Dreaming of studying in Australia but are shocked by the price tag?

With undergraduate tuition fees averaging between $20,000 and $45,000 annually and living expenses estimated at $21,041 per year, the financial challenges can seem insurmountable.

But don’t lose hope—education loans can help you achieve your study abroad dreams.

In this guide, we’ll explore everything you need to know about Education loan for Australia. Down Under, from interest rates to eligible courses and application requirements.

Let’s make your dream of an Australian education a reality without breaking the bank.

Also Read: Education loan for Study Abroad Guide for Students

Introduction to studying in Australia

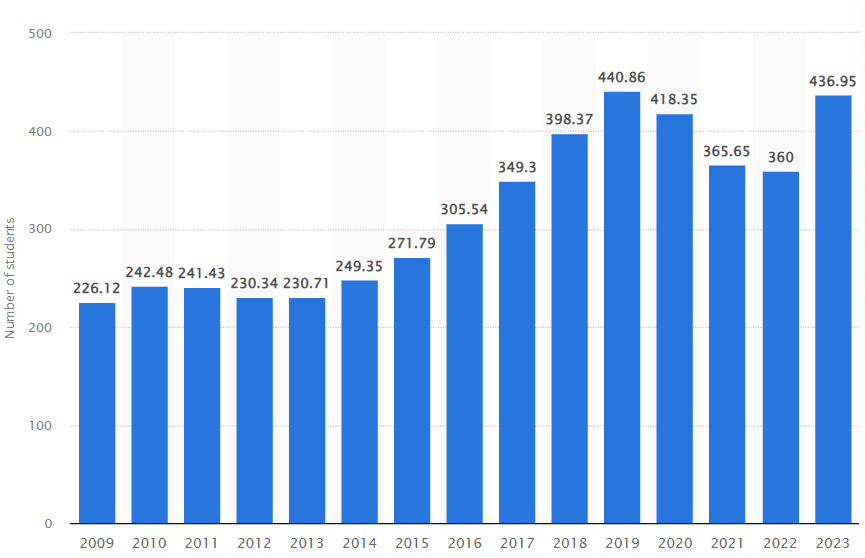

Australia has become a popular destination for international students, with the number of students enrolled in Australian universities rising from 226,000 in 2009 to 436,950 in 2023.

This surge is proof of Australia’s rising reputation as a coveted destination for higher education. Here are the reasons behind these growing numbers.

Diverse study options

Australia offers a wide range of options for international students. With more than 1,100 institutions and 22,000 courses available, students have ample opportunities to explore and specialize in their chosen fields.

The Australian Qualifications Framework (AQF) facilitates smooth transitions between different qualification levels, making the education pathway both structured and adaptable to your aspirations.

Regulatory bodies

The education system in Australia is backed by some of the most robust regulatory bodies.

The Australian Skills Quality Authority (ASQA) oversees vocational education and training programs, while the Tertiary Education Quality and Standards Agency (TEQSA) oversees universities and higher education providers.

These bodies ensure that the programs meet industry needs and prepare you for the workforce.

Multiple visa options

When it comes to visas, you can opt for multiple options depending on your career interests. For example, the 402 Training and Research Visa and the Training Visa subclass 407 offer two-year work opportunities for students with employer sponsorship.

Financial support through loans

Australia is known for its quality education and the support it offers international students. Many universities provide study loans to cover tuition fees and living expenses, making your higher education journey smoother and more affordable.

For Indian students, education loans from Indian Banks and NBFCs are also available, often with competitive interest rates and flexible repayment terms.

Also Read: Study in Australia 2025: Process, Eligibility, Documents, Visa & More

Application process for education loan to study in Australia for Indian students

While the application process is time consuming, with several steps, you can navigate it with confidence when you have all the right information. So, if you’re looking to study abroad, the guidelines below can help you get started with your application.

