The US is still one of the most popular study-abroad destinations for Indian students. In 2024-25, the Indian student population in the US stood at 363,019.

Despite its popularity, the US continues to be one of the more expensive study destinations. The total cost of attendance can stretch your finances fast.

You can expect to pay up to $55,000 a year in tuition fees. Furthermore, expect to pay up to Then, there’s the additional cost of around $40,000 a year in food, accommodation, and living expenses as well.

Education loans can help cover the majority of the cost.

So, what if you don’t have a cosigner? Won’t you be able to get an education loan without a co-applicant?

However, what if you don’t have a cosigner? Won’t you be able to get an education loan without a co-applicant?

That’s exactly what we’ll discuss here. This guide explains whether it’s possible to get a student loan for international students in the USA without a cosigner.

By the time you finish reading this article, you’ll have a clear idea of what you can or can’t get.

This guide will discuss:

- Is it possible to get an education loan without a co-applicant?

- The difference between a financial co-applicant and a primary co-applicant

- Ways to get an education loan without a co-applicant

“Only a tenth are being funded by these NBFCs… a large portion of overseas education is being funded through alternative means.” — Ajit Velonie, Senior Director, CRISIL Ratings

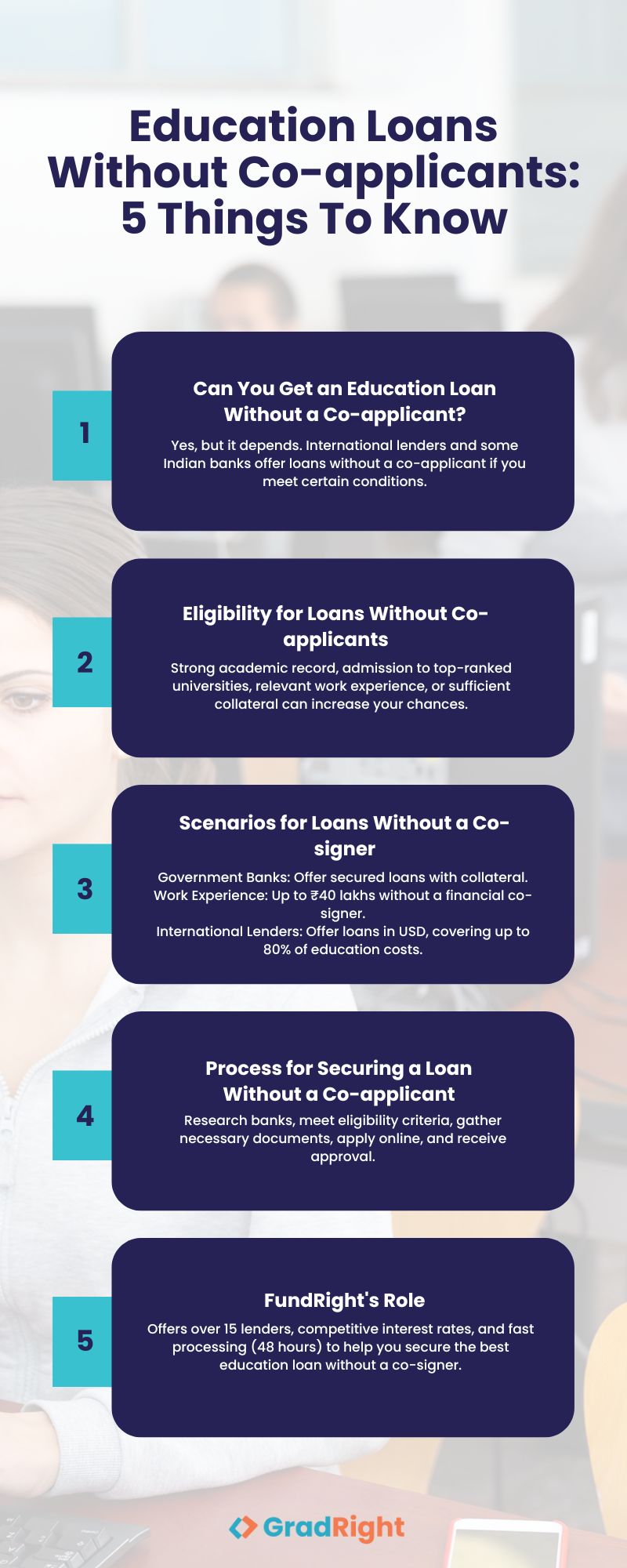

Can you get an education loan without a co-applicant?

