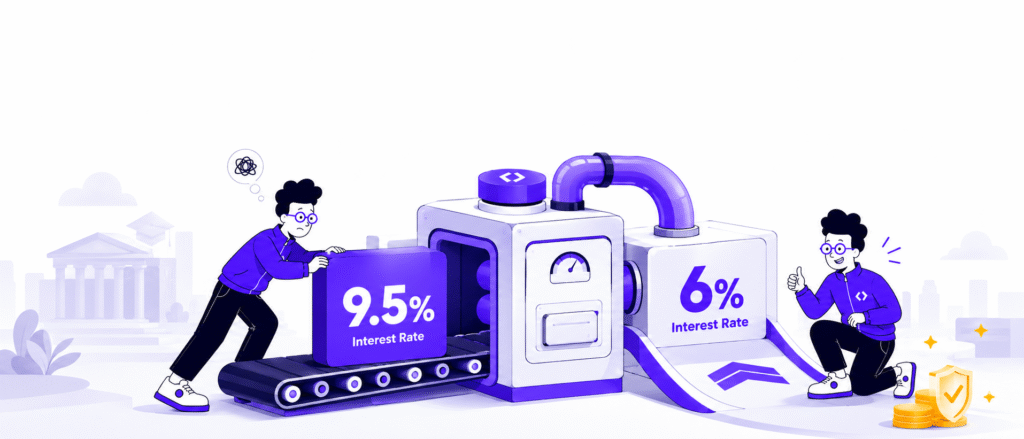

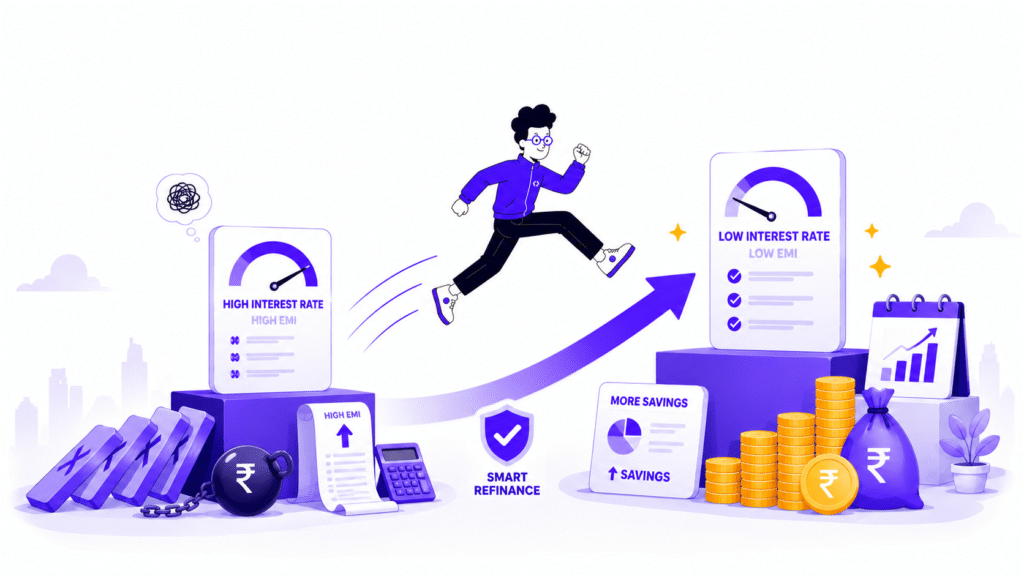

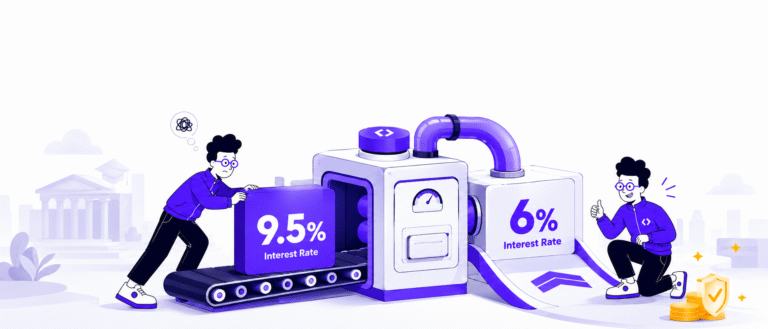

GradRight modelled the true cost of both options – factoring in not just the interest rates but the forex conversion cost and its compounding impact over the remaining tenure. The conclusion was unambiguous: an INR loan at a marginally higher rate would cost less in total because it eliminated the forex overhead entirely.

Single Move – Original Lender to Indian Lender

GradRight took Abhijit’s application to a suitable Indian lender. Sanction was completed in 3-4 days. Disbursement followed in under 15 days. New rate: 10.25% in INR – with no forex charges, no currency risk, and repayments coming directly from the same account his salary went into.

Old Loan → New Loan

Old Loan

| Interest Rate | 7.49% |

| Repayment Currency | USD |

| Hidden Cost | Monthly forex conversion charges |

New Loan

| Lender | Indian Lender |

| Interest Rate | 10.25% |

| Repayment Currency | INR |

| Sanction Timeline | 3-4 days |

| Disbursal Timeline | Under 15 days |

READ MORE: Student Loan Refinance Rates: How to Find the Lowest Deals Right Now

How Did GradRight Help?

Modelling the True Cost Rather than comparing interest rates in isolation, GradRight built a complete cost model – including forex charges and their compounding impact – to give Abhijit a clear, numbers-backed answer to his question.

Identifying the Right Lender GradRight identified the right Indian lender for Abhijit’s returning-to-India profile and managed the application from start to disbursement.

Speed of Execution Sanction in 3-4 days. Disbursement in under 15 days. A fast turnaround that reflected both the strength of the case and GradRight’s process efficiency.

Results

- Switched: USD repayment (7.49%) → INR loan (Indian Lender @ 10.25%)

- Eliminated monthly forex conversion charges entirely

- Income and loan now in the same currency – no more hedging needed

- Sanction in 3-4 days | Disbursed in under 15 days

On the surface, a move from 7.49% to 10.25% looks like a step backward. In reality, for someone earning and spending in INR, it was the most financially rational move available – and GradRight’s ability to model that clearly made all the difference.

Sometimes the best loan isn’t the one with the lowest interest rate number. It’s the one that fits your life.