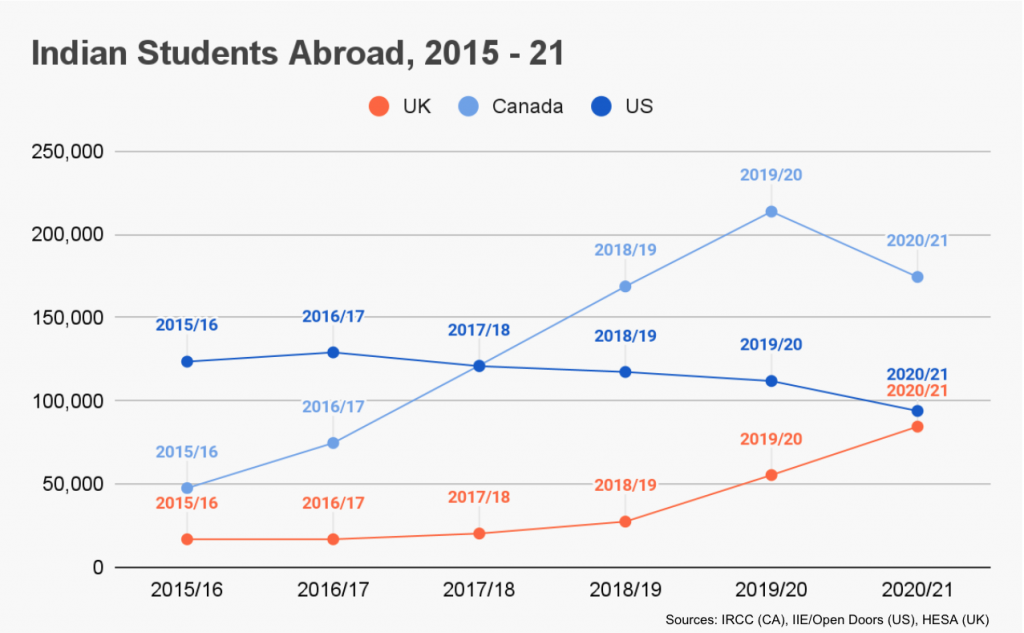

There are about a million Indian students abroad. As the pandemic ends, forecasts project that the number will expand to 1.8 million.

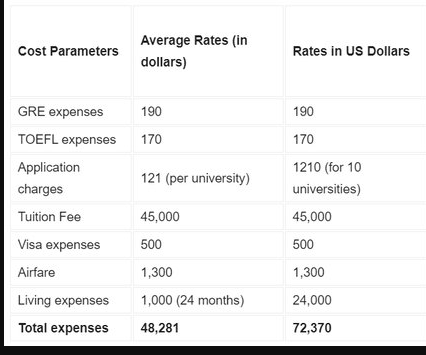

Most of these students have had to avail of hefty bank loans to finance their education abroad. The cost of an MS in the US can be exorbitant (INR 40 lakhs a year at current exchange rates).

But what if the unthinkable happens? If the student faces something tragic, who will pay back the vast outstanding?

Questions such as these make co-signers anxious. It is quite natural since, no matter how much one loves their offspring, paying back a huge outstanding and considerable interest is a burden. Thus insurance on education loans becomes necessary.

Without a doubt, most students are scratching their heads by now. To pay back the loan and interest is an onerous task. Add on more financial burden? Is that a correct decision?

Of course, at the outset, let us hope that nothing much happens, but most financial decisions are based on prudence and not hope.

Insurance on Education Loan—What is it?

The most common way to fund education abroad is through a loan.

Gone are the days when education funds came from selling jewelry or taking loans from family members.

Education loans have many benefits.

- Avail substantial tax benefits under Sec 80E. The entire interest component can be claimed as a deduction.

- Makes it possible for the student to finance his/her own education with as little burden on parents as possible.

- Opens up an opportunity for students from economically weaker sections to participate in higher education and become exceptional professionals.

Every well-known government and private bank in India offers education loans. Several financial institutions also do the same.

In most cases, parents are co-signers. Even secured loans require someone to sign as a co-applicant.

Buying insurance on an education loan will help to mitigate the risk.

In case of a tragic incident, the parents do not have to worry about losing their home to the bank.

For the bank, too, it is a judicious proposition.

The bank might maintain the house deeds as collateral, but they do not want to be involved in the appraisal and the sale of the property. They would rather that someone actually pays them back and helps them avoid all kinds of bookkeeping hassles.

Insurance on Education Loan—Cost

The question a reader might have at this stage is quite natural:

Does it cost an arm and a leg to sign up?

As it is, education abroad is eye-watering due to tuition and boarding fees. Add on a charge on top of it and it seems well near impossible.

Unlike life or medical insurance, general insurance premiums vary widely.

They depend on the amount of risk the bank is taking on.

Of course, the amount is less than taking term life insurance for the applicant. Otherwise, it makes no financial sense to sign up for insurance on an education loan.

Government banks routinely charge between 1% and 2% of the loan amount as the premium.

On a loan of 30 lakhs that works out to INR 30000—INR 60000. Not a huge amount when you consider the peace of mind it brings.

Is It Mandatory to Buy Insurance on an Education Loan?

Not at all.

No bank can insist that you buy another financial instrument to de-risk an existing transaction.

At most, they can ask for collateral and a co-signer.

If you approach lenders through FundRight, you are assured of the best and most lenient terms. Lenders from several financial institutions and banks would view your application and bid against each other. You pick the one you deem best, right from the comfort of your study table. No hassle, no wait and minimum paperwork.

