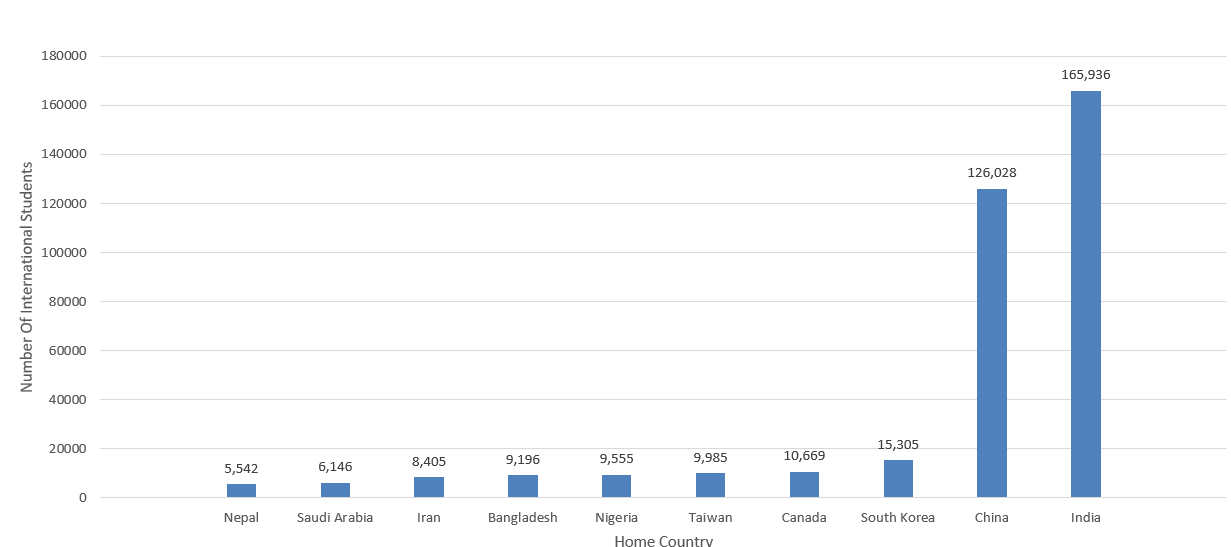

Take a look at the following graph. It shows the number of graduate students in the U.S., by country of origin. By far, the most populous are Indians. The story is the same in any other popular destination for students: UK, Australia, Ireland.

Source: Statista

Given the high cost of studying in the U.S., many of those students will have taken an education loan — and so can you.

Finding the best education loan in India is crucial for students planning to pursue higher education overseas. Let’s explore the top loans from various banks..

It is important to get the right loan early on, as even half a percent of interest can save you lakhs in the long run. More on that later.

And without any further ado, let us look at which is the best education loan in India.

Best education loan in India in 2025

At FundRight, we believe that no education or financial consultant can tell you what’s best for you. For instance, what might be the best education loan in India for one student, may not be the same for you.

Still, we can highlight some of the more popular loan products/lenders from India.

