Your first few months on OPT or an H-1B have probably taught you two things: the dollar salary feels great, and the rupee EMI on your Indian education loan still stings.

You’ve already decided to swap that high-maintenance INR debt for a calm, fixed-rate USD loan. And now, you just need a clear map of how to pull off a student loan refinance for international students.

Here’s the reality most borrowers face:

- Eligibility uncertainty: Which visa classes do SoFi, Citizens Bank, or MPOWER actually accept? When does a thin US credit file become ‘good enough?’

- Documentation riddles: What goes into a payoff statement from SBI or HDFC? And how do you get the bank to issue one within the lender’s 10-day window?

- Process gaps: Who wires the money to India – you or the refi lender? How do you collect the No-Objection Certificate and release collateral?

- Rate-shopping overload: Every website claims to be the ‘best student loan refinance.’ Comparing APRs, fees, and visa requirements across half a dozen lenders is a job in itself.

This guide strips away that confusion. You’ll see exactly which lenders entertain non-citizen applications in 2026, the paperwork queue, and smart ways to pit offers against each other.

You’ll also learn how GradRight makes student loan refinancing a breeze –

with multiple domestic and international lenders bidding on your profile.

Who Really Refinances International Borrowers in 2026?

As of June 2026, only three US lenders routinely consider non-citizens for student loan refinancing, while the rest reserve refinancing for permanent residents or green-card holders.

| Lender | Visa Classes | Pays Off Indian Loan? | Cosigner | Typical Fixed Rate (June 2026) | Key Features |

| SoFi | E-2/E-3, H-1B, J-1, L-1, O-1, other non-PR categories | No – loan must be US-serviced | Optional; most international borrowers apply solo | ~5.9%-9.2% | Broad terms 5-20 yrs; soft-pull pre-qualification; 0.25% autopay discount |

| MPOWER Financing | OPT, STEM-OPT, H-1B, other work visas | Yes – wires directly to Indian banks | No cosigner, no US credit history required | ~9.99% (fixed 10-yr term) | Purpose-built for international grads; higher rate but solves foreign-payoff hurdle |

| Citizens Bank | Resident alien with SSN (F-1/OPT or H-1B) | Sometimes – needs US citizen/PR cosigner | Cosigner mandatory for visa holders | ~6.4%-10.3% | Loyalty and autopay discounts up to 0.50%; harder if loan is still in India |

Rate footnote: All rates are publicly posted ranges as of June 2026, before discounts. Your offer depends on credit score, income, term length, and visa duration. Verify current rates directly with each lender before applying.

What About Earnest, ELFI, Laurel Road and Other ‘Best Rate’ Lenders?

If your loan is still with SBI, HDFC Credila, or any other Indian lender, SoFi and Citizens usually cannot wire funds overseas. In that case, MPOWER is the practical first move. Once the rupee loan is closed and you’ve logged 12-24 months of on-time US payments, you can shop with mainstream lenders for a lower rate.

| Lender | Citizenship/PR Rule |

| Earnest | Citizens or PR only. Often among the lowest fixed and variable rates once you qualify. |

| ELFI | Citizens or unconditional PR. High credit-score borrowers see competitive APRs; 5-20-year terms. |

| Laurel Road | Citizens or PR. Extra 0.25% checking-account discount and physician-friendly perks. |

| PenFed | Citizens or PR; credit 670+. Federal credit union product, no origination fee. |

| Splash Financial | Depends on partner banks, mostly citizen/PR. Single application pulls offers from multiple banks. |

Planning for a second refinance from day one (choosing a no-fee, no-penalty lender first) keeps the door open to even bigger savings down the road.

Compare refinance offers from multiple lenders in one place – let them compete for your loan. Explore on GradRight

Understanding Refinance Rates: Fixed vs Variable and the INR-to-USD Switch

Fixed and Variable Rates in the US

- Fixed APRs: Stay the same for the life of the loan. Popular if you want a predictable monthly budget.

- Variable APRs: Track a short-term benchmark like SOFR. Can start lower but rise with market rates.

Visa-friendly lenders currently advertise (June 2026):

- SoFi: Fixed 5.9%-9.2% for qualified visa holders.

- MPOWER: Fixed 9.99% (11.52% APR) after autopay discount.

- Citizens Bank: Fixed 6.4%-10.3% with a US cosigner.

