Most conversations about study abroad ROI begin and end in the same place: total cost versus starting salary. Take the degree, divide the cost by the first-year income, and get a break-even number. If it is under five years, the investment is worth it. If it is over seven, think twice.

That framework is not wrong. However, it is dangerously incomplete. In 2026, two students can borrow the same amount, attend universities at the same rank, and graduate into the same job market. One breaks even in three years. The other is still carrying debt six years later. The difference between those two outcomes is almost never the variable everyone obsesses over. It is rarely the country, the university, or even the field. It is the interaction between seven specific variables that most families only partially account for when they are making the decision.

This blog explains each of those variables clearly, shows how they combine to shape your actual study abroad ROI, and gives you a framework to run the numbers for your own situation, before you sign a loan agreement or accept an offer letter.

Why the simple ROI calculation misses the point

Before going into the variables, it is worth understanding what the standard break-even calculation actually measures and what it leaves out.

The standard formula is: total investment divided by annual salary premium equals break-even years. For instance, a ₹60 lakh loan repaid at ₹15 lakh per year in net salary premium gives a four-year break-even. That looks manageable.

However, this formula assumes constant salary, steady employment, and no compounding interest. In practice, none of those assumptions reliably hold. A student who graduates in the US on an F-1 OPT visa but fails to secure H-1B sponsorship by year three is not earning $95,000 from year four onwards. Moreover, a student with a ₹60 lakh loan at 12 percent interest who takes two years to find a role in their field is not repaying ₹15 lakh per year from graduation. They are paying interest first, then principal, under compounding pressure.

Consequently, the real ROI question is not what happens in the best-case scenario. It is what happens in the realistic one.

Variable 1: Total cost, not just tuition

The first and most commonly underestimated variable in the study abroad ROI calculation is the difference between tuition cost and total cost. These numbers are, in most countries, significantly different.

Tuition is what universities advertise. Total cost is what families actually spend. The gap between the two includes accommodation, food, health insurance, transport, visa fees, one-time relocation costs, and the income foregone during the study period.

| Country | Typical Tuition (2-year Master’s) | Typical Total Cost (Tuition + Living, 2 Years) | Difference |

| USA | ₹35 to ₹60 lakh | ₹70 lakh to ₹1.1 crore | ₹30 to ₹50 lakh |

| UK (1-year Master’s) | ₹20 to ₹35 lakh | ₹40 to ₹60 lakh | ₹15 to ₹25 lakh |

| Canada | ₹25 to ₹40 lakh | ₹50 to ₹75 lakh | ₹20 to ₹35 lakh |

| Germany | ₹0 to ₹3 lakh | ₹15 to ₹22 lakh | ₹13 to ₹20 lakh (living only) |

| Ireland | ₹18 to ₹28 lakh | ₹35 to ₹50 lakh | ₹15 to ₹22 lakh |

The rupee is currently at ₹92 against the dollar and approximately ₹107 against the pound. Unsecured education loan interest rates have touched 12 percent in India in 2026. At that rate, a ₹70 lakh loan running for five years before full repayment costs approximately ₹112 lakh in total outflow. Therefore, students who calculate their ROI from tuition alone, rather than from total cost including interest, are systematically underestimating their actual investment by 30 to 50 percent.

The practical implication is simple: the city where you study and the lifestyle you build while studying are financial decisions, not lifestyle preferences. A student in Stuttgart versus a student in Munich at the same German university can differ by ₹4 to ₹6 lakh per year in total living costs, which directly affects their loan amount and break-even timeline.

Variable 2: Field of study and its salary ceiling in the destination country

Not all fields return equally in all countries. This is the variable most students intellectually understand but do not actually model before choosing a programme.

A computer science fresher in India typically earns ₹3.5 to ₹8 lakh per year at entry level. The same candidate with a US Master’s in STEM earns ₹64 to ₹85 lakh in their first year on OPT. That gap is structural. However, it is specific to STEM fields in the US and does not apply equally to all fields or all countries.