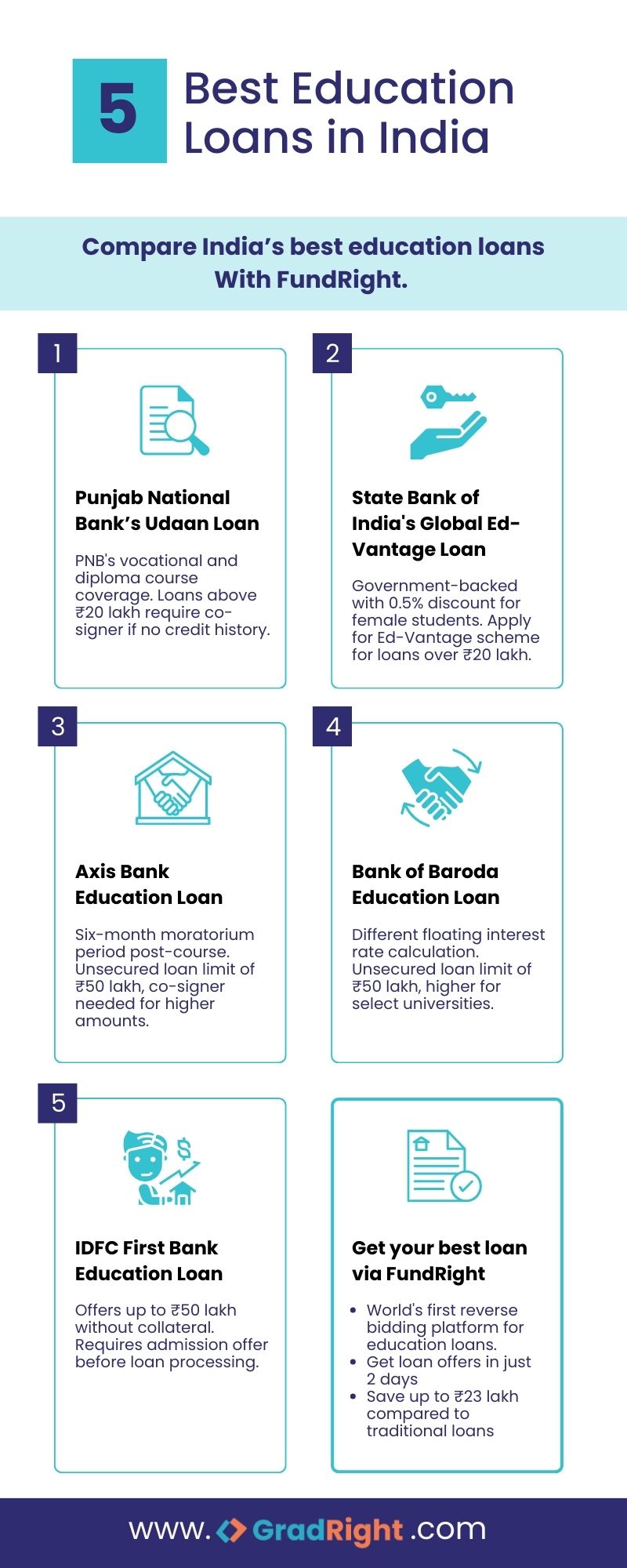

- Punjab National Bank

- State Bank of India

- Axis Bank

- Bank Of Baroda

- IDFC First Bank

Below is why each of those loans made our top five list.

Punjab National Bank Education Loan

PNB’s “Udaan” line of loans allows for professional courses (including diplomas) that other banks would normally reject. They even consider vocational courses, which are becoming popular for Australia (mining, rigging, drilling, etc).

State Bank of India (SBI) Education Loan

Being funded by the government, SBI is one of the best banks for education loans. SBI offers two loan schemes, but most borrowers will prefer the “Global Ed-Vantage” offering. The loan allows a discount of 0.5% (interest) for female students.

Axis Bank Education Loan

Axis Bank offers one of the best education loans for students in India. Borrowers should note however that the axis bank moratorium period is 6 months post-course completion, not 1 year. The moratorium period is the amount of time you have after graduating before you need to begin paying your EMIs.

Bank of Baroda Education Loan

Bank of Baroda often crops up as an answer to “which bank is best for education loan?”. Note that BOB uses a different floating interest rate calculation than other banks, so consider that if you are not opting for a fixed rate loan.

IDFC First Bank Education Loan

IDFC first bank has one of the best education loan interest rate(s) in the country. However, that is not why they are on our list. IDFC First Bank offers the best education loan in India without collateral, providing up to ₹50 lakh without collateral. This is useful for students who do not have assets that can cover the cost of their loan.

Each of these loans has the student’s needs in mind. The best bank for education loan will depend on your specific needs, including the type of course and where you plan to study.

As with everything, this list comes with some restrictions that you should know about.

For PNB loans

- Loans above 20 lakh require a co-signer if you do not have credit history.

For SBI loans

- For loans above 20 lakh, you should apply for the “Ed-Vantage” loan scheme. It has no penalty for prepayment.

For Axis Bank loans

- For unsecured loans, the limit is 50 lakh.

- The “no-maximum” loan limit is only for “secured” loans, i.e. loans with collateral.

- If You want unsecured loans above 50 lakh, Axis bank asks for a member of your immediate family to be a co-signer.

For BOB loans

- Unsecured loans are available only up to a limit of 50 lakh.

- Higher unsecured loans are available to get admission to certain colleges (mainly A-list/ Russell Group) universities.

For IDFC First Bank loans

- IDFC First bank requires the admission offer in hand before your application can be processed.

In the next section, we’ll understand education loan interest rates for foreign studies, and how they affect you.

