Arjun, a Data Scientist on STEM OPT who refinanced to a US bank and reclaimed thousands of dollars in savings.

Case Study Overview

Arjun had done everything right. A STEM degree from the University of North Texas, a full-time role as a Data Scientist at Infosys by December 2024, and an annual income of $80,000 – a strong start for any fresh graduate.

But one thing lingered: an education loan at 9.5% fixed, with $34,500 still outstanding. The loan was in USD, the income was in USD – the math wasn’t terrible. But 9.5% wasn’t the best rate available anymore. Not with a stable job, a credit score of 731, and a clean repayment track record.

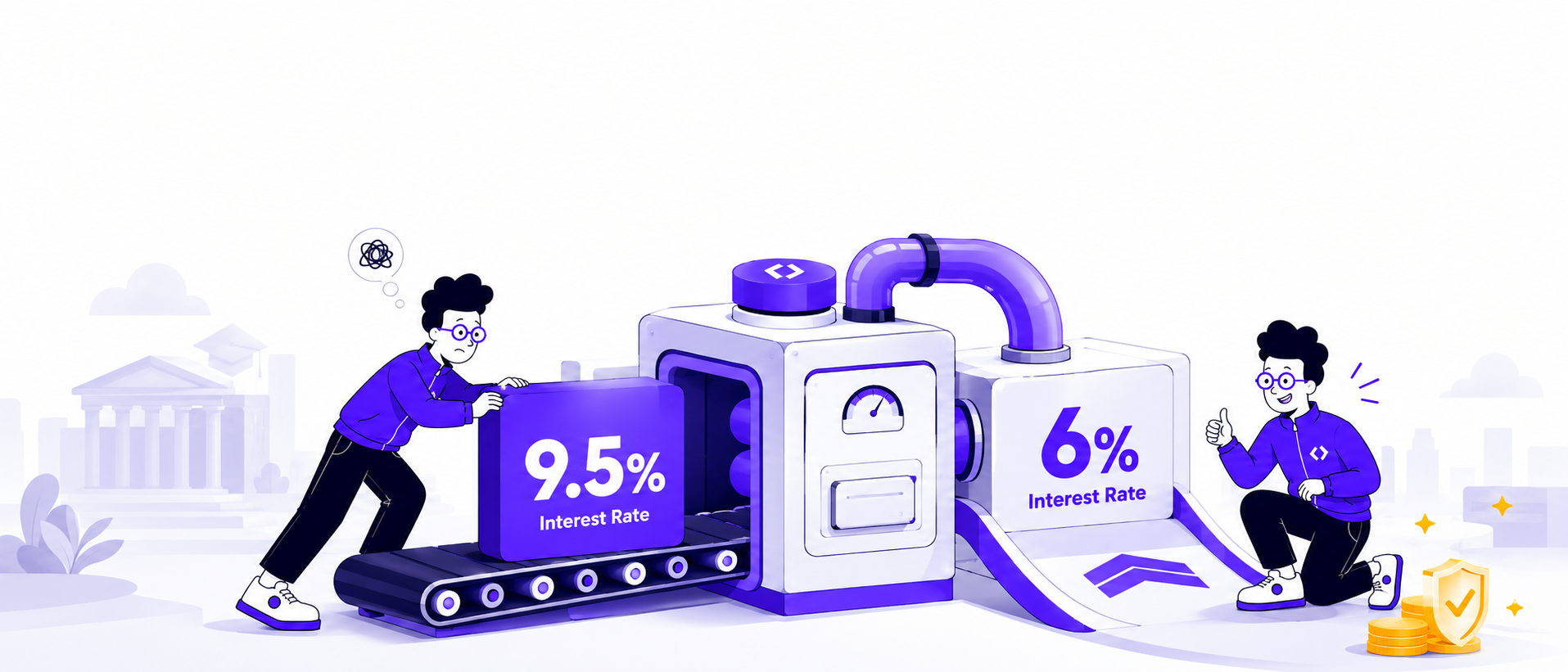

GradRight evaluated the full financial profile and the verdict was clear: a strong candidate for US bank refinancing. On 2 May 2025, the US bank disbursed $34,500 directly to the original lender, closing out the old loan completely. New rate: 6% fixed.