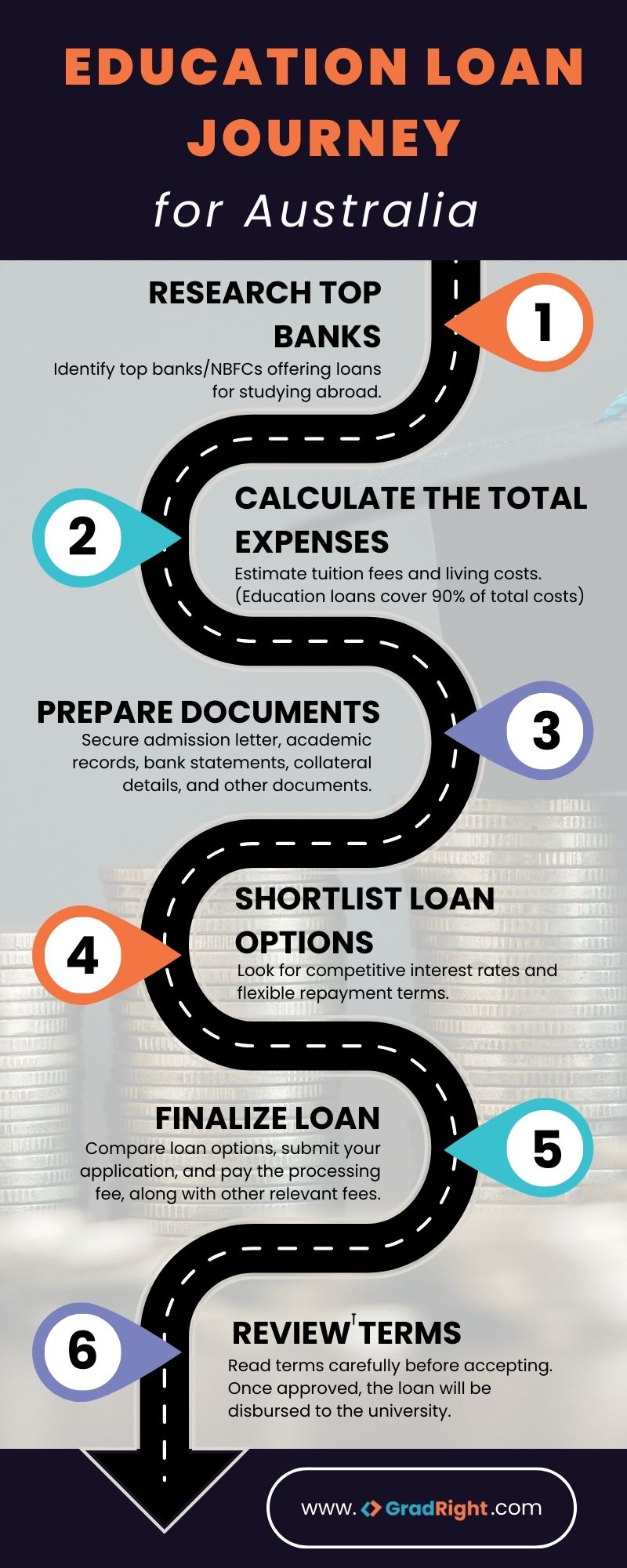

Step 1: Research and list banks

Start by identifying banks and Non-Banking Financial Companies (NBFCs) that provide education loans for Australia, in India. Some of the popular options include HDFC Credila and Union Bank of India education loans.

The bank or NBFC you choose should recognize your university and course so that you can secure a loan from them.

Step 2: Calculate expenses

Ensure that you understand all the costs of studying in Australia–such as tuition fees and living costs, to arrive at the loan amount you need to apply for.

Step 3: Obtain all the required documents

Secure an acceptance letter from your Australian university of choice as proof of admission. You’ll also need academic records, bank statements, details of a cosigner (if required), and the documents of your collateral.

Note: If you haven’t secured an admit letter from the university you’ve applied to, you can still apply for the loan by submitting your GRE/GMAT/Any other relevant exam’s scores.

Also, education loans are available without the need to pledge any collateral. In such cases, you’ll need a co-applicant to apply alongside you.

Step 4: Shortlist loan options

Make a checklist of banks that provide education loans, including competitive interest rates, flexible repayment terms, a bank offering 100% financing, and quick payout options.

You can do this with ease on FundRight, a loan-search platform that can help you compare loan offers from the top 15 lenders (including the best Indian government and private banks, NBFCs, and international lenders). Simply register, complete your profile, and get loan offers from top banks within 30 minutes. We will explain this in more detail later in this guide.

Step 5: Finalize the loan amount and apply

Compare your overall spending with the loan options, submit your application, and wait for the final decision.

Step 6: Review terms and disbursement

Once approved, the lender will provide a loan offer or sanction letter. Carefully read the terms and conditions before signing the loan disbursement agreement.

The processing fee, paid after your loan is sanctioned, is used to get your official sanction letter from the bank. This sanction letter can be used for your visa application.

The loan amount will be credited to your account once you have accepted every clause.

When you apply for an education loan to study in Australia, you need time for planning and preparation. That’s why we recommend that students start this process at least six months before the program begins.