| Field | USA Starting Salary | UK Starting Salary | Germany Starting Salary | India Starting Salary (Top 20 Colleges) |

| Computer Science / STEM MS | $88,000 to $115,000 | £35,000 to £55,000 | €52,000 to €70,000 | ₹12 to ₹24 LPA |

| MSc Finance / Investment Banking | $75,000 to $100,000 | £48,000 to £75,000 | €50,000 to €65,000 | ₹20 to ₹35 LPA (IIM) |

| MSc Management / MBA | $70,000 to $90,000 | £35,000 to £55,000 | €45,000 to €60,000 | ₹18 to ₹35 LPA |

| Public Health / Healthcare Admin | $75,000 to $110,000 | £30,000 to £50,000 | €45,000 to €58,000 | ₹8 to ₹18 LPA |

| Arts / Humanities | $45,000 to $65,000 | £25,000 to £35,000 | €35,000 to €45,000 | ₹5 to ₹12 LPA |

Furthermore, salaries in the same field vary significantly by city within a country. A data engineer in San Francisco earns roughly 40 percent more than the same role in Austin. Similarly, a finance graduate working in London earns more than one working in Manchester. Consequently, the country-level salary figure is only the first layer. The city, the employer tier, and the specialisation within the field all determine the actual number.

Find programs in countries tailored to your profile with GradRight‘s personalized shortlist.

Variable 3: Post-study work visa duration and conditions

Post-study work visa duration is arguably the most financially consequential variable that students underweight in their ROI calculations. The reason it matters so much is compounding. Every additional year of post-study work authorization gives you one more year of high-denomination income before your visa situation becomes uncertain.

Students can work after a Master’s for up to three years in Canada and New Zealand, two to four years in Australia, 18 months in Germany, and up to three years in the USA for STEM courses. These are not minor differences. A STEM MS student in the US with three years of OPT working at $95,000 accumulates substantially more loan-repayment capacity than a non-STEM graduate with one year of OPT at the same institution.

Moreover, post-study work visa conditions matter as much as duration. The UK Graduate Route allows you to work in any sector for any employer, which gives maximum flexibility. The US OPT, by contrast, requires that you work in a role directly related to your field of study. Canada’s PGWP is an open work permit without sector restriction. Germany’s job seeker visa limits you to 20 hours of paid work per week until you convert to a full work permit.

| Country | PSW Duration (Master’s) | Sector Restriction | Job Offer Required at Start? | PR Pathway Timeline |

| USA (STEM) | 3 years (OPT + STEM-OPT) | Must be field-related | No | H-1B dependent (lottery ~28%) |

| UK | 2 years (apply by Dec 2026) | None | No | 7 to 9 years |

| Canada | Up to 3 years (PGWP) | None | No | 3 to 5 years |

| Australia | 2 years (coursework) | None | No | 4 to 6 years |

| Germany | 18 months (job seeker) | None | No | 3 to 4 years (STEM) |

| Ireland | 24 months (Stamp 1G) | None | No | 4 to 5 years |

One important 2026 update for UK-bound students: the post-study work visa is reduced from two years to 18 months for Master’s graduates who apply from January 2027 onwards. Students whose courses complete in 2026 should apply before 31 December to preserve the full two-year window.

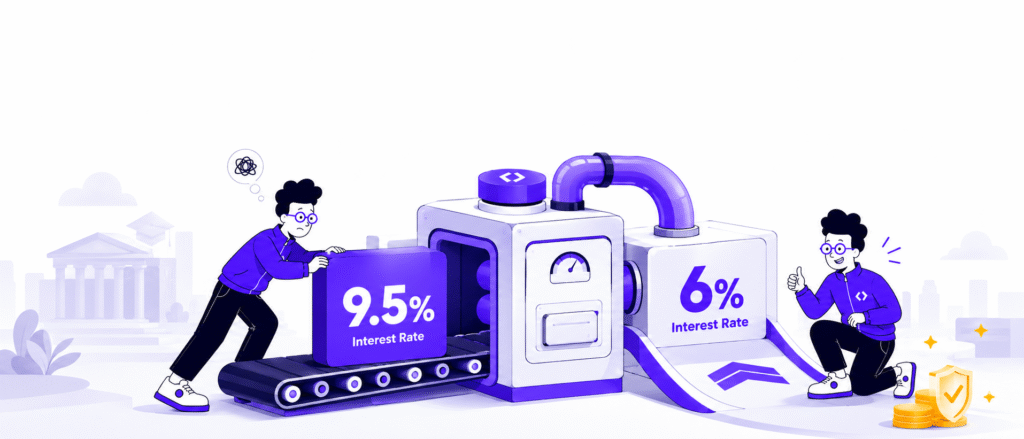

Variable 4: Loan structure and interest rate

Education loan structure is the variable that most directly determines how painful the repayment period feels, even when the underlying ROI of the degree is positive.

