India sends the most students to Canada, yet most families don’t know what it actually costs.

Here’s a number that should stop you in your tracks.

According to the August 2025 data by the Canadian immigration department:

“About 74% of Indian applications for permits to study at Canadian post-secondary institutions in August were rejected…compared to about 32% in August 2023.”

Thomson Reuters, November 7, 2025

And one of the biggest reasons for this rejection? Weak or incomplete financial proof.

That is why understanding a study loan for Canada matters so much now.

In early 2025, Canada said it planned to issue 437,000 study permits for 2025, which was lower than the previous year.

That tells you something important.

Canada is still open, but students now need to be more prepared, more realistic, and far more careful about money than before.

This guide is here to make that simpler.

I’ll walk you through how a study loan for Canada works, what Indian students should look for in 2026, how to compare options, and how to avoid common mistakes.

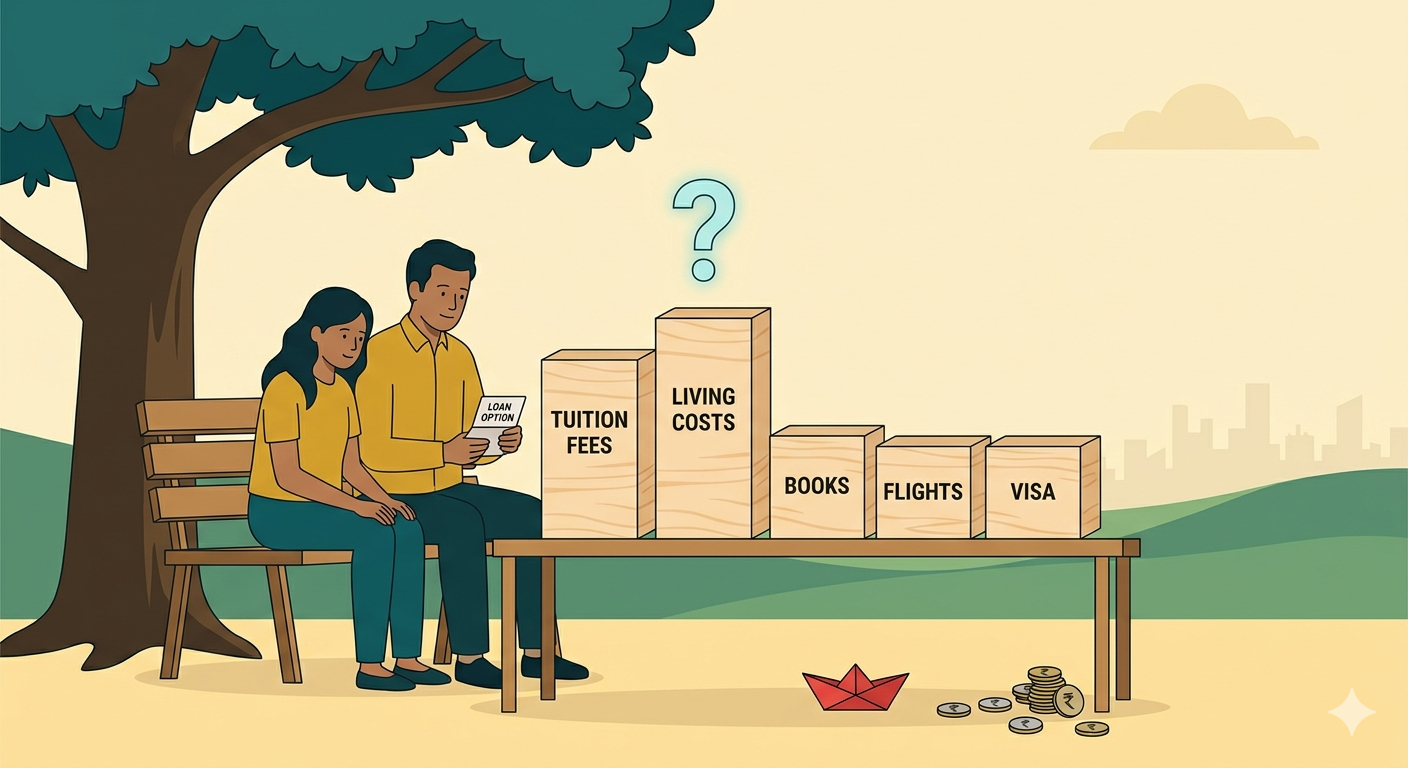

How much money do you really need for Canada in 2026?

Most students underestimate this part.

They think only about tuition. But for Canada, your funding plan has to cover much more than that.

A study loan for Canada is used to fill that full gap, not just the college fee.

Tuition Fee

For 2025–26, Statistics Canada said average international tuition was about C$41,746 for undergraduate students and about C$24,028 for graduate students. Your actual number may be lower or higher depending on the course and university. But this gives you a realistic benchmark.

Living Costs

For study permit applications made on or after September 1, 2025, Canada requires proof of C$22,895 for living expenses for one student outside Quebec. This is separate from tuition. It is not optional.

Essential Purchases

Then add the other costs students forget:

- airfare

- visa and permit-related expenses

- GIC or other required fund arrangements, where relevant

- health insurance

- books, laptop, deposits, and first-month housing setup

This is why many families feel shocked halfway through planning.

A study loan for Canada from India should be planned against the full first-year cost, not just the admission letter amount. If your tuition is C$25,000 to C$35,000 and living costs alone need nearly C$23,000, your funding requirement can quickly cross C$50,000 before you even add flights and setup costs.

That is the number you should plan around.

What does a study loan for Canada cover?

A study loan usually covers more than just tuition.

Most lenders include the core costs directly linked to studying abroad.