The right answer, it depends. International lenders offer education loans without a co-applicant. However, these lenders keep a list of selected universities for which they give out the loans. Thus, if you’re not going to study at these universities, you won’t be eligible for a student loan without a co-signer.

With Indian banks, the scenario is different. While banks like SBI and Bank of Baroda may offer education loans without a financial co-applicant if you provide sufficient collateral, a primary co-applicant is usually still required. We’ll explain the difference between the two in the next section. For now, note that many public banks now have updated policies in 2024, when it comes to educational lending. These new policies allow loans without co-applicants for students with strong academic backgrounds or significant work experience.

Additionally, several universities, such as Harvard, NYU, ESSEC, and LSE, have partnerships with lenders. These lenders offer favorable terms to students without needing a co-signer, though they come with their own set of considerations. Therefore, understanding these options can help you plan your education financing even if you don’t have any co-applicant(s).

With Indian banks, the scenario is different. Here you can get an education loan without a financial co-applicant. However, you can’t get an education loan without a primary co-applicant.

Therefore, when you hear the phrase ‘education loan without a co-applicant,’ know that here the co-applicant means a financial co-applicant, not a primary co-applicant.

However, there are specific scenarios when this rule doesn’t apply, and you can get an education loan without a co-applicant. We’ll discuss those scenarios later in this article.

What’s the difference between a financial co-applicant and a primary co-applicant? That’s what we’re going to discuss next.

What’s the difference between a financial co-applicant and a primary co-applicant?

The table below explains the basic differences between a financial co-applicant and a primary co-applicant.

Aspect | Financial Co-applicant | Primary Co-applicant |

Role | Supports the financial eligibility of the loan application | Primarily serves as a contact and guarantor, with limited impact on financial eligibility |

Who Can Be Assigned | Siblings, uncles, aunts, cousins | Parents, spouse, or immediate family members |

Income Requirement | Must have a stable income | No income requirement; can be a retired person |

Impact on Loan Approval | Significant impact if the primary applicant has weak financials | Limited impact; serves more of a procedural role |

Example | A sibling with a steady job acting as a financial co-applicant | A retired parent acting as a primary co-applicant |

If you’ve understood this, then skip to the next section. There, we detail three situations where you can get an educational loan without a co-applicant.

Below, we explain in more detail the differences between a primary and a financial co-applicant:

Financial co-applicant

A financial co-applicant is a person who is related by blood to the loan applicant. The loan applicant needs to have a financial co-applicant when they don’t have a primary co-applicant with a permanent income.

Loan applicants can put their siblings, first cousins, maternal uncle or aunt, and paternal uncle or aunt as financial co-applicants.

Primary co-applicant

A primary co-applicant is a person who co-signs the education loan agreement with the loan applicant.

The co-applicant’s financial profile doesn’t affect their eligibility.

Applicants can name their parents or any immediate family member – even when they don’t have a stable income or when they are retired pensioners – as primary co-applicants.

In summary, a financial co-applicant is someone with a strong financial profile who backs your loan application. A primary co-applicant’s role is more administrative, ensuring that there is a responsible contact person for the loan.

Also Read: Non-collateral loans for Master’s Abroad

One important note before we move on. Different banks use different terms. Some will call this “co-applicant.” Others will call it “co-borrower” or “joint borrower.” The idea is the same. One person is there mainly for contact and responsibility. The other person strengthens the repayment profile with income.

This matters because when students search for “no cosigner,” they often mean “no earning co-applicant.” Not “no second name on the loan papers.” So, it’s important to keep that distinction clear.

3 scenarios where you can get a student loan without a co-signer

While it’s challenging to get an education loan without a co-signer, there are specific situations where this is possible. Here are three:

Taking an education loan from a government bank

Government banks take collateral to secure education loans. Thus, the banks don’t care much about having a co-applicant or the financial profile of the co-applicant.

Furthermore, government banks offer you a payment-free moratorium period.

During the moratorium period, you usually don’t have to start EMI payments.

But the interest continues to accrue. In many bank structures, that interest can get added to the outstanding amount if you don’t service it during the course period.

However, what if:

- You don’t have collateral you can pledge

- The value of the collateral is too low to get the amount of the loan you need

- You don’t have a financial co-applicant

That’s when the rest of the 3 scenarios can help you get a student loan without a co-signer.