Also Read: Get non-collateral loans with FundRight

Education loan interest rates for foreign education in India

When taking out a loan, the first thing you have to contend with is the interest rates.

Now, a bank does not just get to decide their interest rate based on their whims and fancies. The interest rate of an education loan (any Indian loan in general) is based on the Reserve Bank of India (RBI). The RBI sets a prevailing (base) rate of interest.

Private banks can then add on their additional interest. This additional interest includes the bank’s processing charges, and profit margins. The repo rate is usually a couple points higher than the prevailing rate of inflation in the country, but that is atopic for another day. Basically, the interest rate of an education loan in India is made up of two parts:

RBI Repo Rate + Bank’s Additional interest = The interest rate offered to you.

If a bank offers you a “floating interest rate,” that means the interest rate can change. The rate can change over the lifetime of your loan. For instance in year one you could be paying 9.15%, and in year six you find you’re paying 8.5%.

This happens if the repo rate goes down during your loan period. However, weigh the pros and cons carefully because the repo rate can also go up instead of down. That would end up increasing your rate of interest.

The RBI updates the repo rate through press releases, the latest of which (as of March 2024) can be found here. You can also learn about the charges on foreign education loans levied by the Indian government here.

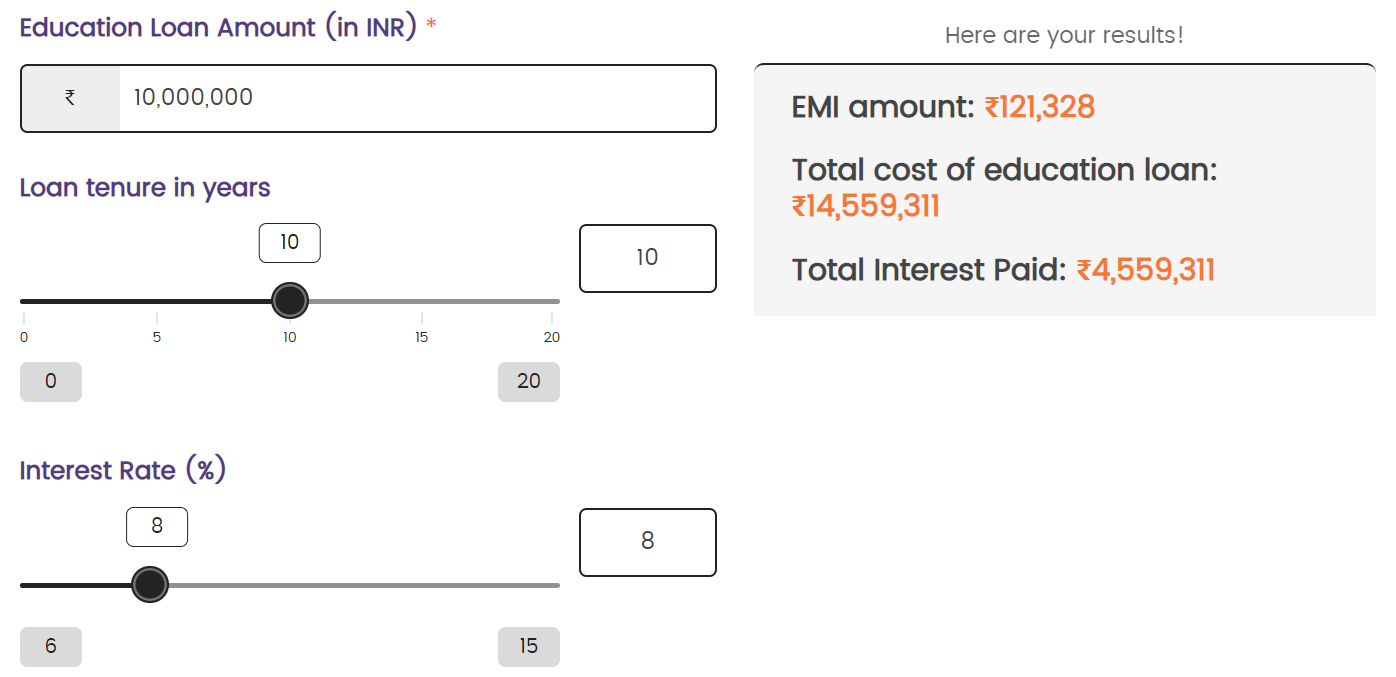

To illustrate how interest rates affect your monthly repayments, consider this example:

- Principal (P) = ₹1,00,00,000 (₹1 Crore). This is the amount that the bank will grant you.

