Affordable Education Loans Up to 2 Cr. in 20 Mins*

Whether it’s a premier degree in India or a global pivot, get loan offers from 15+ lenders, starting at just 8.33%*

Transparent process. No hidden charges.

Select from our Features

- Compare Lenders

- KYC in 2 Mins

- View Bids on Your Profile

- Free Expert Assistance

Accessible, Impactful, At Scale

Trusted by 2.5 lakh Indian students

Get the Funds to Study Anywhere You Can Imagine

No borders. No bias. Just funds that follow your admit.

Choose from public banks, private banks, and NBFCs

Education Financing Made Easy

Sign Up in Minutes

Create your profile in minutes – add your loan request and academic profile, no branch visits, no piles of forms. Just you, your study plans, and our platform.

Get Offers From 15+ Lenders

15+ banks and NBFCs compete for your profile. Compare rates, EMIs, and terms side by side in one dashboard – organized, transparent, stress-free.

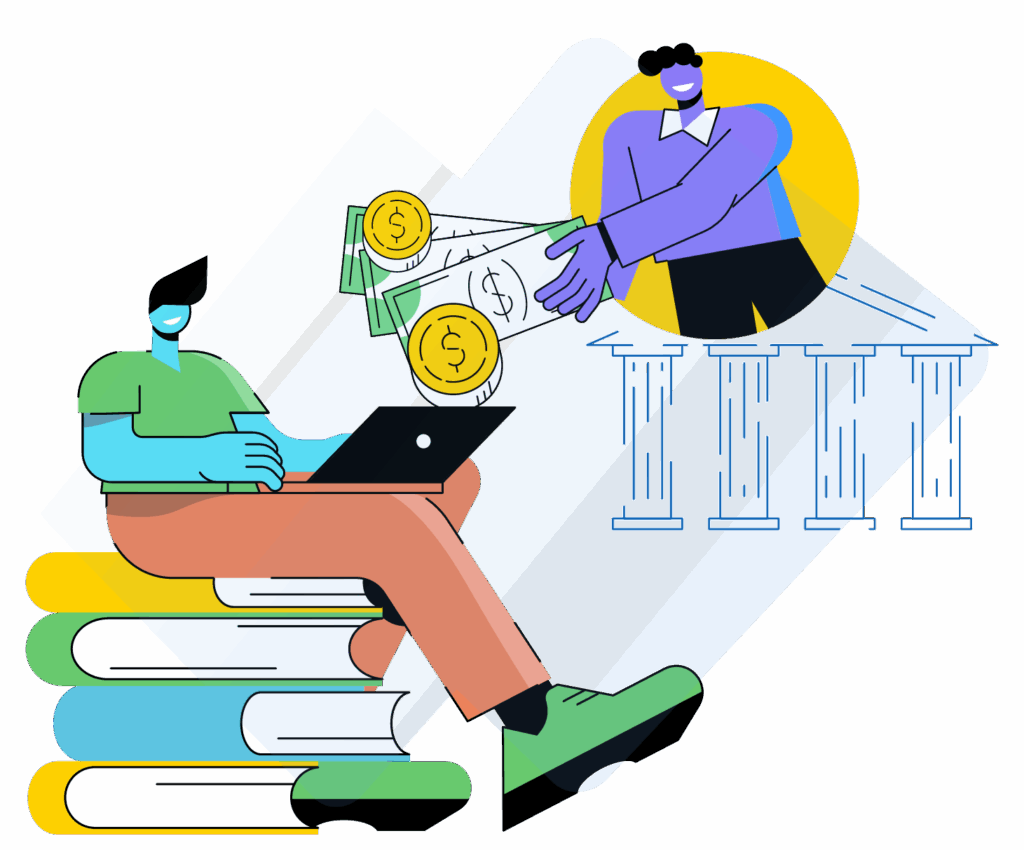

Scholarships That Cut Down Your Loan

Get auto-enrolled for a loan scholarship pool of $1M. Reduce what you borrow and repay. Less debt, more breathing room for your future.

Submit Documents Once

Upload everything securely online – admit letters, ID, financials. No chasing signatures or scanning at the last minute.

Get Approved in 20 Minutes

Pick your best offer, hit submit, and get your approval faster than the old “run to five branches” method.

Helping Students & Parents Get Access to Affordable Financing

I went to several banks before I found GradRight. They helped me get the loan that I wanted, without charging me anything.

Pratham

|

San Jose State University

MS in Software Engineering

From starting the loan process till the end, they took care of everything. I would recommend them to all my friends.

Jayashree

|

United Kingdom

Master's in Public Health

We were facing difficulty with the loan process, but GradRight was God’s gift to us – they helped us fulfil our dream of sending our two kids abroad.

Jharna Bhatt

|

United States

Parent

GradRight simplified the entire process for me. After submitting my docs, I received multiple loan offers within days. They help you see things clearly.

Kiyedh

|

Germany

Master’s in Sustainable Energy

Most banks confused me, but with GradRight everything went on very smoothly. I appreciate their transparency and communication. Thank you GradRight.

Seshendra

|

United States

Parent

What Kind of Loan Offers Are You Eligible For?

Your response was submitted

Frequently Asked Questions

Can I get an education loan for study abroad without collateral?

Yes, many banks and NBFCs provide unsecured education loans for overseas studies, especially for top universities. The approval depends on your profile, co-applicant income, and course. With GradRight, you can compare student loans for study abroad – secured and unsecured – side by side to pick the best fit.