But most banks would at least offer you the advice to sign up for insurance on an education loan.

After all, it makes good sense if for INR 5000 per month or less you can have a viable mechanism to pay the loan back in case there is a mishap.

In case a financial institution not covered by RBI offers a loan with no collateral, they are fully within their rights to insist on insurance on education loan.

A lot of persuasion is usually unnecessary since the benefit far outweighs the cost.

Payment Process for Insurance on Education Loan

When the student buys insurance on an education loan, how does he pay?

Be assured that there is no separate transaction to keep track of.

The amount of premium will be added to the education loan EMI.

The amount of premium and number of times you have to pay would depend on the loan tenure, moratorium period, and other factors.

As the loan amount decreases, the amount of insurance premium would be adjusted downwards (at the same time the loan applicant will increase in age so it might offset an increase in premium).

Breaking down an Education Loan Policy

There are education loan insurance policies from a number of banks. It is best if we dissect one and examine the terms and conditions.

For our case study, we have chosen SBI Life – RiNn Raksha.

State Bank of India is the largest lender in the country, surpassing any rival from the private or public sector.

SBI Life – RiNn Raksha

To begin with, the insurance product is general purpose and not for educational loans alone.

Features of SBI Life – RiNn Raksha

- It is a Group Credit Life plan. Let’s dig deeper. Group indicates several people can be covered. In the case of educational loans, this would include the parents usually. Credit indicates that it is a loan de-risking instrument. Life means it would pay back the sum assured upon the end of life.

- The amount of death cover would be the loan amount outstanding. What the co-signer would have to pay, would be paid up by SBI Life – RiNn Raksha.

- The cover can be increased during insurance tenure to 120%. A loan of INR 30 lakhs can be raised to INR 36 lakhs, but no more. This makes it impossible for the applicant to avoid paying EMI and passing on the burden to SBI Life.

- The premium can be funded by the lender.

- There would be a moratorium period of 3 months to 6 years, during which disbursements could be staggered.

- The education loan insurance has to cover at least 2/3rd of the loan amount. A loan of INR 30 lakhs must carry a cover of at least INR 20 lakhs.

- Apart from the loan applicant, two more persons who are co-signers can be covered. Each can be covered for the whole loan amount or a proportional share. The premium would vary accordingly.

- Premium can be paid in a single installment or level premium after 5 or 10 years.

- There is no maturity benefit. Like health insurance, there is no sum assured at the end of tenure. Otherwise, think of it as pure insurance risk with no financial investment benefits (like whole life plans, endowment plans, etc).

Eligibility of SBI Life – RiNn Raksha

SBI Life – RiNn Raksha eligibility criteria is given below:

| What type of plan? | Group Insurance |

| Minimum age of policyholder | 16 years |

| Maximum age of policyholder | 70 years |

| Maximum age at maturity | 75 years |

| Minimum group size | 20 |

| Maximum size | No limit |

| Minimum tenure | 2 years |

| Maximum tenure | 30 years |

Sum Assured and Premium for SBI Life – RiNn Raksha

| Minimum sum assured | INR 10000 |

| Maximum sum assured | No limit |

| 2 years to 30 years | Single Premium |

| 8 years to 30 years | Premium Payment Term – 5 years |

| 15 years to 30 years | Premium Payment Terms – 10 years |

Premiums can be paid monthly, quarterly, half-yearly, and annually.

SBI Life – RiNn Raksha offers two plans that are slightly different.

- Gold Plan – The amount payable upon death is equal to the outstanding loan amount based on the floating interest rate as calculated by the lender.

- Platinum Plan – The amount payable upon death is at least equal to the outstanding loan amount based on the interest rate at inception.

Let’s understand with an example.

Arnav Bose took an educational loan from ICICI Bank of INR 30 lakhs at 7.2% per annum floating rate on April 20th, 2018.

The premium was paid by a single premium every year.

On May 15th, 2022 he died due to a traffic accident near his university. The rate of interest at that time had dropped to 6.5%.

- According to Gold Plan SBI Life – RiNn Raksha would pay the amount that ICICI Bank calculates at a floating rate.

- According to Platinum Plan SBI Life – RiNn Raksha would pay at least 7.2% interest. If after paying ICICI Bank in full any amount is excess then the survivors can claim it.

Usual income tax benefits apply under Section 80C and 10(10)D.

What is Not Covered by SBI Life – RiNn Raksha

There will be no payout in case of suicide by the person whose life is insured within 12 months. 80% of the total premium paid would be refunded without interest after subtraction of necessary taxes.

Do You Need Expert Advice?

In times like these one often needs a friend and advisor.

Why Use FundRight

It’s not enough to ask your uncle who sometimes dabbles in the stock market about education loan insurance.

You need experts who have been in the field for years and have practical experience of sending students abroad.

Enter FundRight.

FundRight get you the funds you need at the least cost through a reverse bidding process.

The FundRight Advantage

You provide FundRight with the details and FundRight places them before lenders.

There is no need for you to make twenty sets of photocopies and wait in the bank foyer for two minutes of the manager’s time.

Lenders from 30+ banks, financial institutions and NBFCs go through your details and decide what is the best offer they can provide.

You pick the one you like best.

As easy as that.

Last Words

There is intense competition for study at foreign universities. You need to focus on your Indian board exams, IELTS, visa and so much more.

We promise to make fundraising and college selection the easiest part of going abroad.

Call us and we shall make your dream come true.