- Rate of Interest (R) = 8% per annum. This is the effective interest rate on the principal (P).

- Tenure (N) = 10 years. This is the number of years you have (once repayment starts) to pay off the loan. Most lenders allow you to pay it off earlier , with a small penalty should you have the funds.

Because we are looking at monthly repayments, we convert the annual interest rate into a monthly number.

- Monthly Interest Rate = (8/12) / 100 = 0.0067

The formula for your monthly amount is: EMI = [P x R] x [(1 + R)N] / [(1 + R)N -1].

Using this formula, we can see that your monthly repayment (EMI) would be approximately ₹121,328.

Source: The GradRight EMI Calculator

However, calculating these figures manually isn’t necessary. At GradRight, we offer two calculators to help you. One is for determining your loan eligibility and another for calculating your monthly repayment. This simplifies finding the best bank for education loan(s) and managing your finances effectively.

Choosing the best bank for an education loan or the best education loan in India requires understanding these interest rates and how they impact your repayment plans. Always research to ensure you select the best education loan for your situation.

For instance, if you are studying for a field that lands a very high paying job (engineering, medicine, programming), you may want to opt for a shorter tenure and higher EMI.

Now let us look at the advantages that an education loan in India provides you.

Also Read: All About Education Loans Without Co-Applicants

Advantages of education loan in India for abroad studies

Securing the best education loan in India comes with many benefits, especially for students aiming to study overseas. Let’s break down the main advantages.

Affordable Interest Rates

Unlike car, house, or personal loans, education loans have low interest rates. This makes them a financially wise choice for covering education expenses. Even if, say, a personal loan can cover your study needs, opt for an education loan instead. The process is a little longer, but the benefits are worth it.

Extended Repayment Periods

Education loans offer the luxury of long repayment tenures, ranging from 15 to 20 years. This flexibility is far beyond what you’d find with other types of loans, where repayment periods are typically shorter.

Tax Benefits

Under the Income Tax Act, students taking education loans can avail certain tax deductions. Opting for longer tenure loans can lead to substantial savings over time. Depending on the situation, your co-signers will also be eligible for a tax exemption, based on their contribution. Note: you can only begin to avail the deductions one year after loan repayment has started. Your exemption will fall under section 80-E of the tax code. You get to deduct the interest paid on the loan from your taxable income.

No Collateral Required

Up to a certain amount, usually ₹7.5 lakhs, no collateral is needed for education loans. However, some banks can offer no-collateral loans up to ₹50,00,000. In our section above on the best education loan in India, we have an example of this (IDFC).

Comprehensive Coverage

Education loans often cover the entire cost of your education. This includes not just tuition fees but also accommodation, travel, and other related expenses, varying by lender.

Credit Score Improvement

For young borrowers, timely repayment of education loans can significantly boost credit scores. This is a critical step in building a strong financial foundation for the future. Note: you will only benefit from credit score improvement if you are one of the co-signers on the loan. If the loan is in your name but your parents are the ones who are paying the EMIs, only your parents can claim the deduction. In this case, your credit score will not be affected by the loan repayment, for better or worse.

Post-Education Repayment

In most cases, EMIs commence only after the completion of education. For instance, if your degree spans four years, repayment would typically start 4 + 1 years later. This grace period allows students to focus on their studies without the immediate pressure of repayments.

Each of these advantages highlights why finding the best bank for education loans or the best NBFC for education loan is important. Whether exploring the best bank for abroad education loan or the best overseas education loan in India, these points will help you.

Next, we will look at the eligibility criteria for an education loan in India.

Education loan eligibility criteria

Familiarizing yourself with these factors will help you determine which bank is best for overseas education loan(s). Some lenders may also want additional documentation such as external scholarships and bursaries.

Applicant Citizenship

Eligible applicants for Indian-based lenders must have a tie to the country. For this, the applicant (and all co-signers) would need to be one of the following:

- Indian Citizens,

- Non-Indian Residents (NRIs),

- Persons born to Indian parents abroad who wish to study in India.

Note: Persons of Indian Origin and Overseas Citizens of India are also eligible for these loans. However, you need to check individually with your lender, as residents of certain countries are ineligible.