Two students borrowing ₹60 lakh for the same programme can have very different repayment experiences depending on whether the loan is secured or unsecured, the interest rate they receive, whether it is a floating or fixed rate, and what the moratorium period looks like. Indian public sector banks offer rates between 8.5 and 10.5 percent for secured loans. Private lenders offer unsecured loans at 11 to 14 percent. Non-banking financial companies and international lenders like Prodigy Finance or MPOWER Financing have their own rate structures.

| Loan Type | Typical Rate (2026) | Security Required | Moratorium | Best For |

| Public sector bank (secured) | 8.5% to 10.5% | Property or FD collateral | Study period + 12 months | Students with collateral |

| Private bank (unsecured) | 11% to 13% | None | Study period + 6 months | Students without collateral |

| NBFC (unsecured) | 12% to 14% | None | Varies | Students with limited options |

| International lender (e.g. Prodigy, MPOWER) | 13% to 16% | None | Minimal | Students at specific partner universities |

A 2 percent difference in interest rate on a ₹60 lakh loan over five years adds approximately ₹7 to ₹9 lakh in total interest outflow. Therefore, the time spent comparing lenders before accepting a loan is among the highest-ROI activities a student can do in the entire study abroad process.

In addition, Section 80E of the Income Tax Act allows Indian taxpayers to deduct the full interest paid on an education loan from taxable income for eight years. For students who return to India after graduation, this deduction meaningfully reduces the net cost of the loan.

Head to GradRight to compare 15+ financial institutions and receive offers which help ypu save up to ₹12 lakhs in EMIs.

Variable 5: Study abroad career skills that carry a salary premium

The India Skills Report 2026, published by Wheebox and the Confederation of Indian Industry, identifies adaptability and cross-cultural communication as among the scarcest skills in the domestic workforce. This matters financially because it translates directly into salary outcomes, both abroad and on return to India.

Study abroad career skills broadly fall into two categories: hard skills that are field-specific, and soft skills that are globally portable. Both carry a measurable premium in 2026.

The hard skills earned abroad that most directly affect salary are those tied to technologies, frameworks, and research infrastructure that Indian programmes do not yet offer at equivalent depth. For STEM fields, this includes access to advanced computing clusters, cutting-edge research labs, and industry-academia pipelines that produce work experience during the degree itself. For business and management students, it includes exposure to global case studies, international faculty networks, and structured employer recruitment on campus.

The globally portable soft skills gained from studying abroad, on the other hand, are what skills employers report most consistently valuing when they hire internationally educated candidates. These are the skills that explain why Indian graduates returning from UK universities consistently secure early-career salaries 20 to 25 percent higher than their domestically educated peers.

| Study Abroad Skill | Why It Carries a Salary Premium | Relevant for Careers in |

| Cross-cultural communication | Scarcest skill in Indian workforce; valued by GCCs and MNCs | All sectors, especially consulting, finance, tech |

| Independent problem-solving | Developed by navigating academic and life challenges alone | Research, strategy, product, engineering |

| Fluency in second language or professional English | Differentiates candidates in global client-facing roles | Law, business development, policy, diplomacy |

| Global network and alumni access | Peer referrals remain the primary hiring channel at senior levels | All sectors |

| Adaptability under ambiguity | Valued by early-stage companies and fast-growing MNCs | Startups, consulting, product management |

What skills do you gain from studying abroad that you cannot easily replicate domestically? In short: lived experience of operating independently in a professional and cultural environment that is not your own. That experience is difficult to simulate and has a documented salary premium of 15 to 25 percent in employer surveys across India, the UK, and the US.

Variable 6: Scholarship and part-time income during the study period

Scholarships and part-time work during the study period are the two most powerful levers students have to reduce their total loan burden and therefore shorten their break-even timeline. Yet both are consistently underutilised, partly because students discover them too late in the application process.

Even a 20 percent tuition cut through a scholarship shortens the payback period significantly. On a ₹60 lakh loan, a ₹12 lakh scholarship reduces the loan principal to ₹48 lakh, which at 10 percent interest over five years saves approximately ₹14 lakh in total outflow. The scholarship application requires a few weeks of effort. The financial return on that effort is ₹14 lakh. The ROI on applying for scholarships is, in most cases, the highest ROI activity in the entire study abroad process.