Student Financial Profile

| University | University of North Texas |

| Graduation | May 2024 |

| Program | STEM |

| Visa Status | STEM OPT (valid till Dec 2027) |

| Employer | Infosys |

| Role | Data Scientist |

| Employment Start | December 2024 |

| Annual Gross Salary | $80,000 |

| Monthly Net Income | ~$5,000 |

| Car Loan Outstanding | $10,000 |

| Credit Cards | 2 (Discover & Amex) – $1,100 outstanding |

| Credit Score | 731 |

Problem Statement

A Rate That No Longer Matched the Profile The education loan carried a 9.5% fixed interest rate on $34,500 outstanding. It wasn’t a crisis rate – but it was a rate assigned to a borrower who was still a student. That borrower no longer existed. A full-time job, a consistent income, and a clean credit history had built a profile that deserved better.

The Cost of Not Acting With both income and loan in USD, there was no currency risk – but staying at 9.5% when a significantly lower fixed rate was within reach was a cost in itself. Every month of inaction was money left on the table.

A Profile Ready for a US Bank A credit score of 731, STEM OPT visa validity through December 2027, stable employment at Infosys, and manageable existing liabilities – a car loan and two credit cards with a small outstanding balance. The profile wasn’t just eligible. It was strong.

READ MORE: Are You Eligible to Refinance Your Student Loans?

Solution

GradRight assessed the full financial picture and identified that Arjun didn’t need a staged approach. The profile was solid enough to go directly to a US bank and secure the most competitive rate available in a single move.

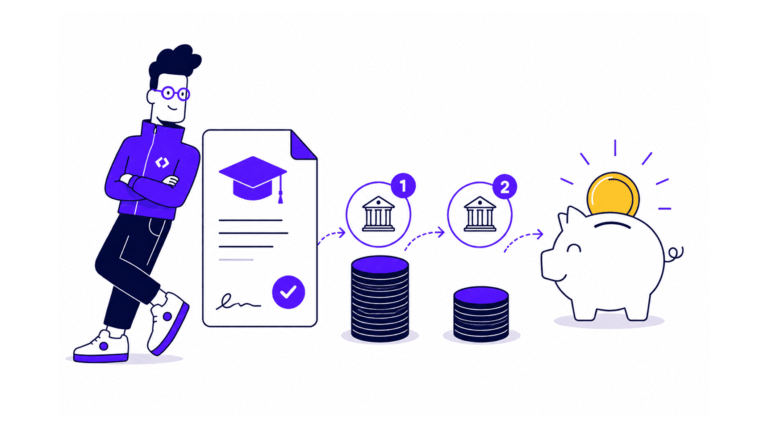

Single Phase – Original Lender to US Bank GradRight matched the borrower with a US bank whose eligibility criteria aligned closely with the profile. On 2 May 2025, the US bank disbursed $34,500 directly to the original lender – closing out the old loan in one clean transaction. The new rate: 6% fixed, with no reset risk for the entire tenure.

Old Loan → New Loan

Old Loan

| Lender | Original Lender |

| Interest Rate | 9.5% Fixed |

| Outstanding Loan Amount | $34,500 |

New Loan

| Lender | US Bank |

| Interest Rate | 6% Fixed |

| Disbursement Date | 2 May 2025 |

| Repayment | US Bank directly paid off original lender |

READ MORE: How International Students Can Refinance Their Education Loan in the U.S.

How Did GradRight Help?

Full Profile Evaluation

GradRight assessed employment status, visa validity, income, credit score, and existing liabilities – building a complete picture of eligibility before recommending a path forward.

Direct Lender Match

Based on the profile, GradRight identified the right US bank – one whose product and criteria aligned closely enough to make approval at a competitive rate a high-probability outcome.

End-to-End Execution

GradRight managed the process from application to disbursement, ensuring the US bank paid off the original lender directly – a clean, seamless transfer with no loose ends.

Results

- Rate: 9.5% (Original Lender) → 6% Fixed (US Bank)

- Loan Amount: $34,500 fully refinanced in a single move

- No Currency Mismatch: USD income, USD loan – no exchange rate risk

- Fixed Rate: No surprises for the entire tenure

A 3.5 percentage point reduction on $34,500 compounds into thousands of dollars saved over the loan tenure. More importantly, every month means a lower payment and more of the income stays where it belongs.

Refinancing here wasn’t about financial trouble. It was about recognising that the profile had evolved – and demanding a rate that matched it. Sometimes the best financial decision isn’t a dramatic rescue. It’s simply knowing when you’ve earned the right to a better deal – and acting on it.