Having work experience

If you qualify for this scenario, you can receive up to 40 lakhs of student loans without a financial co-signer or collateral. The interest rate for these loans ranges between 10.5% to 11%.

Check out the eligibility criteria below:

- The loan applicant must have work experience of 3 years or more

- The loan applicant’s last drawn salary must be at least 35K a month

- The loan applicant must have been selected at universities that are present in the top 300 universities list worldwide that lenders keep

- The loan applicant must have chosen an MS or MBA course

Note that the banks or financial institutions still need you to have a primary co-applicant for contact purposes. The banks won’t check the primary co-applicant’s financial profile.

The primary co-applicant must be of your first family, such as parents, siblings, spouse, and in-laws.

Going for international lenders

International lenders offer student loans without a co-signer. The lenders offer student loans in USD and can cover up to 80% of the total cost of education.

Furthermore, these lenders charge between 9% to 10.5% interest on the loan. However, note that since the funds are offered in USD, your repayment cost in INR can still rise if the rupee weakens against the dollar. The interest rate stays in USD. What changes is how many rupees it takes to repay each dollar.

International lenders offer student loans without a co-signer when you qualify to study at one of the universities they have tied up with. If you have been selected at a university that’s not on their list, you won’t be eligible for the student loan.

Now, before you reach out to international lenders, you must decide which ones to reach out to. There are hundreds of them out there, and you can’t rely on random blogs with half-information (or worse, misinformation).

That’s when GradRight’s loan search platform comes to your rescue. Here, you’ll receive:

- Over 30 lenders, including public and private sector banks, NBFCs, and even two international lenders, compete to offer you customized education loans.

- Competitive interest rates that help you save more on your budget.

- A processing time of 48 hours. Know any organisation that offers a faster processing time?

Want to know more? Drop us an email at grad@gradright.com to talk to our financial and educational advisors.

If your goal is to get a student loan for international students in the USA without a cosigner, these three routes are still the core pathways. But what changes is how lenders evaluate you.

For US programs, the university and course matter more than most students expect. Some lenders are comfortable without an earning co-applicant only when the program has strong job outcomes, and your cost sheet is realistic.

“It… will help consumers identify fake apps and encourage them to use only legitimate digital lending apps.” — Adhil Shetty, CEO, BankBazaar.com

Eligibility for an education loan without co-applicants in India

Securing an education loan without a co-applicant is possible under specific conditions. Here are the key eligibility criteria typically required:

- Strong Academic Record: Students with an excellent academic background, high GPA, or strong standardized test scores (like GRE or GMAT) are often considered for loans without a co-applicant, especially by international lenders.

- University and Course Selection: Admission to a top-ranked university, especially those partnered with certain lenders, increases your chances of getting a loan without needing a co-signer. Programs like MS, MBA, or other STEM degrees are more likely to be considered.

- Work Experience: If you have relevant work experience (typically 3+ years) with a stable income, some lenders, including Indian private banks, may offer education loans without requiring a co-applicant.

- Collateral Availability: Public banks in India may offer loans without a financial co-applicant if you provide sufficient collateral, such as property or fixed deposits.

- Recognition of the University: Some lenders have a list of approved universities. If you’ve been admitted to one of these institutions, you stand a better chance of getting a loan without a co-applicant.

The easiest way to gauge eligibility is to think like a lender for a minute. Even when you’re applying for an education loan without a co-applicant, the bank still needs confidence in two things:

- Can the course and university justify the loan size?

- Can you realistically repay the loan once you graduate?

So, the details that matter the most are your total cost sheet and whether you’ve shown a clear gap plan. The loan amount vs your own contribution, the strength of the security, and past payment record all come into play.

After identifying the eligibility criteria, it’s clear that one of the best ways to secure an education loan without a co-applicant is by choosing a university where the cost of studying aligns with the maximum loan limit offered by reputable banks and NBFCs. However, finding such a university shouldn’t mean compromising on the quality of education. This is where GradRight’s university search platform comes in.

It analyzes your academic profile and career goals to match you with universities that not only offer high-quality education but also fall within the financial limits for loans without a co-applicant. The platform uses advanced data analytics to generate a curated list of programs that fit your budget and aspirations.

You create a free profile and provide details about your academic background and financial requirements. The system processes over 8 million data points to identify universities that meet your criteria. You can then compare shortlisted programs based on factors like tuition fees, alumni success, and location. Expert advice is available throughout the process, ensuring you make informed decisions. Finally, you connect with peers and alumni to gather insights and support before making your final choice.