How do I choose the best student loan for study abroad?

Choosing the right student loan for study abroad depends on loan amount, interest rate, repayment terms, and processing speed. Education loans for overseas education can differ widely across lenders. GradRight’s FundRight platform makes lenders bid for your profile, ensuring you get the lowest rate possible.

What does an education loan for abroad studies usually cover?

An education loan for abroad studies typically covers tuition fees, living expenses, exam fees, insurance, and even travel tickets. Student loans for overseas study can be customized based on your course and country. GradRight ensures you know exactly what’s covered before you commit to any lender.

Which banks provide student loans for abroad education?

Banks like HDFC, ICICI, and SBI offer education loans for overseas education alongside private lenders. Each student education loan for study abroad comes with different conditions on collateral, co-signers, and repayment. GradRight aggregates offers from 15+ lenders so you can compare all in one place.

How do interest rates work for student loans for study abroad?

Interest rates for education loans for abroad studies vary depending on the bank, co-applicant income, and loan amount. For instance, HDFC Credila or ICICI Bank may offer flexible rates for overseas education loans. GradRight helps you discover which lender gives the lowest rate for your profile.

What is the maximum amount I can get through loans for overseas study?

Most banks provide an education loan for overseas studies covering ₹20–40 lakhs without collateral, and higher amounts with collateral. Student loans for study abroad can even go up to ₹1.5 Cr for premium programs. GradRight ensures you don’t overborrow while still covering all your expenses.

Can I get a student loan for study abroad after admission?

Yes, you can apply for an education loan for overseas education both before and after securing admission. Having your admit letter improves approval chances. With GradRight, lenders compete to offer you the best education loan for abroad even post-admission.

Are student loans for students studying abroad available without a co-applicant?

Some lenders provide student loans for students studying abroad without a co-applicant, though terms may be stricter. Education loans for overseas studies with co-signers often come with lower interest rates. GradRight lets you explore both scenarios and see what’s feasible for you.

How does GradRight make getting an abroad education loan easier?

Instead of you chasing banks for an education loan for overseas studies, GradRight flips the script. Our platform invites multiple lenders to bid for your student loan for abroad. This means you choose from the best offers, saving both time and money.

Can I use a study abroad loan to cover living costs?

Yes, most study loans for abroad cover living costs like rent, food, and travel along with tuition. Education loans for overseas studies are designed to support your entire journey. GradRight helps you confirm coverage upfront, so you’re never surprised later.

Are study abroad education loans different for undergrad and master’s?

Yes, an education loan for abroad studies may have different terms for undergraduate vs. postgraduate programs. Undergraduate study loans for overseas study may require higher collateral, while master’s programs often have more flexible terms. GradRight helps you compare by degree level.

What documents are needed for student loans for overseas study?

For an education loan for overseas education, you’ll typically need admission letters, academic records, financial documents, and ID proof. Requirements may vary for each student loan for study abroad. GradRight guides you step-by-step so you don’t miss a single document.

Can I get full funding through an education loan for study abroad?

Some banks and NBFCs provide education loans for abroad studies that cover full tuition and living expenses. Student loans for students studying abroad can be topped up with scholarships for better affordability. GradRight ensures you see options that get as close as possible to 100% coverage.

What are the repayment terms for overseas education loans?

Repayment for an education loan for overseas studies usually starts after a moratorium period (course duration + 6-12 months). Student loans for study abroad can offer tenures of 10-15 years. GradRight helps you find lenders with repayment plans that match your career goals.

Is GradRight really free for students applying for an overseas education loan?

Yes. GradRight doesn’t charge students for using the platform. You can explore lenders, compare offers, and finalize your student loan for abroad without paying a single rupee. The only costs are the loan charges set by the bank you choose.

How does GradRight ensure transparency in education loan offers?

Every lender’s terms – interest rates, processing fees, repayment tenures-are shown upfront on GradRight’s platform. Whether it’s HDFC Credila, ICICI, or SBI, you see the exact student loan for overseas education details side by side. No hidden clauses, no surprises.

How does GradRight help me finance my higher education?

GradRight helps you compare loan offers from multiple lenders, understand repayment options, explore scholarships, and make informed financing decisions for your higher education journey, whether you plan to study in India or abroad.

Can I get an education loan for studying in India or abroad?

Yes. GradRight helps students explore education financing options for higher education programs across India and international destinations.

How do I choose the right education loan?

Can I compare loan offers from multiple lenders?

Yes. Instead of applying separately across banks and NBFCs, GradRight helps you compare multiple education loan offers in one place.

Which lenders can I access through GradRight?

Students can explore loan offers from public banks, private banks, NBFCs, and international lenders based on eligibility and profile fit.

Can I get an education loan without collateral?

Some lenders provide collateral-free education loans depending on your university, course, profile, and loan amount.

What expenses can an education loan cover?

Education loans may cover tuition fees, living expenses, travel costs, accommodation, study materials, insurance, and other approved educational expenses.

Can scholarships help reduce my loan amount?

Can I apply for a loan after getting admission?

Yes. Many students begin the financing process after receiving admission offers. Loan options may vary based on timelines and lender requirements.

How quickly can I receive loan offers?

Is GradRight free for students?

Yes. GradRight is free for students and helps simplify higher education planning without platform charges.

How does GradRight make financing easier?

GradRight acts as your Higher-Ed Co-pilot by helping you compare financing options, understand tradeoffs, and make informed decisions without confusion.