Why Indian Bank Rates Still Run High

Indian education loans usually float on the External Benchmark Lending Rate (EBLR). The Reserve Bank of India’s repo rate is currently 6.25% (after three cuts in 2025), but each bank’s spread still pushes unsecured study-abroad loans into the 9%-12% bracket.

Every time the RBI tweaks policy, your EMI shifts – which is precisely why many Indian students on US salaries prefer the predictability of a fixed USD loan.

Currency Conversion: INR Risk vs USD Stability

Paying a rupee loan from a dollar salary adds two costs you don’t control:

- INR depreciation: The rupee has slid roughly 4% a year on average since 2015.

- Telegraphic-transfer fees: Banks charge ₹500-₹1,000 per overseas remittance.

Refinancing into USD ends both exposures. Your repayment now matches the currency you earn, and you skip monthly wire fees.

A Quick Number Check

Illustrative example (June 2026 rates, FX ₹84 = $1):

| Scenario | Monthly Payment | Total Interest (10 years) |

| Keep INR loan (11%) | ₹34,400 | ₹16.3 lakh |

| Refinance to USD loan (6% fixed)* | ~₹28,000 | ~₹8.3 lakh |

*Based on $30,120 at 6% fixed. Exchange rates vary – figures are illustrative only. Actual savings depend on your balance, rate, and FX rate at time of conversion.

Student Loan Refinance Eligibility for International Students on OPT or H-1B

1. Immigration and Identity Documents

| What Lenders Need | Typical Proof | Key Notes |

| Valid US status through loan term | Passport, visa stamp, I-94, EAD/I-797 | SoFi: J-1, H-1B, E-2/E-3, O-1, L-1. MPOWER: F-1 OPT, STEM-OPT, H-1B |

| Social Security Number | SSN card or recent W-2 | Needed for credit pull. ITIN alone won’t work. |

| Degree completion | Final transcript or diploma | Citizens Bank and MPOWER require this before releasing funds |

2. Income and Employment

Provide two recent pay stubs or a signed offer letter. W-2s help if you’ve already filed a US tax return. Most lenders want a debt-to-income (DTI) ratio under 40% and reward autopay enrollment with a 0.25 percentage-point rate cut.

3. Credit History

| Scenario | What Works | Workaround |

| Established US file | FICO 670-739 is the ‘good’ zone. SoFi approvals below 700 are possible but rare. | Strengthen cash flow, pay down cards, or wait 6 months to add payment history. |

| Thin or no file | MPOWER underwrites primarily on employment and visa status, not FICO. | A US citizen/PR cosigner can bridge the gap – mandatory at Citizens Bank. |

4. Loan Type and Location

SoFi and most mainstream banks will refinance only loans already serviced in the US. If your balance sits with SBI or HDFC Credila, they’ll decline. Direct foreign payoff is available through MPOWER, and occasionally Citizens Bank if the loan is first transferred to a US servicer.

Paperwork and Processing Timeline

1. Identity and US Status

- Passport photo page and current visa stamp: Scan in colour; show all page corners.

- I-94 record or I-797/EAD card: Download the latest I-94 PDF online.

- Social Security Number: SSN is mandatory for SoFi, Citizens, and MPOWER.

2. Employment and Income

- Pay stubs or offer letter (last 30 days).

- W-2 or tax return if you’ve completed a US tax year.

- 0.25 pp autopay discount applied once income documents are approved.

3. Education Proof

Upload your final transcript or degree certificate. Citizens Bank and MPOWER mark this as critical before releasing funds.

4. Payoff Statement from Your Indian Lender

This single document causes most delays. It must show:

- Exact payoff amount calculated to a future ‘good-through’ date.

- Banking details (SWIFT/IFSC, account number) for the incoming wire.

- Your loan account number and full name.

Request a validity window of at least 15 business days to cover document review and funding.

5. Typical Timeline (After Documents Are In)

| Step | SoFi | MPOWER |

| Initial review | Within 1 business day | 6-8 business days after full upload |

| Final approval and rescission period | 2-4 business days | 3 business days (federal requirement) |

| Disbursement | Funds sent within 10 business days | Wired within 10 business days; Indian bank receives in 5-7 days |

Pro tip: Upload PDFs (not photos), name each file clearly (e.g., ‘Paystub-Jun26.pdf’), and keep the payoff letter’s validity in mind. If the lender takes longer than expected, request an updated statement to avoid short-payment fees.

Step-by-Step Guide: Student Loan Refinance for International Students

With your documents in order, the actual refinance moves quickly – often in 2-3 weeks from rate check to loan closure. Follow these steps in sequence.