But the exact list depends on the bank or NBFC, so students should always check the sanction terms before assuming everything is included. Public-sector lender policies such as SBI’s overseas education loan scheme show the usual pattern.

Here’s a table for a simple overview:

| Cost item | Covered? |

| Tuition fees | Yes |

| Hostel or accommodation | Usually |

| Books and study material | Yes |

| Travel expenses | Usually |

| Laptop or equipment | Sometimes |

| Insurance | Sometimes |

| Visa-related costs | Sometimes |

| Living expenses | Often partly covered |

The key point is simple.

Do not assume that your study loan for Canada from India will cover every expense automatically.

Check what is approved, what is capped, and what you must still arrange separately.

Approval factors for study loan for Canada

Approval for a study loan for Canada depends on a few linked factors.

Lenders are trying to judge both your academic plan and your ability to repay later.

That is why approval is never based on admission alone.

The main deciding factors are:

- University and course: Better-known institutions and career-linked programs usually inspire more confidence.

- Academic record: Consistent marks can strengthen your profile.

- Loan amount needed: The amount should look reasonable for the course and total cost.

- Co-applicant profile: Income, repayment history, and financial stability matter a lot.

- Type of loan: A secured loan depends more on collateral. An unsecured loan depends more on profile strength.

- Collateral, where applicable: Property or eligible assets can support higher loan amounts.

- Overall repayment potential: Lenders want to see that the plan makes financial sense.

When you apply for a loan, approval depends on how well all these pieces fit together.

If getting a loan approval is a worry for you, you will get your mind’s peace at GradRight. Just within 4 years of launch since 2019, the platform had already processed loan requests of more than $1.75 Billion (INR 14,300 Crore) and assisted more than 55,000 students via its platform.

You can get expert advice for financing your study abroad plans. Simply write to us at GradRight.

How to get a study loan for Canada from India?

The process is usually simpler when you do it in the right order:

- Estimate your total cost: Include tuition, living expenses, travel, insurance, and setup costs.

- Check how much you can arrange yourself: This helps you know the real loan gap.

- Choose the right lender type: Bank or NBFC, secured or unsecured, based on your profile.

- Keep your documents ready: Admission letter, KYC, academic records, income proof, and collateral papers if needed.

- Apply and compare offers: Do not look only at the interest rate. Check moratorium, processing time, and repayment terms too.

- Get the sanction letter: This becomes important for your funding plan and visa process.

- Track disbursement rules: Some amounts go directly to the university, while others may be released in stages.

Next, let’s look at how to pick the right lender for yourself.

Also Read: A guide to IELTS score for Canada

How to compare lenders without getting distracted by headline interest rates?

The lowest rate is not always the best deal.

When comparing a study loan for Canada, look at the full borrowing experience, not just the number in the ad.

Focus on these points:

- Rate type: Many lenders use floating rates, so your EMI can rise later if the benchmark rate changes.

- Secured vs. unsecured pricing: Unsecured loans usually cost more because the lender is taking more risk.

- Moratorium treatment: In many cases, interest keeps building during the course and moratorium period. That changes the final repayment burden.

- Processing and other charges: Processing fees, legal charges, valuation charges, and insurance can materially increase total cost.

- University-based terms: Some lenders give better limits or easier approval only for selected universities and programs.

- Sanction speed: Important if your deadline is close.

- Disbursement rules: Funds are often released semester-wise, not as one lump sum.

- Prepayment flexibility: Important if you want to repay faster after getting a job.

When comparing, ask one simple question:

Which lender gives me the most workable loan, not just the most attractive-looking rate?

You can also look up GradRight’s lending platform for comparing loans by different lenders. More than 80% of the students we cater to come from Tier 2, 3, and 4 cities of India with average family incomes not more than 6 lakhs a year. People who couldn’t dream of going abroad have their dreams getting fulfilled through scholarships and modest loan rates.

Here are the words of one of our students who had given up on her dreams of studying in the US:

“My father doesn’t have a monthly income. He’s a daily wage laborer. I struggled to get a loan from Indian banks because they kept asking me for documents (to prove his income). I found GradRight and my financial adviser told me about lenders like Prodigy. I am so happy to have GradRight, I am finally in the US.”

Sasipriya Kota, Master’s in Computer Science, Wright State University

Let’s look at some more important things you need to keep in mind in the following section.

Repayment, tax benefit, and what not to assume

This part matters more than most students think.

A study loan for Canada may feel manageable at the sanction stage. The real test starts later, when repayment begins and the total cost becomes real.

Keep these facts in mind:

- Moratorium does not mean zero cost: Repayment usually starts after the moratorium, not immediately, but interest may keep building during this period. So your loan may cost more than the original sanctioned amount.

- Tax benefit applies only to interest: Under Section 80E of the Income Tax Act, Indian borrowers can claim a tax deduction on the interest paid on an education loan. The benefit is available for up to 8 years from the start of repayment. It does not apply to principal repayment.

- Part-time work is support, not a repayment plan: In Canada, eligible international students can currently work up to 24 hours a week off campus during regular academic sessions. That helps with some living costs, but it is not enough to treat part-time work as your full repayment strategy.

Final thoughts

A study loan for Canada can open the door. But it can also create pressure if you borrow without a full plan.

That is the real takeaway here.

For Indian students, the smartest approach is not to chase the biggest sanction or the lowest-looking rate.

It is to understand your real cost, compare lenders properly, and choose a loan that still feels manageable after graduation.

Canada is still possible. But the financial side now needs much more care than before.

If you get this part right, the loan stops being just a source of money.

It becomes part of a stronger study-abroad plan.

That is also where a platform like GradRight can help by making it easier to compare options and think beyond just the first loan offer.