Educational Levels

Loans are available for a wide range of educational levels. These include graduation and post-graduation courses, job-oriented, doctoral, PhD, diploma courses, and more. In normal circumstances, it is usually not possible to take an education loan for qualifications lower than a bachelor’s. Check with your lender if that is your requirement.

Collateral Requirements

Depending on the amount and the best bank to take education loan from, collateral might be needed. Acceptable collateral includes residential or commercial property, plots, fixed deposits, and insurance policies.

Understanding these criteria can help you determine which bank is best for your education loan(s). Next, we will show you what documents you need to get in order to get approved for your education loan.

Documents required for an education loan

When applying for an education loan, having the right documents is crucial. Here’s a quick checklist:

For the Student-Applicant:

Proof of Identity

One valid document required. You may use your passport, aadhaar card, voter ID card, PAN card, etc. If a hindu undivided family is applying for the loan, they will not be able to claim the tax benefit outlined in the sections above. The same holds true for a company. Indian companies are not eligible for tax exemptions from education loan repayments.

Proof of Residence/Address

Passport is mandatory for studies abroad, so might as well use the passport as proof of residence. If your current address is different from your passport address, make sure to communicate this to the bank officer.

Academic Records

Includes 10th and 12th results, graduation results if applicable, and entrance exam results. Certain banks, like Axis Bank, also offer interest rate reductions based on your competitive exam scores (GRE/ GMAT/ TOEFL/ etc).

Proof of Admission

An offer of admission letter is required from the institution. This is not strictly a requirement though. Many, if not all banks, offer pre-admission loans. You are likely to be asked for your high school results if you apply for a pre-admission (prospective) loan.

Statement of Cost of Study

This is a schedule of expenses covering evert aspect of your education in a foreign university. If your target university does not publish a cost of study statement, you will have to make one yourself. Include tuition, estimated living expenses, and other miscellaneous expenses. You will need to attach proof of your estimations.

- Course Prospectus If available

- 2 passport-size photos

- Last 1-year statement if there was a previous loan

For the Co-applicant/Guarantor:

- Proof of Identity and Residence/Address: Same requirements as the student.

- 2 passport-size photos

- For the last year if there was a previous loan

Income Proof:

- For salaried individuals: Salary slips, Form 16, IT returns, and a 6-month bank statement.

- For self-employed individuals: Business address proof, IT returns, TDS certificate, and a 6-month bank statement.

Additionally, property or other security documents might be required, depending on the loan.

Gathering these documents beforehand will simplify the process. Some banks require less documentation than others. Knowing this will help determine which bank is best for education loans for study abroad.

Major banks and NBFCs providing education loans

When it comes to securing an education loan, knowing which bank is best for an education loan in India or identifying the best student education loan in India is crucial. Here’s a brief overview:

NBFCs Overview:

Here are the most popular NBFCs for education loans in India.

- Avanse offers loans up to 1 Cr with interest rates starting from 11.5%, and a repayment duration of up to 15 years.

- Incred provides loans up to 60 lacs, with the same interest rate starting point, but caps the repayment at 10 years.

- Auxilo you can get up to 75 lacs, enjoying similar starting interest rates and a decade for repayment.

- HDFC Credila also offers up to 75 lacs at a slightly better starting interest rate of 11% and up to 15 years to pay back.

All these NBFCs offer a nil loan margin, a processing fee between 1-1.5% of the loan amount, and a moratorium period that includes the course duration plus 6 to 12 months, depending on the lender.

Banks Overview:

We have already talked about the best education loan in India at the beginning of this article.

Here is a table with additional information about the best NBFCs and the best banks for education loans in India.

| Bank/NBFC | Interest Rate Range | Loan Type | Loan Amount Range |

| State Bank of India | 8.30% to 11.50% | Need-based term loan up to 15 years. | Up to INR 1.5 Crore |

| Punjab National Bank | 8.55% to 11.25% | Need-based term loan up to 15 years. | Up to INR 1 Crore |

| Bank of Baroda | 9.10% to 12.45% | Term loan need-based funding. | Up to INR 80 Lakhs |

| ICICI Bank | 9.50% onwards | Term loan up to INR 1 crore for domestic, and INR 2 crore for international studies. | Up to INR 2 Crore |

| Bank of India | 8.25% to 11.60% | Term loan need-based financing. | Up to INR 1 Crore |