- List the exact numbers on your current loan: Note the outstanding balance, current floating rate, remaining term, and any pre-payment rules. Most Indian bank loans carry no pre-payment penalty.

- Pre-qualify with visa-friendly lenders: Use soft-pull tools at SoFi or MPOWER. See fixed and variable offers without affecting your credit score.

- Compare total cost, not just the rate: Factor in autopay discounts, term length, and any origination or late-payment fees before choosing fixed versus variable.

- Request a payoff statement from your Indian bank: Ask for a validity window of at least 15 business days and make sure SWIFT/IFSC details are printed on the letter.

- Upload all documents and authorize the hard credit check: Lenders typically give a conditional approval within 48-72 hours once the full file is in.

- Let the lender (or you) move the funds: Direct payoff: MPOWER wires rupees directly to your Indian bank. Self-remit: SoFi or Citizens deposits dollars into your US account – wire them to India the same day to avoid FX swings.

- Close the Indian loan properly: Collect the No-Objection Certificate, retrieve any collateral documents, and ensure the lien is removed from CIBIL records.

- Set up US autopay immediately: Link a checking account, confirm the 0.25-point autopay discount appears on your first statement, and add calendar reminders for payment dates.

Also Read: Best US Lenders to Refinance Your Education Loan (gradright.com/best-u-s-lenders-to-refinance-your-education-loans/)

Also Read: Student Loan Refinance Rates 2026: What You Need to Know (gradright.com/student-loan-refinance-rates-what-you-need-to-know-in-2025/)

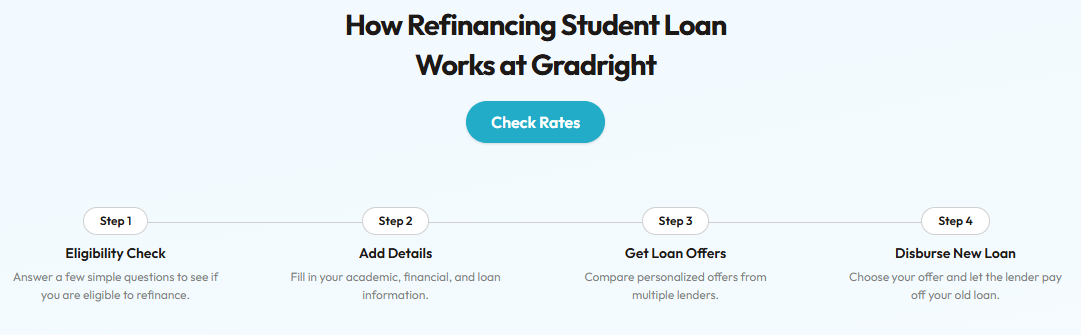

Refinancing With GradRight: One Profile, Multiple Competing Offers

Juggling separate applications to every lender can feel like a full-time job. GradRight shrinks the process into a single online form and lets banks fight for your business.

Here’s how it works:

- Eligibility check (30 sec): Answer a few yes/no questions to confirm you meet basic visa, income, and loan-size criteria.

- Upload details once: Add your academic records, US pay stubs, and current loan balance. GradRight’s dashboard auto-forwards the packet to every matched lender.

- Compare live bids side by side: See fixed vs variable APRs, tenors, fees, and any cosigner requirements in one table. The calculator shows potential savings (₹4.16 lakh on a ₹25 lakh loan when dropping from 11% INR to 6% USD).

4. Select and close: Choose the best offer. The winning lender pays off your old loan while GradRight’s support team walks you through payoff letters and collateral release.

4. Select and close: Choose the best offer. The winning lender pays off your old loan while GradRight’s support team walks you through payoff letters and collateral release.

4.

4. In short, GradRight streamlines the hunt for the best student loan refinance while giving you the negotiating power usually reserved for large corporate borrowers.

Refinance your education loan – one profile, multiple competing offers, free. Start on GradRight

Treat refinancing as a milestone, not an endpoint. Once your rupee loan is swapped for a dollar loan, use the breathing room to build US credit fast – on-time payments, low card balances, no new debt. In 12-18 months, that stronger profile can unlock an even leaner APR or a shorter term, multiplying today’s savings.

Start now: pull your payoff figure, gather the documents in one folder, and request soft-pull quotes tonight. The sooner you act, the sooner your hard-earned salary stops subsidising exchange rates and starts compounding your future.