Don’t wait—start your journey with SelectRight today and find the perfect university for your needs.

Also Read: Non Collateral Education Loan for Study Abroad: How To Apply?

Cons of taking an education loan from international lenders

Getting student loans without a co-signer from international lenders comes with its own set of hazards.

Tax benefits under Section 80E are available only when the education loan is taken from a “financial institution” or an approved charitable institution.

So, whether you get 80E benefits depends on the lender’s legal status in India. Don’t assume it either way. Check this before you sign.

Furthermore, the currency fluctuation with INR depreciation means you’ll end up paying way more than what you borrowed.

This is the real risk with international loans. Your EMI is typically in USD. The interest rate stays in USD, too. But if the rupee weakens, you need more INR to repay the same dollars.

So when you compare options for the best student loans for internationals in the USA with no cosigner, don’t stop at approval. Also run a repayment stress check for exchange-rate swings.

Benefits of taking an education loan without a co-applicant

Here are some of the benefits of getting an education loan without a co-applicant:

- Securing a loan without a co-applicant gives you financial independence, allowing you to manage your education expenses without depending on family members.

- If you don’t have financially strong family members or guardians, getting a loan without a co-applicant opens up opportunities that might otherwise be out of reach.

- Lenders offering non-co-signed loans often have streamlined processes, reducing the time it takes to get approval since there’s no need to evaluate another person’s financial profile.

- Without needing to involve a co-applicant, the paperwork is simpler, making the entire loan application process more straightforward.

- Lenders offering non-co-signed loans focus more on your academic achievements, course selection, and university ranking. This gives you a much better chance of approval if you’re a strong student.

In the next section, we will outline the documents that you will need if you are considering applying for an education loan without a co-applicant.

What Are the Documents Required for Education Loans Without a Cosigner?

Applying for an education loan without a co-applicant requires careful preparation. Here’s a detailed checklist based on different types of lenders:

For Government Banks (with Collateral)

- You’ll need an official letter from the university confirming your enrollment.

- You’ll also need to provide proof of ownership of any collateral. These could be property papers, fixed deposit certificates, or other forms of collateral (originals and photocopies).

- You’ll need English copies of all your transcripts, certificates, and mark sheets.

- You’ll need your original Passport, Aadhaar card, or PAN card.

- You’ll also need to provide proof of income. Commonly, these include salary slips, Form 16, or bank statements if you are self-financing during your studies.

- And lastly, you’ll need to complete the loan application form.

For Indian Private Banks and NBFCs

- You’ll need an official letter from the university confirming your admission, along with course details.

- You’ll need to provide documents showing your past employment, especially if you are using it to qualify without a cosigner.

- Again, you’ll need proof of income. These could be recent salary slips (last 3 months) or bank statements if self-employed.

- You’ll need at least two KYC documents. These are Identity and address proofs, including Aadhaar, voter ID cards, driving licenses, and passport copies.

- If applicable, include property or asset documents that you are going to pledge as collateral.

For International Lenders

- Your university admission offer letter. Note: In this case, it must be from a partner university (each lender usually has their list).

- You’ll need a valid passport for identity verification (compulsory).

- As before, you’ll need marksheets and certificates from your previous education. If these are not in English, you’ll need official translations.

- For those applying based on work experience or scholarship, include relevant documents like scholarship award letters or proof of employment.

By ensuring you have these documents ready, you can avoid delays and improve your chances of getting your loan approved without needing a co-signer.

One extra checklist item that students often miss is the cost sheet. Many Indian lenders will ask for a clean estimate of tuition and living expenses.

Keep your fee structure, housing estimate, and insurance estimate ready. It helps the lender size the loan correctly and speeds up your sanction.

If you check the requirements for student loans for internationals in the USA without a cosigner, you’ll see the cost sheet mentioned everywhere.

With that done, let’s look at the process of getting an education loan without a co-applicant in India.

Process for getting an education loan without a co-applicant in India

Getting an education loan in India, even without a co-applicant, can be straightforward if you follow the right steps.

Here’s how to get an education loan without collateral or a co-applicant in India:

- Start by researching Indian banks and financial institutions that offer education loans without requiring a financial co-applicant. Public sector banks like SBI and Bank of Baroda are good options if you have collateral to pledge.

- Ensure that you meet the bank’s eligibility criteria, which usually include admission to a recognized university, a decent academic record, and, in some cases, collateral.

