How a borrower with a messy repayment history turned discipline and persistence into a successful refinance – and a second chance.

Case Study Overview

On paper, Vikram’s loan file looked like a lender’s nightmare. Seven EMI bounces on record. Rejected by two lenders – both citing repayment concerns. An outstanding loan of ₹40 lakhs at 12.9% interest. And a period of zero income right after graduation.

The context, of course, was more nuanced. The bounces happened during the gap between Vikram’s graduation and the first job – not out of negligence, but circumstance. Once full-time employment began at $50,000 per year and an H1B application was filed, every overdue amount was cleared and a clean repayment streak was maintained.

When Vikram approached GradRight, most advisors would have said wait. GradRight didn’t.

Student Financial Profile

| University | University of Houston |

| Visa Status | STEM OPT (H1B applied) |

| Job Status | Full-time |

| Annual Income | $50,000 |

| Outstanding Loan Amount | ₹40 Lakhs |

| EMI Bounces on Record | 7 |

| Prior Refinance Rejections | 2 (lenders who declined citing repayment concerns) |

Problem Statement

A Repayment History That Told an Incomplete Story Seven EMI bounces on record. Two refinance rejections. On the surface, a difficult case. But the bounces occurred during a specific and temporary window – the gap between graduation and employment – not as a pattern of financial irresponsibility. The story didn’t end with the bounces. It continued with a full clearance of overdue amounts and a consistent repayment streak once income was stable.

Twice Rejected, Still Standing Two lenders had already reviewed the file and declined, both citing repayment concerns. For most borrowers, a second rejection signals the end of the road. For Vikram, it was still the middle of the journey.

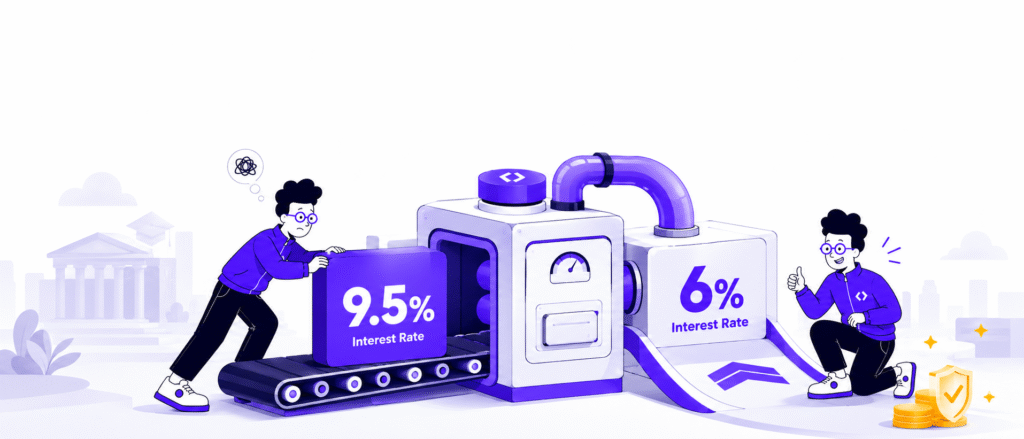

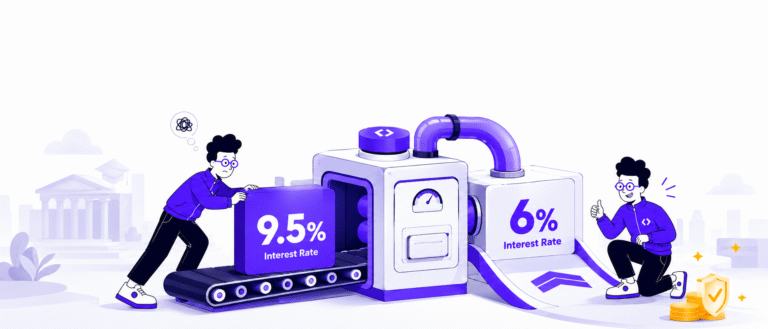

A High Rate on a Significant Balance The existing loan with the original lender carried a 12.9% interest rate on ₹40 lakhs outstanding – a rate compounding into a real and growing cost, with no refinance path yet secured.

READ MORE: I Have EMI Bounces on My Indian Loan. Can I Still Refinance From the US?

Solution

GradRight didn’t look at the bounces in isolation. The team studied the complete repayment arc – what happened before, what happened during, and critically, what happened after. The post-employment track record showed a borrower who had recognised the problem, cleared the backlog, and built a clean streak from that point forward.

The strategy wasn’t to hide the bounces. It was to present the full picture to the right lender.

Identifying the Right Lender GradRight identified a refinancing partner with the appetite to look beyond surface-level blips and assess genuine creditworthiness. Not every lender would take this case – but the right one would, with the right framing.

Making the Case GradRight presented Vikram’s complete profile to the new lender – the temporary gap period, the context behind the bounces, the full clearance of overdue amounts, and the clean repayment record since. A borrower who had struggled temporarily, rebuilt consistently, and was now a stable, employed professional on STEM OPT with an H1B application filed.

The New Lender Said Yes The loan was refinanced at 10.5% – a meaningful reduction from 12.9%, and a result that two other lenders had already declined to offer.

Old Loan → New Loan

Old Loan

| Lender | Original Lender |

| Interest Rate | 12.9% |

| Outstanding Loan Amount | ₹40 Lakhs |

New Loan

| Lender | New Lender |

| Interest Rate | 10.5% |

| Status | Approved despite 7 prior EMI bounces and 2 earlier rejections |

READ MORE: How International Students Can Refinance Their Education Loan in the U.S.

How Did GradRight Help?

Looking Beyond the Surface

Where other lenders saw a red flag, GradRight saw a fuller story. The team didn’t dismiss the bounces – they contextualised them, tracing the arc from the gap period through to the clean track record that followed.

Finding the Right Lender

GradRight identified a refinancing partner with the right appetite for this profile – one that would assess the borrower holistically rather than stopping at the bounce count.

Framing the Case Correctly

The pitch to the new lender wasn’t a cover-up. It was a complete, honest presentation of Vikram’s journey – the struggle, the recovery, and the consistency since. That framing made the difference.

Persisting Where Others Had Stopped

Two rejections had already accumulated. GradRight pursued a third attempt with a different lender and a sharper strategy – and it worked.

Results

- Rate: 12.9% (Original Lender) → 10.5% (New Lender)

- Approved despite 7 prior EMI bounces

- Successful on the third attempt – after two earlier rejections

- Outcome: Interest savings and a credit score rebuilding opportunity

Beyond the rate reduction, what was gained here was arguably more valuable: a cleaner credit slate. With a lower EMI and a fresh repayment track, the path to rebuilding a credit profile the right way was now open.

A rejection isn’t a verdict – it’s a data point. The right guidance can turn that around.