| Bank of Maharashtra | 9.20% to 11.05% | Term loan up to INR 10 lakh in domestic and up to INR 20 lakh for abroad studies. | Up to INR 20 Lakhs |

| Central Bank of India | 8.30% to 11.25% | Term loan up to INR 50 lakh. | Up to INR 50 Lakhs |

| Axis Bank | 13.70% to 15.20% | Customizable loans with flexible repayment options. | Up to INR 40 Lakhs |

| Kotak Mahindra Bank | Up to 16.00% | Custom solutions based on course and institution. | Varies |

| Canara Bank | 7.30% to 9.30% | Need-based term loan. | Up to INR 40 Lakhs |

| Mpower Finance | Starts from 8.00% | No collateral, cosigner-free loans. | Up to $100,000 |

| Prodigy Finance | Variable | Borderless credit, based on future earning potential. | Up to 100% of tuition fees |

Note: All of the above banks (not NBFCs) allow you to foreclose your loan. And now, let us learn the process of applying for these loans in India.

Disclaimer: Though we say that the tenure varies, all banks will generally offer a loan of 15 years, especially if the loan amount is above ₹1 Crore.

How to apply for education loan in India

Applying for an education loan requires careful planning and attention to detail. Here’s a streamlined guide to help you through the process.

- First, verify if you’re eligible for the loan based on your course, institution, and nationality.

- Prepare your documentation, including identity and residence proof, admission letter, and financial details of the co-borrower.

- Research and compare various lenders. Look for competitive interest rates, favorable repayment terms, and positive customer feedback.

- Apply through the lender’s website or apply for multiple lenders through FundRight. Ensure all your paperwork is complete and accurate.

- The lender will assess your application to determine if you qualify for the loan, the amount you’re eligible for, and under what terms.

- Upon approval, review and sign the loan agreement to finalize the terms.

- The loan amount will be disbursed as agreed, ready to be used for your educational expenses.

Selecting the right lender and understanding the terms of your loan is crucial. Taking time to research and compare options can save you from future financial stress, ensuring a smoother education journey.

You can get real world insights by adding the name of a platform behind your search query. For example, type in “best bank for education loan in india quora” for Quora articles. You could type in “best bank for education loan in india Reddit” as well. These will show you real-life experiences of people who have been where you are, helping you make a better decision.

How can FundRight simplify the process?

Navigating the major loan providers in India can be challenging for an individual.

By the time you’ve researched five loan providers, you’ll just want to take something that seems decent. FundRight solves this problem.

Having a tool like FundRight can help you save up to 23 lakhs over the course of your loan tenure. All you need to do is:

- Register today

- Complete your profile

- Unlock loan offers from India’s top 15 banks and NBFCs

- Get personal support from an expert financial advisor from FundRight, who will help you negotiate for even better terms with the bank.

- Upload your documents securely via FundRight

- Get your loan approved in as little as 10 working days.

Frequently asked questions

1. How do I find the best education loan for studying abroad?

Start by comparing loan offers from various banks and NBFCs. Look at interest rates, repayment terms, and eligibility criteria. FundRight can help streamline this process by offering comparisons from India’s top lenders.

2. What factors affect the interest rate of an education loan?

Interest rates can vary based on your credit score, the loan amount, the repayment period, and the lender’s policies. The financial market conditions at the time of applying also play a crucial role.

3. Can I apply for an education loan for abroad studies without collateral?

Yes, some lenders offer unsecured loans for studying abroad, but these generally come with higher interest rates and may have a lower maximum loan amount.

4. What expenses are covered by education loans for studying abroad?

Loans typically cover tuition fees, living expenses, travel costs, and sometimes even insurance. However, coverage can vary by lender, so it’s essential to check the specifics.

5. How long does it take to get an education loan approved for?

The approval time can vary from a few days to a few weeks, depending on the lender and the completeness of your application. Using FundRight can expedite the process, offering loan offers within two days.

6. Are there any tax benefits on repaying the best education loan?

Yes, under Section 80E of the Income Tax Act, the interest paid on education loans is deductible from your taxable income, which can lead to significant savings.

7. What should I do if my education loan application for studying abroad is rejected?

First, understand the reasons for rejection, such as low credit score or insufficient income of the co-borrower. Then, address these issues and consider reapplying or consulting with a financial advisor for alternative options.