Similarly, part-time work during study is legally permitted in most destination countries and can meaningfully offset living costs.

| Country | Legal Part-Time Work Hours (During Study) | Approximate Monthly Earnings |

| Germany | 120 full days or 240 half days per year | ₹25,000 to ₹45,000 |

| UK | 20 hours per week during term | ₹35,000 to ₹60,000 |

| Canada | 20 hours per week during term | ₹30,000 to ₹55,000 |

| Australia | 48 hours per fortnight | ₹40,000 to ₹65,000 |

| USA | 20 hours per week (on-campus only on F-1) | ₹15,000 to ₹30,000 |

Over a two-year program, consistent part-time work at the lower end of these estimates reduces living costs by ₹6 to ₹10 lakh, which directly reduces the loan amount required.

Variable 7: What you do in the first 24 months after graduation

The final variable is the one students have the most control over and the least visibility into before they travel: what happens in the first two years after graduation.

This period is where most of the ROI variance between same-programme graduates is created. A student who secures a relevant internship during the degree, applies for roles three months before graduation, and has a job offer before their student visa expires is in a fundamentally different financial position than a student who begins job-hunting on the day their visa expires.

A degree alone does not guarantee a high salary. Skills, internships, and networking play a much larger role in determining outcomes. Students who focus only on academics often struggle, while those who build practical experience succeed.

Study abroad career opportunities are not evenly distributed. They concentrate around students who are geographically present in industry clusters, who have internship experience in the destination country, and who have built local professional networks during their study period, not after it. Consequently, how you use your time during the programme, not just the programme itself, is a major determinant of ROI.

The practical checklist for maximising post-graduation outcomes starts from semester one: connect with the careers centre early, apply for internships before the summer break, build a LinkedIn profile oriented toward your target market (not toward India), and attend on-campus employer events actively rather than treating them as optional.

How much money does it take to study abroad?

This is the most commonly searched question in this topic, and the honest answer is: it depends entirely on which of the seven variables you can optimise.

| Scenario | Total Cost | Loan Required | Break-Even Timeline |

| Germany STEM MS (public university, scholarship) | ₹10 to ₹15 lakh | ₹0 to ₹10 lakh | Under 1 year |

| Germany STEM MS (self-funded) | ₹17 to ₹22 lakh | ₹15 to ₹20 lakh | 1 to 1.5 years |

| UK 1-year MSc (STEM, with part-time work) | ₹35 to ₹45 lakh | ₹30 to ₹40 lakh | 2.5 to 3.5 years |

| Ireland 1-year MSc (tech, Dublin) | ₹35 to ₹50 lakh | ₹30 to ₹45 lakh | 2 to 3.5 years |

| Canada 2-year MS (PGWP, STEM) | ₹55 to ₹75 lakh | ₹50 to ₹65 lakh | 3 to 5 years |

| USA 2-year STEM MS (STEM-OPT, top 50 univ.) | ₹70 lakh to ₹1 crore | ₹60 to ₹90 lakh | 3 to 5 years |

| USA 2-year STEM MS (mid-ranked, no scholarship) | ₹80 lakh to ₹1.1 crore | ₹70 to ₹95 lakh | 5 to 8 years |

The range from “under 1 year break-even” to “5 to 8 years” is not determined by how hard a student works or how intelligent they are. It is determined by how well they optimise the seven variables: total cost, field and destination salary, post-study work visa structure, loan terms, skills and career capital built during the degree, scholarships and part-time income, and how they use the first 24 months after graduation.

The bottom line

Study abroad ROI in 2026 is not a single number. It is the product of seven variables, each of which you can influence before, during, and immediately after the programme. Students who treat the decision as a financial planning exercise rather than a prestige exercise consistently produce better outcomes.

Furthermore, the decisions that most affect your ROI are often the ones that get the least attention: which lender you borrow from, which city within a country you study in, whether you apply for scholarships, and how you spend your time in the first semester. These variables collectively can move your break-even timeline by two to four years.

GradRight helps Indian students compare education loans across 15+ lenders, model their break-even timelines, and plan the financial side of their study abroad decision with real numbers rather than approximations. Start with a free GradRight profile to understand where your specific situation lands across these seven variables.