Eligibility criteria for an education loan to study in Australia

To be eligible for an education loan to study in Australia, students have to meet the following criteria:

- You should be an Indian citizen

- You should have secured admission to a recognized university in Australia

- The course you enroll into must be recognized by the lending institution and should be job-oriented, professional, technical, or a diploma course

- You should have a good academic record

- Some banks may also require a co-applicant, such as a parent or guardian, to grant the loan

- As per the bank’s policy, collateral may be needed for loans exceeding a certain amount

- If you’re a minor, your guardian will be required to take a loan on your behalf

Check with specific banks or financial institutions for their detailed eligibility requirements for the education loan to study in Australia.

How to choose a bank for a study loan to study in Australia?

When you choose a bank for an education loan to study in Australia, consider these factors:

Interest Rates

Compare the interest rates offered by different banks. Nationalized banks generally offer lower rates than private banks and NBFCs.

For example, Union Bank of India, Bank of Baroda, and State Bank of India offer rates between 9.25% and 11.5%. The actual interest you will be offered depends on the loan amount and other factors.

Loan Amount

Check the maximum loan amount offered by the bank. It should cover your tuition fees and other expenses.

Repayment Terms

Look for banks that offer flexible repayment options and a longer moratorium period. This will give you more time to repay the loan and reduce financial stress.

Processing Time

Choose banks that process loan applications quicker to ensure you receive the funds on time. Nationalized banks are known to take longer to process loans compared to private banks and NBFCs.

Collateral Requirements

Some banks provide unsecured loans without requiring any collateral. This is helpful for students who don’t have assets to use as security. However, unsecured loans might mean you have to pay a higher rate of interest.

Loan Coverage

Ensure that the loan covers tuition fees and other expenses such as accommodation charges, travel expenses, and study materials. Some banks also cover medical insurance (OSHC Australia) expenses.

Subsidy Schemes

Check if you are eligible for government subsidy schemes on education loans, such as the Dr. Ambedkar Central Scheme of Interest Subsidy or the Padho Pradesh Central Scheme of Interest Subsidy.

Before you decide, we recommend you get in touch with an advisor from GradRight. We are not affiliated with any bank/NBFC and offer free-of-cost, unbiased, and accurate guidance to students who wish to study abroad. Expect to get the most up-to-date information on your chosen bank’s education loan offerings for Australia, along with any other info you might need.

Also Read: All You Need To Know About Student Loans for Australia

Before you apply for an education loan to study in Australia, consider this

Here are some key factors to keep in mind:

- Make sure that you meet all the requirements set by the bank or NBFC

- Decide between a secured or an unsecured loan

- Choose a lender that offers a quick approval process

- Understand the terms of loan repayment (the tenure, EMIs, repayment schedule, and moratorium period) before you commit to the loan

- Ask about any extra fees like processing fees, early payment charges, or fees for late payments

Documents required for securing a student loan to study in Australia

Here’s a list of documents that you must submit with your application for an education loan to study in Australia.

- CRE/GMAT or IELTS test scores

- Acceptance letter from an Australian university

- Fully completed application form for the loan

- Documents outlining the expenses related to the studies

- Proof of identity

- Proof of address

- Permanent Account Number (PAN) details

- Financial statements from the guarantor, co-borrower, or student

- Asset declaration from the guarantor, co-borrower, or student

- Income documents of the guarantor, co-borrower, or student

- Student’s academic documents (10th, 12th, bachelor’s)

Things to remember when applying for education loans to study in Australia

Here are some key considerations:

- Many institutions that provide education loans for studying in Australia also help Indian students with living expenses. This is crucial because it impacts your financial situation and your Australian student visa application.

- To study in Australia, secure an adjustable student loan with any scholarships you may receive. This can help you manage your finances more effectively.

- Verify if the student loan covers the cost of OSHC Australia, which is mandatory for international students. This ensures you have the necessary health insurance during your stay.

- If you plan to apply for an Australian Permanent Residency (PR) visa, confirm whether your loan will remain valid.

- Understand the interest rates and process for applying for Indian government education loan subsidies for foreign study. This can help you plan your finances more effectively and choose the right loan option.

Rules related to collateral for education loans for studying in Australia

Collateral refers to a property or an asset that is movable or immovable, which can be offered to a bank as security to get a particular loan amount. In Australia, where collateral guarantees loan repayment, it also helps mitigate the lender’s risk.

There are many things that can be considered as collateral. These could be liquid assets like savings account balance, public provident fund, and fixed deposits (FDs), or other immovable properties such as houses, commercial properties, or land.

However, agricultural land is generally not accepted as collateral in this case.

Role of a guarantor in an education loan for studying in Australia

A guarantor is crucial in getting education loans to study in Australia, but why? It’s because they act as a backup, providing financial security to the lender on behalf of the borrower. They’ll be responsible for repaying the loan if the borrower cannot do so.