- Gather the necessary documents, including admission letters, academic records, identity proof, collateral documents (if needed), and income proof (if you’re self-financing).

- Most banks now offer an online application process. Fill out the application form, upload the documents, and submit your request. You can also visit the bank’s branch if you prefer a physical application.

- The bank will verify your documents, check your eligibility, and process your application. This stage may involve a representative visiting your collateral property (if applicable) for verification.

- Once approved, you’ll receive a loan sanction letter detailing the loan amount, interest rate, and repayment terms. The funds will be disbursed directly to your educational institution.

Following these simple steps will help you smoothly secure an education loan in India, even if you don’t have a financial co-applicant.

You need to know two practical tips before you start applying. First, find out if the lender means “no cosigner” as in no earning co-applicant, or no second borrower? In India, it’s usually the first. That clarity saves a lot of back-and-forth.

Second, don’t treat sanctions as the finish line. For US universities, disbursement is often semester-wise. So keep your payment schedule handy, and confirm how the lender releases funds.

“Talent is borderless… access to finance is not.” — Cameron Stevens, Founder & CEO, Prodigy Finance

Frequently asked questions about student loans without co-applicant-:

1. Can I get an education loan without a co-applicant?

You can get a student loan without a co-signer from international lenders.

For Indian banks and financial lenders, you can get an education loan without a financial co-applicant. However, you can’t get an education loan without a primary co-applicant.

2. Are there student loans with no cosigner?

Yes, but it depends on where you borrow. Some international lenders offer a student loan for international students in the USA without a cosigner. But you’d need to be admitted to an eligible US university and program. In India, “no cosigner” usually means no earning-backed co-applicant. But a parent/guardian may still be required as a co-borrower.

3. What’s the meaning of co-applicant in education loans?

Ans: A co-applicant is a person whom the banks or financial institutions will ask to repay the education loan if the loan applicant can’t repay the education loan due to any unforeseen circumstances.

That’s why banks and financial institutions are reluctant to offer education loans without co-applicants.

4. Where can I find international lenders for getting student loans without a co-signer?

Ans: We at FundRight are here to help. At FundRight, you’ll get over 30 public and private banks, NBFCs, and two international lenders. Furthermore, we’re working every day to add more lenders to our platform.

5. Should I go for international lenders to get an education loan without a co-applicant?

Ans: The right answer, it depends. If you can get an education loan without a co-applicant through the ways we shared in this article, go for Indian banks and financial organisations.

However, if you don’t qualify for those ways, international lenders are the only way you’re left with.

6. Do international students need a cosigner?

Not always. For US study loans taken in India, lenders may ask for a primary co-borrower. But you might not need an earning co-applicant in some cases. For international/US lenders, some products are truly no-cosigner. But they approve only for specific universities and programs. Always check the exact requirements for a student loan for internationals in the USA without a cosigner before applying.

7. Can a student get an education loan without parents in India?

Yes. You can apply solo or with an alternate co-applicant (like a guardian). Many lenders allow education loan without parents by assessing your profile and income potential. Just ensure you meet their credit and documentation requirements for an education loan without collateral.

8. Which NBFCs offer NBFC education loans without collateral?

Several NBFCs like Avanse, Credila, and Prodigy Finance provide NBFC education loans without collateral up to specific limits. They focus on your admission, course fees, and future cash flow instead of assets. Compare options to find the best unsecured how to get an education loan without collateral deal for you.

The Best Way to Get an Education Loan without a co-applicant

Here’s the simple takeaway. For most Indian students heading to the US, “no cosigner” usually means no earning co-applicant. So your job is to compare the options that fit your admission, your total cost, and your ideal repayment plan.

Sounds overwhelming? Go for GradRight’s reverse-bidding loan platform. At GradRight, we offer:

- More than 30 lenders, including private and public sector banks, NBFCs, and even two international lenders, are happy to offer you student loans without a cosigner

- A processing time of 48 hours. Yeah, you read it right. Do you know of any other organisation that offers a faster processing time?

- Competitive interest rates that allow you to save more on your budget.

GradRight also has strong institutional backing. It raised ₹50 Cr in a Series A round led by IvyCap, which helped scale the platform and expand lender participation.

If you want to know more, drop us an email at grad@gradright.com to strike up a conversation with our financial and education advisors.

Now that you know all about education loans without a co-applicant, we hope the knowledge will help you make the most informed decision.