Guarantors can be your parents or blood relatives with a good credit history. This can increase your chances of loan approval, especially for students with limited credit history or income.

Indian banks and NBFCs offering loans for studying in Australia

When planning to take education loans to study in Australia, there are certain banks or NFBCs you must consider for the best interest rates and flexible repayment offers. Here’s a list of such Indian banks and Non-Banking Financial Companies (NBFCs), along with their minimum rate of interests and maximum loan amounts (for collateral based loans).

State Bank of India (SBI)

SBI offers a starting interest rate of 10.15% on education loans up to ₹1.5 crore, with a processing fee of ₹10,000. The typical processing time for getting a loan from this bank is about 14 days.

Union Bank of India

This bank provides loans with a starting interest rate of 9.25% and a maximum amount of ₹1.5 crore. However, the best thing about this bank is its refundable processing fee, which is ₹5,000. Loans are usually processed within 10 days.

IDFC Bank

IDFC bank’s starting interest rate is 9.75% for loans up to ₹1.5 crore. The processing fee ranges between 0.5% and 1%, and the processing time is up to 10 days.

ICICI Bank

ICICI bank offers loans at a starting interest rate of 10.25%, with a maximum loan amount of ₹2 crores. Processing fees vary between 0.5% and 1%, and the processing time is the quickest at 7 days.

HDFC Credila

This education loan is available at an interest rate of 10.25% for a maximum amount of ₹1.5 crore. The processing fees range from 0.5% to 1%, and loans are processed within 7 days.

Avanse

This bank offers loans at a starting interest rate of 10.5% and a maximum loan amount of up to ₹80 lakhs. The best part is that its processing fees are between 0.5% and 1%, and the processing time is one of the best, at 5 days.

Auxilo

Auxilo is generally known to offer loans at an interest rate that starts from 11.25%. Its loan amount can pan up to ₹1 crore maximum. The processing fees range between 0.5% and 1%, and the processing time is surprisingly the fastest at around 2-3 days.

InCred

InCred provides loans with a starting interest rate of 11.50% and a maximum amount of ₹80 lakhs. Processing fees are slightly higher, ranging from 0.5% to 1.5%, with a processing time of 7 days. With so many banks and NBFCs to choose from, you can easily be overwhelmed in your search for the best education loan.

Sorting out banks based on details like interest rates, repayment grace periods, late fees, and collateral requirements requires extensive research and can be exhausting.

That’s where FundRight comes in. FundRight transforms the entire loan process to make your higher education journey seamless and hassle-free.

Let us see how:

- When you create your profile on FundRight, you get competitive loan offers from 15+ top lenders.

- FundRight helps you get the lowest interest rates in the market, which could lead to savings of up to 23 lakhs throughout the loan period (depending on your loan terms).

- With FundRight, you have access to experts who will help you negotiate even better terms with lenders.

How FundRight works

- Sign up and provide the necessary details.

- Gain access to offers from India’s top 15 banks and NBFCs.

- Benefit from the guidance of an expert financial advisor from FundRight to negotiate even better loan terms.

- Safely upload your documents through the platform.

- Get your loan sanctioned in 4 or more working days.

FAQs

1. What is the typical interest rate for education loans to study in Australia?

The typical interest rate for education loans to study in Australia ranges between 9.25% and 11.35% for traditional banks. For NBFCs, the interest rates range from 10.25% to 13%.

2. How much of a loan can I get to study in Australia?

You can get education loans up to 75 lakhs to 1.5 crore from Indian banks like SBI and Union Bank. Meanwhile, private banks like ICICI, IDFC First, and Axis Bank may offer up to 75 lakhs to study in Australia.

3. What are the processing fees for education loans?

The Processing fees for education loans vary between banks. For example, SBI charges ₹10,000, Union Bank of India charges ₹5,000. NBFCs typically charge between 0.5% to 1.5% of the loan amount.

4. How long does it take to process an education loan for studying in Australia?

The processing time for an education loan can range from 5 to 14 days, depending on whether it’s a secured or unsecured loan. Some private banks and international lenders may take less time than public banks.

5. How can FundRight help me with my education loan to study in Australia?

FundRight helps you find the best education loan for Australia by letting you compare loan offers from 15+ top Indian and international lenders. As the world’s first loan-bidding platform, FundRight Because lenders can see their competitors’ offers, they’re motivated to offer you the best possible interest-rates and repayment terms. This competitiveness benefits you–the student. Plus, you get access to impartial expert financial advice from an expert, at every stage of your study-abroad journey, with FundRight.